This is the tenth edition of The Polycrisis newsletter, written by Kate Mackenzie and Tim Sahay. Subscribe here to get it in your inbox.

Decarbonization—reducing the output of invisible CO2 molecules into the atmosphere—requires nothing less than remaking the chemical basis of fossil fuel civilization. The energy transition from an economic system run on fossil-fuels into a new metals-based one will reshuffle winners and losers, and blow up both domestic and international political orders. The major decarbonization plots unfolding globally are in the realms of cash (green finance), cars (EV growth), and chemicals (battery production). Inspired by energy finance analyst Nathaniel Bullard’s tour-de-force presentation illustrating the white-knuckle ride of the energy transition, this week’s newsletter picks out a few big charts that get at the antinomies of these three processes.

Cash

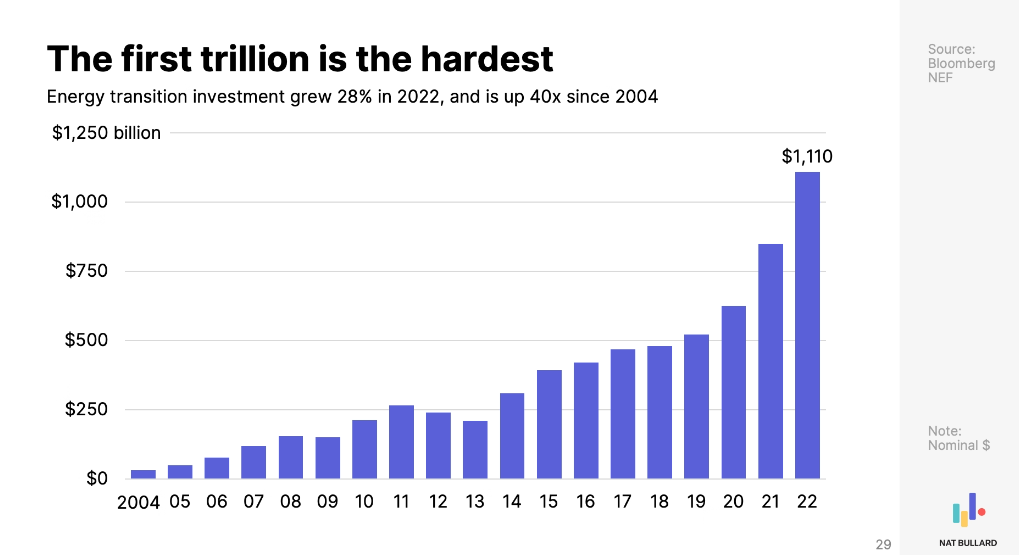

Not so long ago, one trillion dollars in annual global green investments was the goal. We are now there:

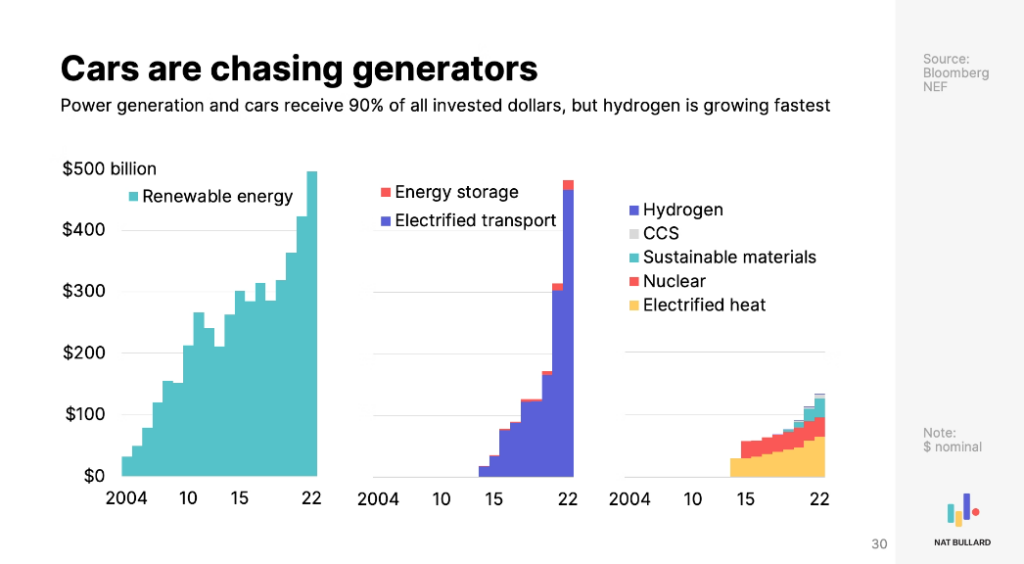

But the energy transition requires stamping on the brakes of fossil fuels and the green accelerator. The largest banks in the world still lend more money to fossil fuel projects than clean energy projects. The money that has flowed into green investments so far concentrates on two destinations: renewable energy generation and the auto sector:

