October 30, 2025

Analysis

A State-led Financial Empire

The rise and expansion of China's global financial architecture

The United States’ increasing weaponization of global financial interdependency—through sanctions, blacklistings, reserve freezes, and the exclusion of entire states from global payment networks—has revived interest in alternatives to the dollar-dominated financial system across emerging economies. Perhaps the most important response to these policies has come from the People’s Republic of China.

Having long prioritized domestic stability over the pursuit of a global role for the Renminbi (RMB), Beijing has recently accelerated its construction of a parallel financial architecture. Without seeking to fully replace the dollar’s global dominance, it has nevertheless sought to reduce its exposure to US monetary power while embedding its trading partners in RMB-denominated circuits of trade and finance.

Whereas British and US financial dominance relied on open capital markets, private banking networks, and the global expansion of highly financialized instruments—from deep derivatives markets to speculative financial activity increasingly detached from the real economy—China’s strategy is state-led and more functional in orientation. RMB internationalization is more closely organized around trade settlement, investment channels, and funding for production and infrastructure. It deliberately avoids the full liberalization and speculative excesses that have inflated the size of the USD-based system far beyond underlying economic activity. Rather than building vast global capital markets, Beijing constructs controlled channels that facilitate cross-border RMB use while maintaining state oversight. This produces a qualitatively different financial empire: smaller in scale compared to the sprawling dollar system, but informed by trade relations, value chains, and political alliances, and structured around managed connectivity.

These infrastructures are not neutral technical fixes. Their design determines who can access liquidity, how transactions are routed, and under which rules financial activity takes place. By embedding itself as a central node in these networks, China is doing more than internationalizing its currency: it is quietly reshaping the architecture of global finance by enhancing Beijing’s financial autonomy, reducing its exposure to US sanctions and monetary policy spillovers, while binding economic partners in the Global South more tightly to Beijing. The result is an expansive system of influence aiming to position China not as a sole hegemon but as a critical pillar in the new global order that is characterized by a growing fragmentation of financial and economic activity along geopolitical lines.

From integration to fragmentation

Efforts to internationalize the RMB have emerged gradually since the early 2000s. Over the past two decades, they have reflected a persisting tension between China’s growing economic weight and its cautious approach to financial exposure. In the wake of the 1997–1998 Asian Financial Crisis, Chinese policymakers concluded that premature liberalization of capital flows exposed economies to destabilizing volatility. While the renminbi was made convertible for current account transactions in 1996, the capital account remained largely closed. This slow pace stood in stark contrast to China’s rapidly expanding trade footprint, creating a mismatch between its economic scale and the RMB’s international role.

The 2007–2009 Global Financial Crisis marked a turning point. The freezing of dollar liquidity worldwide underscored the risks of a global system dependent on a single reserve currency. In 2009, People’s Bank of China (PBoC) governor Zhou Xiaochuan openly questioned the sustainability of dollar dominance and proposed expanding the role of IMF Special Drawing Rights (SDRs) or establishing a ‘super-sovereign’ reserve currency. The proposal, largely ignored by Washington, revealed a deep frustration in Beijing over the vulnerabilities inherent in a dollar-centric order. While never a top government priority, Chinese technocrats launched a series of pilot programs that laid the groundwork for its wider international use beyond its borders.

The years leading up to 2016 were the high point of integration. With reforms to its exchange rate regime, a gradual widening of QFII quotas, and the creation of offshore RMB hubs in Hong Kong, London, and Singapore, the RMB’s global profile rose significantly. This culminated in its inclusion in the IMF’s SDR basket in October 2016, a milestone that appeared to validate China’s efforts to secure recognition for its currency within the existing global monetary order.

Yet, behind the scenes, tensions were already mounting. US authorities maintained tight control over dollar clearing networks—centralized in US-regulated infrastructures like CHIPS and Fedwire—and have repeatedly demonstrated their ability to deny access to foreign banks or entire states, turning dollar settlement into a geopolitical lever. At the same time, Federal Reserve swap lines remained largely restricted to advanced economies, excluding China and other emerging markets, reinforcing asymmetric access to the core of the dollar system. Meanwhile, speculative inflows into China’s stock market and a turbulent 2015–2016 devaluation episode triggered massive capital flight, leading Beijing to reassert strict capital controls. This underscored the incompatibility between full RMB internationalization on US-style terms and China’s priority of maintaining domestic monetary stability.

The post-2016 period has been defined by growing geopolitical confrontation and partial decoupling. The weaponization of the dollar—through sanctions on Chinese partners like Iran, the freezing of Russian reserves, and the exclusion of Russian banks from SWIFT—highlighted how financial infrastructures could be used as tools of coercion. For Beijing, these events reinforced the need to develop RMB-based alternatives that could shield China and its partners from such vulnerabilities. Attempts at cooperation on global reforms, such as expanded SDR issuance or multilateral payment initiatives under the G20, have repeatedly stalled in the face of US reluctance to dilute its monetary power.