Cars

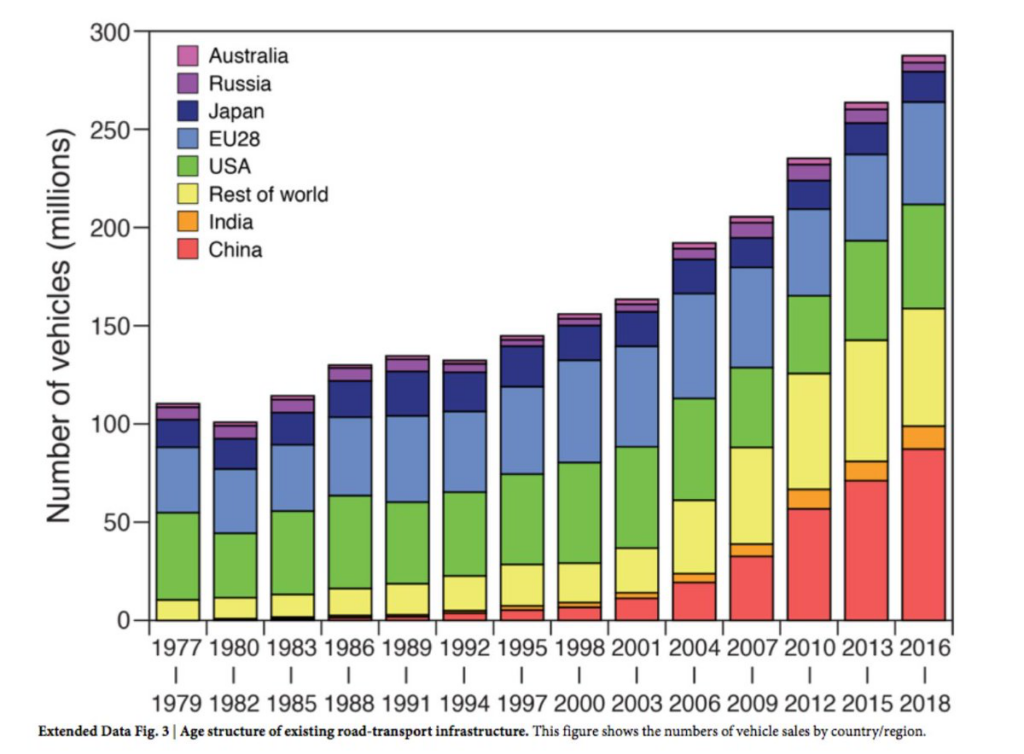

Road transport is responsible for about one fifth of all energy-related CO2 emissions and a large proportion of harmful air pollution. For many governments, the auto sector is also a powerful political constituent and a key node for economic growth and industrial strategy. Moreover, as the largest chunk of cross-border traded goods, the car itself is an emblem of globalization.

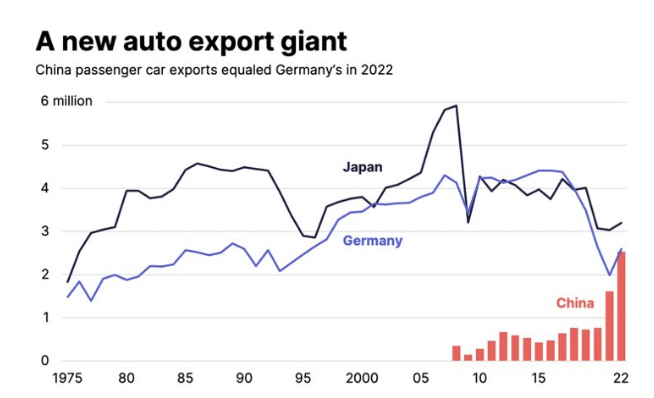

The essential questions are: Who makes them, and who feeds them? Until recently, the first question could be easily answered: Japan, Europe, and North America. In the case of the second question, the answer was simply crude oil from the US, the Middle East, and Russia. But in the past five years, a seismic shift has taken place in the industry: China overtook Germany to become the biggest exporter of passenger cars in the world.

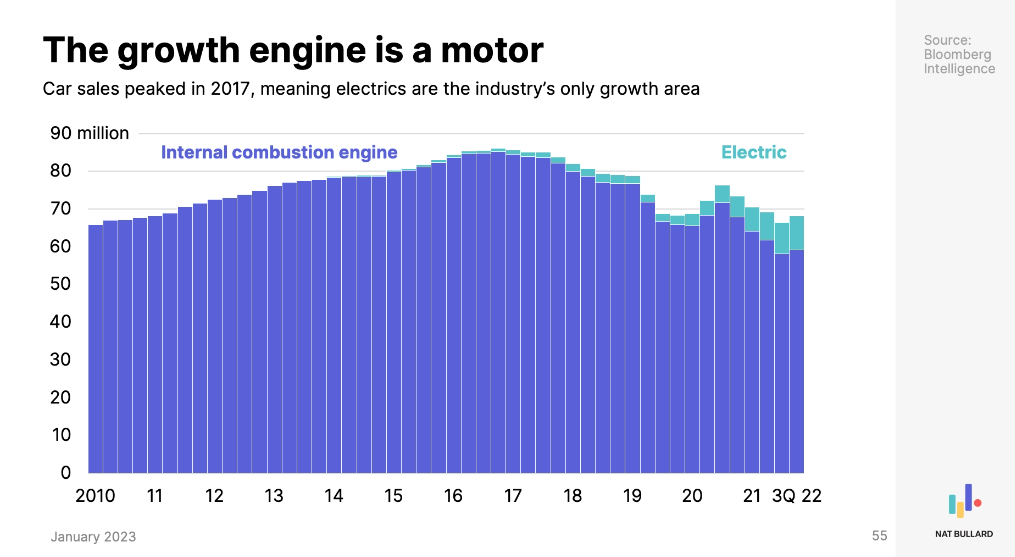

A lot of that growth came from Tesla’s factory in Shanghai. But look around you. Most people in countries like the US have never seen a Chinese-made car. For all the talk of post-Fordism, global production of internal combustion engines is at an all time high. There are over 1 billion cars on the roads. That’s over 280 million cars in the US, China and EU each. In the US, EV sales are at just 5 percent. In China, the figure is 20 percent, and in the EU, 10 percent.

Every manufacturing power—and every aspiring manufacturing power—now has overcapacity issues, having over-invested in internal combustion engines. As sales of EVs boom, those stranded assets and lost jobs will find political champions.

The days of internal combustion engines may be numbered, but we should expect the unexpected. Just this week, German liberals and Italy’s far right pushed back on a proposed EU ban on internal combustion engines by 2035. The entrenched car industry is going to rage against the dying of the light.

The formidable political power of the gas car bloc, and the centrality of cars to American life in particular, provides the terrain for further surprising and climate-devastating sectoral politicking. In the US, big farms have turned out to be more powerful than even the fearsome oil lobby. How? Simple math, as Senator Bob Dole once suggested: twenty-one farm states equals forty-two farm senators. Each time oil prices spiked—in the 1970s, in 2000s, and once again in 2022—those senators made a deceptively simple argument: replace expensive imported gasoline with domestically produced corn ethanol. Yes, corn in cars.

In 2007, these senators secured the passage of the Energy Independence and Security Act. It mandated that 10 percent of every gallon of gas has to be made from corn ethanol. Its ramifications literally terra-formed the world.

BigAg wasn’t done taking sales of petrol away from BigOil. Cheaper ethanol from higher-yielding Brazilian sugarcane was blocked by tariffs, and prairies in the upper Midwest were furiously plowed into cornfields. By the mid 2010s, almost half of all US corn crop was turned into ethanol. So began the search for a cheaper oil for food. The resulting explosion in palm oil production included a plantation boom in the rainforests of Indonesia, which required the slashing and burning of rainforests, and unstoppable peat fires. The 2015 Indonesian fires produced over a billion tons of CO2 and rank among the worst environmental catastrophes of the twenty-first century.