The result has been a strategic pivot: rather than seeking to integrate into the existing dollar system, China has focused on building a parallel set of infrastructures—anchored around its own trade networks and political partners, particularly in Southeast Asia, the Middle East and other parts of the Global South—that could sustain cross-border RMB use on their own terms. This new strategy unfolded across three functional domains: payments, investment and funding. Together, they form the backbone of an emerging Sino-centric financial system. Each represents a deliberate effort to bypass US-controlled channels, insulate China from external monetary coercion, and weave Chinese partners more tightly into RMB-based networks.

Payments

Since the Global Financial Crisis, China has undertaken a deliberate and incremental strategy to build payment infrastructures that support RMB-denominated transactions, bypassing US-controlled clearing networks where necessary and reducing exposure to Western financial coercion. These infrastructures are designed to create the conditions for a broader RMB-based financial ecosystem, offering partners alternative channels for trade settlement while maintaining China’s ability to tightly manage cross-border capital flows.

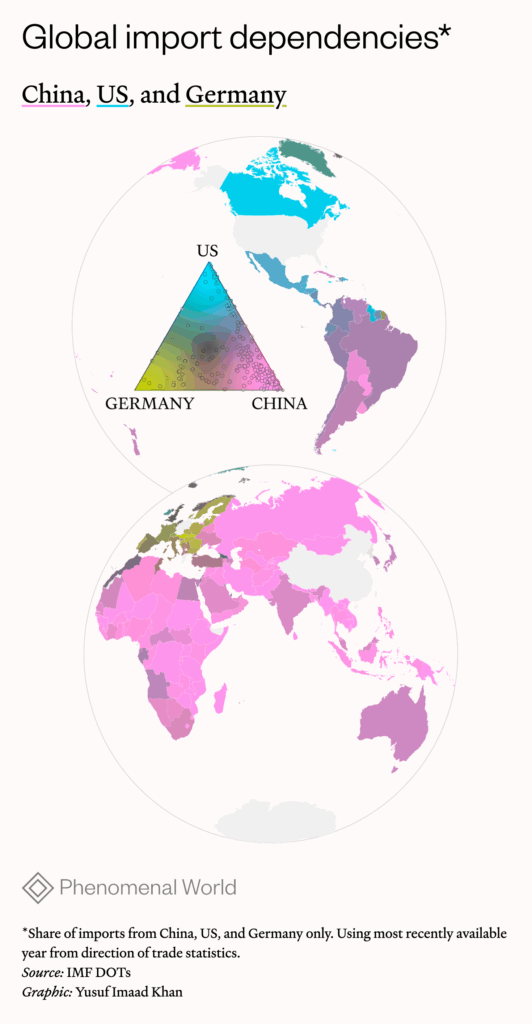

The motivation behind this strategy is clear: although China has become the world’s largest trading nation (by 2023, it was the largest trading partner for 120 countries) the RMB’s share of global trade settlement remains limited. RMB trade has remained overwhelmingly denominated in USD, and Chinese trade itself has long been overwhelmingly invoiced in dollars.

To address this, Chinese policymakers have actively pursued the creation of state-backed financial infrastructures that facilitate RMB payments, ensuring that companies and financial institutions across the world can easily conduct transactions in the Chinese currency, while maintaining a relatively controlled capital account. Several key infrastructures have been developed to facilitate cross-border RMB payments, each contributing to the gradual expansion of the currency’s role in international trade, and at each step of the way, these infrastructures have become more accessible to countries seeking an alternative to the Dollar trade.

The first major step in this process was the introduction of the Cross-Border RMB Trade Settlement Pilot Scheme in 2009. This initiative initially allowed a select group of Chinese companies to settle trade transactions in RMB with designated partners in Hong Kong, Macau, and ASEAN nations. This framework created a legal and institutional foundation for RMB payments outside of China for the first time. Over time, as Chinese authorities gained confidence in the system and ensured that it did not destabilize domestic monetary policy, the program was expanded nationwide in 2012, allowing all Chinese firms to settle any type of cross-border transaction in RMB with partners worldwide.