Chemicals

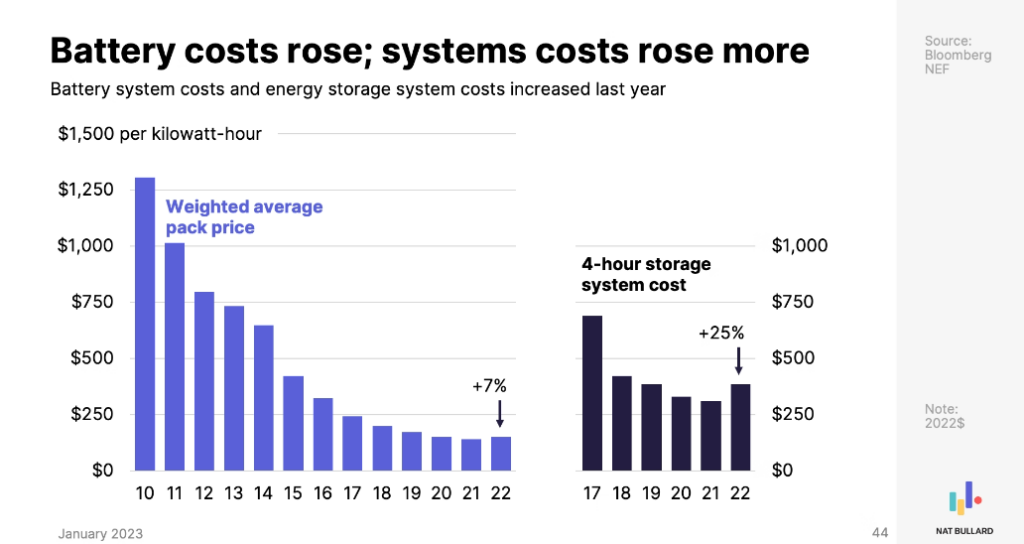

If not planet-changing oil and corn, which chemicals will feed cars? Most of the batteries in EVs—and your smartphones and laptops—are Lithium-ion. Their cathodes are made with nickel, manganese, and cobalt (N, M, and C). An NMC battery provides enough energy density to drive you 300 miles (480 km) on a charge. They had been getting monotonically cheaper with economies of scale and better chemical engineering. But in the past year, for the first time in decades, they started to become more expensive.

Why? Firstly because nickel is mined primarily in Russia and cobalt in the Democratic Republic of Congo. Sanctions against Russia and child labor in the DRC pushed companies to seek alternatives; the auto sector also had concerns about occasional but catastrophic NMC battery fires and the short lifespan of only about a decade.

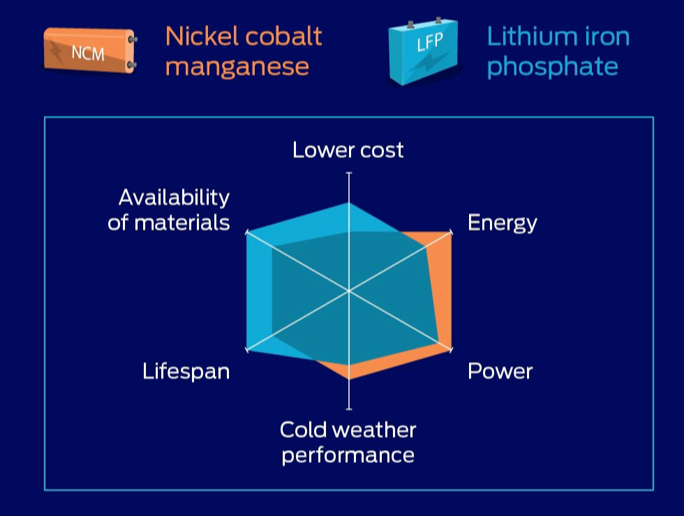

China is leapfrogging the world in battery innovation. Tesla and China’s BYD were among the first EV makers to switch to LFP batteries when nickel became expensive in 2020. The cathodes of an LFP battery use abundant iron (Fe) & phosphate (P) instead of scarce and expensive cobalt & nickel, and have a shorter range than NMC but faster charging. Since the switchover began, LFP’s market share has nearly tripled. In a reversal of decades of green tech knowhow flowing eastwards, Volkswagen in EU and Ford in the US are racing to license LFP battery technology in on-shoring tech-transfer deals with the Chinese battery giant CATL.