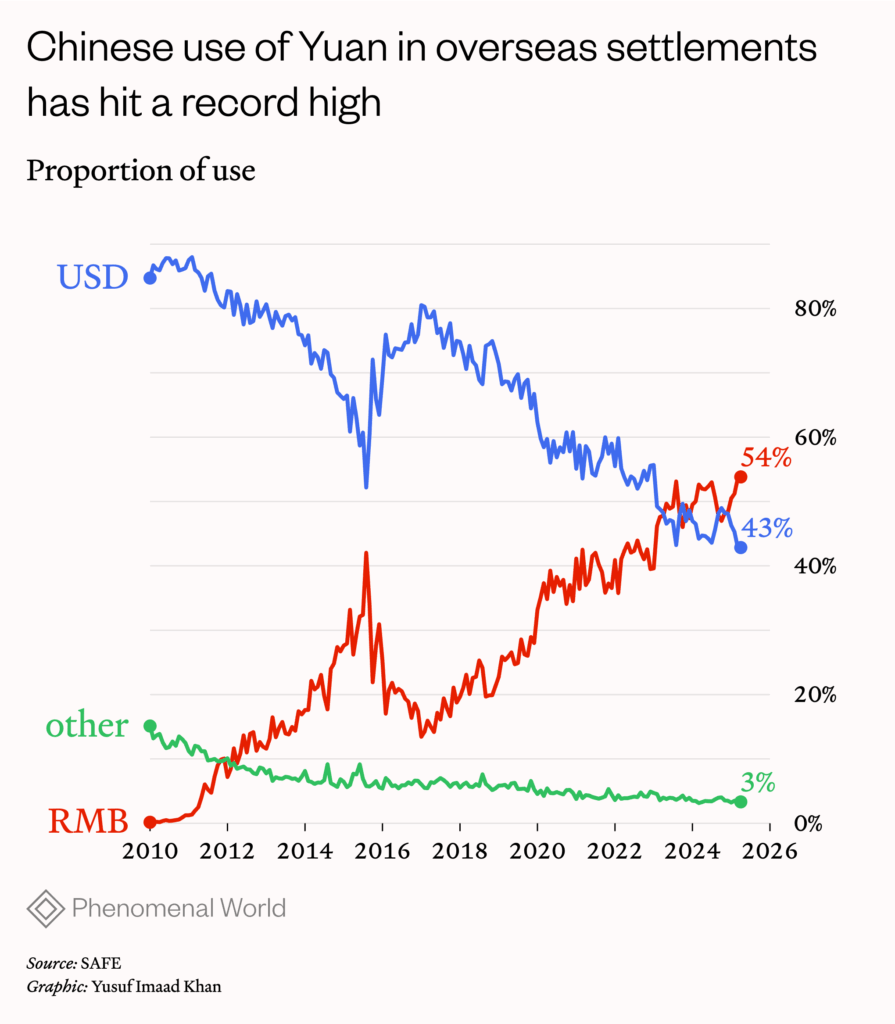

Beyond its technical impact, the scheme began to normalize RMB use in global trade relations, laying the groundwork for a gradual shift away from dollar-denominated invoicing and giving Beijing a first tool to strengthen monetary ties with its trading partners. The impact of this reform has been substantial. While cross-border payments in RMB were virtually non-existent in 2010, by March 2025 the RMB accounted for 54.3 percent of China’s total trade settlement.

A second major step was the establishment of offshore RMB clearing banks. Clearing banks serve as designated financial institutions that facilitate RMB transactions in foreign jurisdictions, allowing overseas banks to settle RMB transactions efficiently without needing direct access to China’s domestic financial system. This model significantly improved transaction efficiency by eliminating reliance on traditional correspondent banking networks, which had previously slowed transaction times and increased costs. First established in Hong Kong in 2003, China rapidly expanded its clearing bank network. By November 2024, offshore RMB clearing banks had been established in 33 economies, including London, Singapore, Frankfurt, and New York.

These hubs not only reduced transaction costs but also anchored RMB liquidity pools abroad, effectively extending China’s monetary reach without dismantling its capital controls. Each clearing bank agreement represents a negotiated institutional link to Beijing’s financial system, incrementally building the infrastructure for a Sino-centric payments network. The growth of offshore clearing banks has played a crucial role in fostering a liquid offshore RMB market. These banks provide local financial institutions with access to RMB settlement, reducing the need for foreign exchange conversion and helping businesses conduct trade with China in its own currency. Clearing banks have become a key driver in increasing RMB-denominated trade globally.

Beyond offshore clearing banks, however, China also sought a more comprehensive infrastructure to further streamline RMB payments. In 2015, it launched the Cross-Border Interbank Payment System (CIPS)—a centralized platform that enables direct clearing and settlement of RMB transactions worldwide. While it launched with just 19 direct participants and 176 indirect participants, by 2024, it had expanded to 168 direct participants and 1,461 indirect participants from 117 countries. This infrastructure has facilitated over 8.9 million transactions totaling USD 23.1 trillion, with 62 percent of transactions originating outside China. CIPS is more than a technical upgrade to global payments—it represents an institutional alternative to Western-dominated infrastructures like SWIFT and CHIPS. This gives China a growing ability to conduct and settle trade flows beyond the reach of US monetary and sanctions power. While CIPS remains significantly smaller than its USD-based counterparts, its rapid growth illustrates its potential as an alternative global payment system. Importantly, major Western financial institutions, including Deutsche Bank, BNP Paribas, and Standard Chartered, have all joined CIPS, signaling its growing relevance in global finance.

Yet, the latest—and potentially most disruptive—development in RMB payment infrastructure is Project mBridge, a multi-central bank digital currency (CBDC) platform initiated by China, Thailand, Hong Kong, the UAE, and the BIS. Unlike traditional payment systems, mBridge is built on blockchain-based technology and enables real-time, direct cross-border settlement between CBDCs, bypassing conventional banking networks. A primary objective of mBridge is to eliminate reliance on the USD in international trade transactions. Unlike existing systems where cross-border payments require intermediary banks and multiple currency conversions (often through USD), mBridge allows direct RMB settlements between central banks and commercial banks. By creating payment channels that operate outside Western-controlled clearinghouses, Beijing is testing the foundations of a parallel digital monetary network that could, over time, give participating economies a viable escape route from dollar dominance.

The geopolitical implications of mBridge are significant. The inclusion of Saudi Arabia in 2024 suggests that China may be laying the groundwork for non-USD oil transactions, a longstanding strategic objective. This project also provides a potential model for sanction-resistant payment infrastructure, allowing participating countries to settle transactions outside the influence of Western financial institutions. While the RMB remains underutilized in Europe and North America, its adoption and use has accelerated in Latin America, Africa, and Asia. Recent trends in commodity trade settlement, such as RMB-settled LNG transactions with the UAE, underscore how financial infrastructure is advancing de-dollarization efforts, particularly among countries wary of U.S. financial sanctions. However, RMB transactions to date remain largely bilateral with China, with minimal third-country use outside specific cases (that often involved sanctioned countries like Russia).

The expansion of RMB payment infrastructure is central to China’s long-term financial strategy. By creating a global network of clearing banks, interbank payment systems, and digital currency platforms, China has built the foundations for an RMB-based international financial system. These infrastructures are instruments of financial statecraft. They not only facilitate the RMB’s practical use but also strengthen China’s financial autonomy by reducing reliance on USD-based networks. While the RMB is still far from replacing the USD as the dominant global currency, the architecture for an alternative system now exists, giving Beijing both optionality in future crises and growing leverage over the terms of global payments.

Financial infrastructures

Many commentators argue that China’s restricted capital account continues to hinder its internationalization. Yet this view underestimates Beijing’s deliberate strategy to internationalize on its own terms. Rather than replicating US-style open and speculative capital markets, China has built a state-managed infrastructure that selectively connects foreign investors to its domestic markets. These tightly controlled channels allow cross-border investment to grow without surrendering monetary sovereignty—advancing RMB internationalization while preserving the political and regulatory autonomy that underpins China’s distinct form of financial empire.

Initially, China’s capital markets were largely isolated from global finance. Foreign investors had minimal access to RMB-denominated assets, with early mechanisms like the B-share market and offshore listings operating in a separate system without directly integrating RMB assets into global investment flows. However, beginning in the mid-2000s, China shifted toward a managed opening, introducing a series of controlled mechanisms that enabled foreign investors to participate in its domestic markets. These reforms were not designed to mimic Western capital mobility but to test, calibrate, and scale access in ways that served domestic priorities while gradually positioning the RMB as an investable currency globally.

The first major initiative was the establishment of the Qualified Foreign Institutional Investor (QFII) program in 2002, which allowed licensed foreign institutions to invest in China’s stock and bond markets under strict quota limits. This was followed by the Renminbi Qualified Foreign Institutional Investor (RQFII) program in 2011, which allowed offshore RMB to be reinvested into onshore capital markets, leveraging the growing pool of RMB held outside China. While these quota-based systems marked an initial step toward financial integration, they remained highly restrictive, requiring approvals, imposing repatriation limits, and constraining trading activities. Rather than liberalizing rapidly, Beijing designed these schemes to bring in long-term, stable investors on its own terms.

While QFII was originally underutilized, a turning point came in 2014 with the introduction of Stock Connect, a cross-border trading mechanism linking the Shanghai and Hong Kong stock markets. Unlike the quota-based QFII and RQFII schemes, Stock Connect provided a more seamless and scalable channel for foreign investors to access China’s A-shares, significantly reducing barriers to entry. International investors could now buy eligible Chinese stocks through a special purpose vehicle in Hong Kong, while Chinese investors could access Hong Kong-listed equities through the same mechanism. The design of Stock Connect allowed for more efficient transactions, eliminated the need for upfront quota approvals, and ensured a steady flow of foreign capital into China’s markets. By 2023, foreign investors accounted for approximately 7 percent of trading in China’s stock markets, a sharp increase from just 0.6 percent in 2014. This again advanced RMB internationalization, not by liberalizing markets wholesale, but by creating controlled conduits that preserved Beijing’s oversight of cross-border flows and thereby reinforcing its vision of a state-led financial empire.