Then there is sodium ion: a possible new contender (table salt in cars!) that is cheaper, if for now less energy dense. India’s Reliance bought Faradian last year, while rumors and reports in the EV trade press suggest China’s CATL and BYD are close to selling passenger cars with the much cheaper Na-ion batteries. As commercial competition for the $46 trillion EV market heats up, we can expect automakers to push for battery regulations that hide protectionist aims in recyclability and recoverability standards for certain battery chemistries.

The energy transition is the site of conflict between an old world anchored in stocks and flows of hydrocarbons, and a new world dependent more on manufacturing processes and genuine innovation in energy.

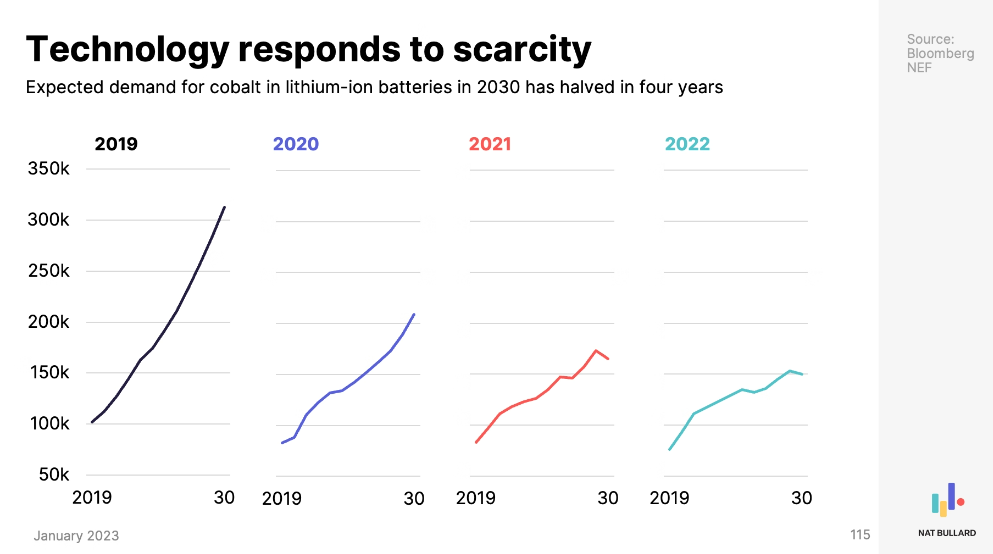

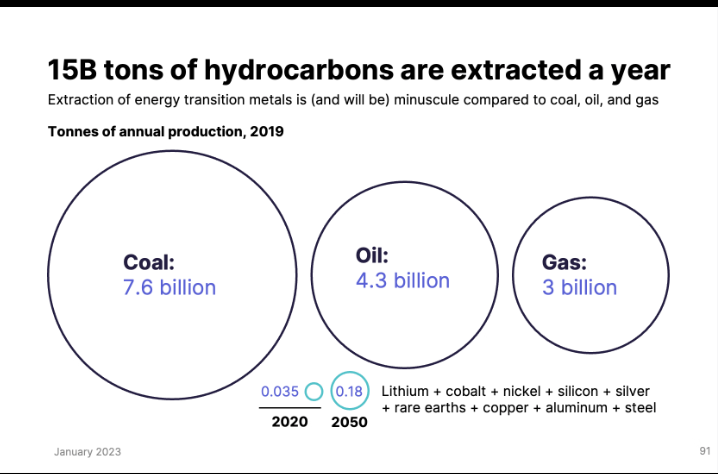

Fears about supply shortages of transition minerals need to be seen against the image of past predictions of cobalt shortages, and the tiny scale of transition minerals versus fossil fuel extraction.

It is true: the energy transition is going to require more mining. But it’s going to be so much less mining than one year of mining coal. An average car burns 17,000 liters of petrol over its life, equivalent to a 25 storey high stack of oil barrels. A EV “consumes” (i.e. after recycling) around 30 kilograms of metals, about the size of a football.

The Polycrisis is a publication focusing on macro-economics, energy security & geopolitics.

Filed Under