Following the success of Stock Connect, similar infrastructures were developed for bond markets. In 2016, the China Interbank Bond Market (CIBM) Direct program was introduced, allowing foreign institutions, including central banks and commercial banks, to invest in Chinese bonds without requiring prior regulatory approval. This was supplemented by the launch of Bond Connect in 2017, which provided an even more seamless route for international investors to access China’s bond markets through established global trading platforms such as Bloomberg and Tradeweb. The introduction of these infrastructures led to a significant increase in foreign ownership of Chinese government bonds, which rose from 0.3 percent in 2012 to eleven percent by 2021. These mechanisms expanded access to RMB-denominated debt while keeping capital flows firmly within a framework designed by Chinese regulators.

A key feature of these infrastructural arrangements is their design as “closed-loop” systems, deliberately constructed to allow participation in China’s markets without ceding control over the broader capital account. While they enable foreign investment in RMB assets, they maintain capital controls by restricting the free movement of funds beyond designated investment channels. This approach allows China to attract foreign capital while minimizing risks associated with speculative flows and financial instability. Moreover, China extended its Connect model to other asset classes, such as exchange-traded funds (ETFs), wealth management products, and interest rate swaps. This has been further complemented by the development of RMB-denominated financial instruments, including stock indices, futures, and cross-currency hedging tools, especially in Hong Kong, which provide international investors with greater flexibility in managing their exposure to Chinese assets.

While geopolitical tensions have led to fluctuations in foreign investment flows—particularly among U.S. investors—the broader trajectory of RMB asset internationalization has continued. In recent years, a decisive shift has occurred in the geography of RMB investments, with non-Western financial institutions, especially those from the Middle East and Southeast Asia, expanding their allocations to Chinese markets.

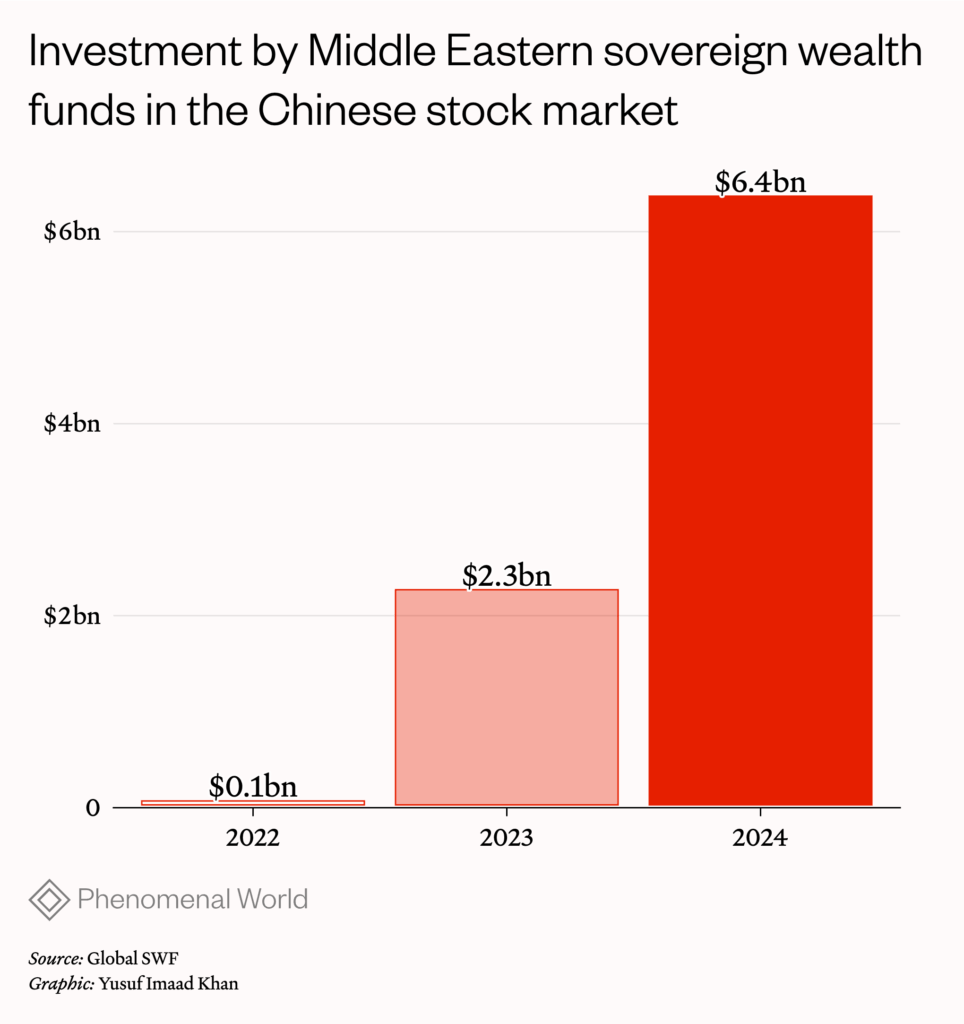

Sovereign wealth funds from Singapore, Abu Dhabi, and Kuwait have emerged as major investors in Chinese stock and bond markets, with Middle Eastern sovereign wealth funds alone channeling over USD six billion into Chinese equities in 2024, up from just 100 million two years earlier. This was also accompanied by cross-listing of ETFs and other financial products, the mutual opening of branches and accelerating financial diplomacy. This changing investor base reflects more than portfolio diversification: it mirrors Beijing’s deliberate strategy of fostering capital linkages with economies already tied into its trade and infrastructure networks, building an RMB investor ecosystem outside Western-dominated financial circuits. Meanwhile, US investors have faced growing regulatory pressure to reduce their exposure to China, with Washington imposing sanctions on Chinese companies and pressuring index providers to exclude Chinese assets. These diverging investment flows underscore how RMB asset internationalization is increasingly anchored in a multipolar, geopolitically fragmented financial order.

Through the development of these financial infrastructures, Beijing has laid the foundations for a distinct, state-managed model of currency internationalization. While de jure its capital account remains restricted, the combination of Connect programs, bond market access schemes, and offshore RMB markets has enabled a level of de facto global integration without relinquishing domestic control. As these systems continue to grow—particularly among non-Western financial actors—they provide the necessary conditions for a wider role of the RMB in global investment flows, gradually reinforcing China’s financial influence in an increasingly multipolar world.

Funding

The construction of financial infrastructures for RMB-denominated financing also plays a crucial role in advancing the currency’s internationalization. Rather than building vast, speculative offshore credit markets as in the U.S.-dollar system, China has pursued a functional, state-managed approach focused on trade, infrastructure, and productive investment. Through the development of panda bonds, dim sum bonds, and bilateral swap lines, China has created mechanisms that facilitate the accumulation, circulation, and liquidity of RMB liabilities beyond its domestic financial system. These infrastructures allow foreign borrowers to access RMB funding, expand the pool of RMB-denominated assets, and provide financial stability measures that encourage the broader use of the currency. While the RMB’s role as a global funding currency remains small, these infrastructural developments have laid important groundwork for its future expansion.

The introduction of panda bonds has enabled foreign corporations, financial institutions, and governments to raise RMB capital within China’s domestic market. Initially constrained by regulatory uncertainty and capital controls, a series of gradual reforms—including clearer issuance rules and the removal of restrictions on repatriating funds—have expanded the market’s appeal. Early issuances were small and experimental, but have grown in scale and scope: in 2016, Poland was the first European state to issue a sovereign panda bond, and in 2023 Hungary used the bonds to fund Belt and Road infrastructure projects, with the proceeds partially used to pay Chinese contractors in RMB. Foreign firms such as Mercedes-Benz, HSBC, and Trafigura began to issue panda bonds in early 2025, taking advantage of low Chinese rates and hedging against Western financial risks. Each issuance strengthens the ecosystem of RMB-denominated assets, creating more opportunities for foreign entities to fund themselves within China’s financial architecture.

The dim sum bond market, launched in Hong Kong in 2007, provides a complementary offshore channel, with bonds issued in financial hubs like Hong Kong, London, and Luxembourg. Initially dominated by Chinese state-owned banks, it gradually attracted multinational issuers like McDonald’s (2010) and HSBC (2012), testing global demand for RMB-denominated debt outside mainland China. Dim sum bond issuance nearly tripled from around USD 18 billion in 2022 to USD 34 billion in 2023, driven not only by Chinese issuers but also a growing share of foreign corporations and sovereign entities tapping Hong Kong’s offshore RMB market. In particular, non-financial corporations outside China expanded their dim sum issuance fivefold over the 2020–2024 period, reflecting a deliberate turn toward RMB funding to support trade, investment, or regional diversification strategies. Both panda and dim sum markets remain small compared to dollar or euro bond markets, but they embed cross-border credit relations in RMB, allowing borrowers to diversify away from dollar funding while increasing their reliance on Chinese financial institutions and investor pools.

Beyond bond markets, China’s network of bilateral swap lines has become a cornerstone of its RMB funding strategy. Unlike the swap arrangements offered by the U.S. Federal Reserve, which are largely limited to advanced economies and designed for crisis liquidity, China’s swaps serve a dual function, providing RMB liquidity during periods of market stress and backstopping cross-border RMB transactions. This dual function enables regular RMB-denominated trade and investment settlements between participating economies.

Notably, China’s RMB liquidity networks are in Asia, Africa, Latin America, and the Middle East. This geographic shift reflects a broader pattern in China’s financial diplomacy—strengthening RMB adoption in regions where demand for alternatives to the dollar is highest and where China is a dominant trading partner. By guaranteeing RMB access in periods of volatility or despite sanctions pressure, these swap lines entrench China’s role as a financial backstop for non-Western economies, weaving them more tightly into RMB-centric networks.

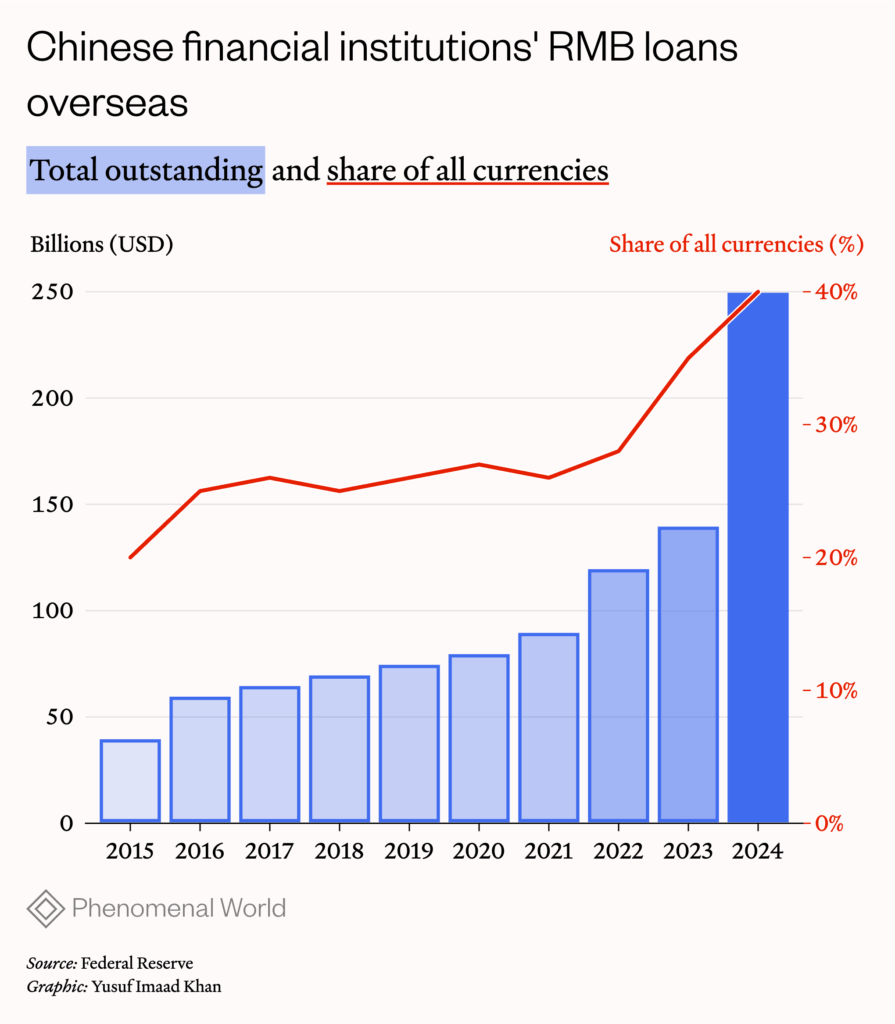

Based on growing offshore capital pools and central bank backstops, Chinese banks have in recent years rapidly increased the issuance of RMB-denominated loans while simultaneously scaling back dollar lending. Between 2015 and 2024, Chinese financial institutions’ RMB lending increased from seven percent to forty percent of overseas loans, with an especially sharp increase after 2022. This had a significant global impact, with total dollar lending to emerging market economies declining by ten percent between 2022 and 2024.

Beyond credit channels, Beijing has begun to link RMB to gold as a trusted reserve asset. In June 2025, the Shanghai Gold Exchange opened its first international gold vault in Hong Kong, alongside new RMB-denominated gold contracts, settled either in cash or physical delivery offshore. This setup allows global investors to convert offshore RMB directly into physical gold, effectively providing a gold-backed mechanism for RMB holdings outside mainland China. By linking the Yuan to a trusted reserve asset, Beijing strengthens international confidence in its currency, adding a quasi-safe-haven function to offshore RMB markets. This initiative complements panda and dim sum bonds, encouraging investors to hold RMB while retaining the option of redemption into gold. As part of a broader state-led effort to build RMB-denominated funding markets, the Hong Kong gold vault extends China’s financial infrastructure beyond credit and swap lines into reserve asset security, deepening the structural appeal of RMB funding. This directly supports de‑dollarization efforts by enabling gold imports and settlements in RMB rather than dollars, representing a powerful extension of China’s financial expansion.

These infrastructures contribute to a reinforcing cycle—expanding the presence of RMB-denominated assets while ensuring the liquidity required to sustain and grow their adoption in global markets. Rather than replicating the deep, speculative funding markets underpinning the US dollar’s dominance, Beijing is building a more functional and strategically targeted ecosystem, closely tied to trade, infrastructure, and productive investment. As China deepens its financial ties with the Global South, these funding mechanisms position the RMB as an increasingly relevant currency in non-Western financial circuits, gradually consolidating Beijing’s centrality in global financial flows.

A Sino-centric financial empire?

Over two decades, the RMB project has evolved from a tentative attempt at integration into the US-dominated order to a deliberate effort to rewire monetary and financial connectivity on Beijing’s terms. The result is not a bid for outright replacement of dollar hegemony, but the gradual construction of a parallel financial architecture—one that reduces China’s exposure to U.S. monetary coercion while binding its trading partners into RMB-denominated trade, investment, and funding networks.

As China’s financial architecture matures, what emerges is not merely a strategy for currency internationalization, but the scaffolding of a broader geopolitical project. Corresponding with other areas like supply chains, digital infrastructures, resources or green technology, this is a project of empire building, creating a network of asymmetric economic connectivity centred around a dominant core.

In the case of RMB internationalization, offshore clearing hubs, investment channels, swap networks, and digital payment platforms rewire cross-border finance in ways that enhance Beijing’s autonomy and create new dependencies for its partners, especially across the Global South. Participation in China’s growing economic sphere increasingly implies participation in its financial sphere, where access to liquidity, settlement systems, and investment flows are intermediated by Chinese institutions and rules.

The deliberate buildout of RMB infrastructure—from clearing banks to mBridge and commodity pricing mechanisms—has established alternative channels that bypass Western-controlled systems. As China consolidates its role as a dominant trading partner for emerging markets, these infrastructures provide the foundation for growing RMB internationalization. While displacement of the U.S. dollar remains unlikely, and is not Beijing’s immediate objective, China’s parallel financial system offers it and its partners a managed pathway to greater financial autonomy while tightening their structural ties to Beijing.

This emerging financial system differs fundamentally from its liberal precedents. Whereas US financial dominance was built on open capital markets, institutional dominance, and a vast ecosystem of highly financialized instruments detached from real production, China’s strategy is state-led, functional, and deliberately restrained. RMB internationalization is primarily tied to trade, infrastructure financing, and productive investment, avoiding the speculative excesses that have inflated the scale of the dollar system far beyond underlying economic activity. The result is a smaller, more targeted financial network that embeds China at its center.

The Global South is central to this project. Through swap lines, RMB bond markets, and partial acquisitions of stock exchanges in places like Pakistan, Kazakhstan or Bangladesh, Beijing is exporting regulatory frameworks, trading rules, and market infrastructures that reorient capital flows toward China-led systems. Cross-border capital platforms, RMB bond issuance, and settlement mechanisms gradually tether emerging economies to China’s institutions, shifting financial influence away from Western networks.

Historically, financial empires shaped global capital flows by controlling trade, credit, and reserve structures. While China’s approach mirrors this logic, it is constructing an alternative financial architecture that strengthens its centrality internationally while preserving regulatory control domestically, representing a more managed, state-led approach to financial internationalization.

China is not building a dollar-style empire of sprawling markets and speculative finance. It is constructing something leaner, more functional, and tightly managed—a financial order that underwrites trade, infrastructure, and productive investment while insulating Beijing from US leverage. The future trajectory of this system remains uncertain. Its growth will depend on how many countries choose to integrate into these parallel channels. Yet the underlying infrastructures are now firmly established. Whether complementary to or competing with the dollar system, this embeds China as a central node in an increasingly fragmenting global monetary order—quietly redrawing the map of financial power.

Further Reading

Global BYD

The international expansion of Chinese electric vehicles

Amid the intensifying retreat of American hegemony, an alternative geo-economic and geopolitical arrangement is coming into view: a battery-powered globalization with Chinese characteristics. Chinese EV...

The Visible Hand

China’s investments into research and development

China has transformed into a leading force in science, technology, and innovation (STI). With rapidly rising research and development (R&D) expenditure, a larger and increasingly...

Parallel Systems

China, the IMF, and the future of sovereign debt financing

At the start of her three-nation tour of Africa this January, US Treasury Secretary Janet Yellen spoke to the Associated Press in Senegal, bemoaning the...