May 23, 2025

Analysis

After Impeachment

Economic stagnation and political crisis in South Korea

Korea remains engulfed in political turmoil following the declaration of martial law on December 3 and the subsequent presidential impeachment by the National Assembly. Former President Yoon Suk Yeol, arrested and detained on January 19, is now on trial in the Constitutional Court. His resistance to investigation incited public outrage and heightened fears about the impact of the political crisis on the economy. Meanwhile, conservative factions and the political right wing have rallied against his impeachment, leaving Korean society deeply polarized. On April 4, the Constitutional Court finalized Yoon’s removal after a lengthy impeachment trial, and on June 3, South Koreans are slated to elect a new president.

The ongoing political instability has exacerbated longstanding structural challenges in South Korea’s economy. A poster child of late twentieth century democratic transitions, hailed for its export-oriented growth model, Korea now confronts democratic backsliding and economic stagnation. A robust program of public investment is needed to shift this course.

Crisis and impeachment

By most accounts, President Yoon Suk Yeol’s declaration of martial law on December 3, 2024, represented a desperate attempt to deflect attention from the corruption allegations and plummeting approval ratings that plagued his government. Claiming that the elections were rigged by hackers linked to North Korea and China, he deployed soldiers to the National Election Commission and the National Assembly—a move that was overturned by the National Assembly within two hours. Thousands of citizens gathered to protest, confronting soldiers and demonstrating a collective resolve to safeguard democracy at the National Assembly on the night Yoon declared martial law. The Assembly formally impeached Yoon on December 14, with twelve members of his own party voting in favor. That day, a massive protest underscored resistance to Korean authoritarianism.

Despite the protests, Korea’s political condition is far from encouraging. For one, the investigation and arrest of Yoon took a long time due to his resistance, and the ruling elite stalled his impeachment. Han Duck-Soo, the acting president and former prime minister, was himself impeached by the opposition for refusing to appoint the constitutional judges needed to finalize the impeachment process. Furthermore, opposition leader Lee Jae-Myung has faced his own swath of legal scandals, including accusations of electoral and financial mishandling.

And since the impeachment, Yoon’s conservative party has only increased its popular appeal, by shifting further to the extreme right and opposing his impeachment. Although the ruling party’s approval ratings sank during the impeachment process in mid-December 2024, they have since surged, nearly surpassing those of the liberal opposition by late January 2025. Public support for Yoon’s impeachment has also declined, dropping from 75 percent to 59 percent, while opposition to his impeachment has risen from 21 percent to 36 percent over the same period, according to Gallup Korea.

The reality is that the impeachment process and coming elections are unlikely to resolve the structural challenges facing Korean democracy. Since its division from communist North Korea, South Korea has been governed by a right-wing governing coalition that repressed democratic mobilization and labor movements but maintained public support with rapid industrialization and economic growth.

With its first direct presidential elections held in 1987, the liberal opposition party only came to power in 1997. Since democratization, the conservative party has maintained its lead over the Liberals in general elections. Despite the Liberals’ landslide victory in the general election in 2024, the conservative tradition has remained powerful, bolstered by the support of large businesses, influential conservative media, intellectual elites, and entrenched bureaucratic networks.

The recent rise of far-right rhetoric, fueled by fears of losing conservative control, has further polarized the political landscape. The violent unrest after Yoon’s impeachment could lead to a kind of political cold war in Korea. How this crisis unfolds will undoubtedly shape Korea’s trajectory, both as a democracy and an economic powerhouse.

A fragile economy

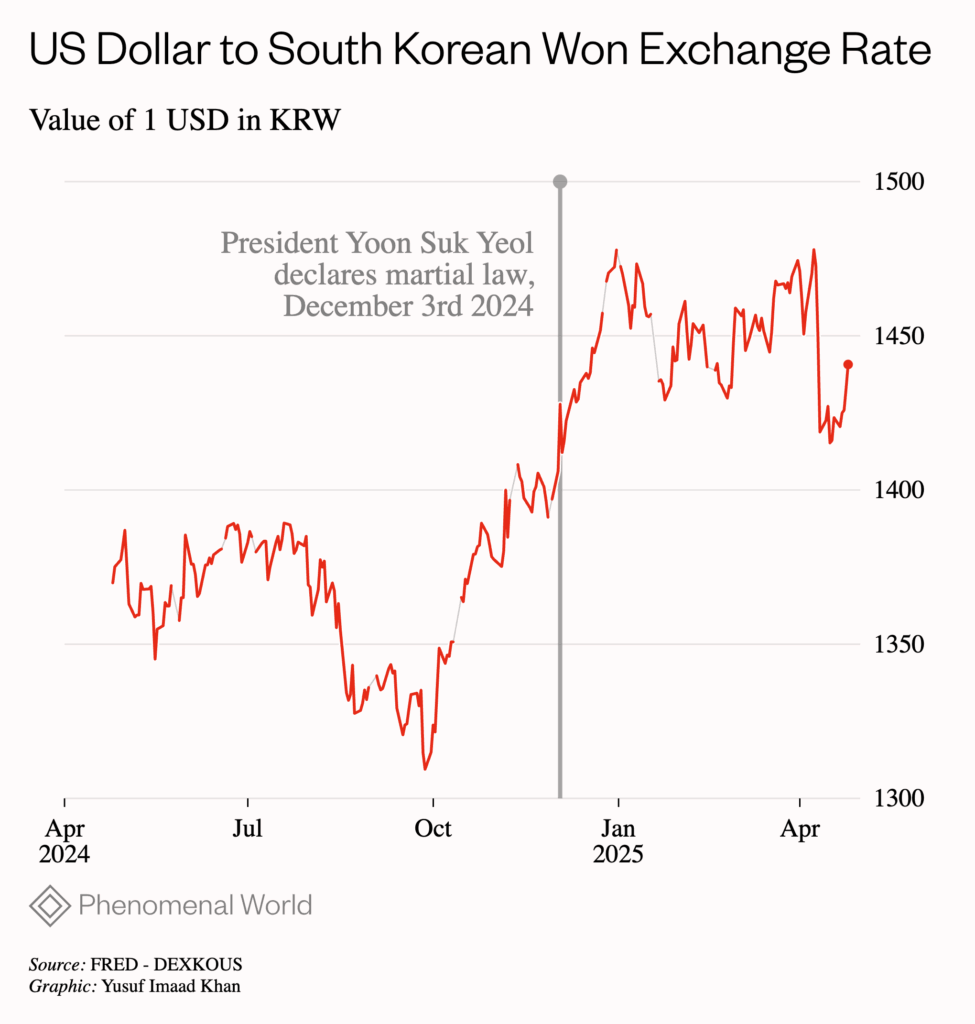

Though the Korean stock market has recovered after a successful impeachment vote in the National Assembly, the Korean won sharply declined from 1,406 won per dollar on December 2 to 1,478 by December 31. During a meeting with Acting President Choi Sang Mok in January, global credit rating agencies expressed heightened concerns about the prolonged uncertainty. A vice president at Moody’s Sovereign Risk Group remarked that “prolonged disruption to economic activity or weakening consumer and business sentiment would be credit negative.” In practice, foreign portfolio investment recorded a net outflow of $3.9 billion in December 2025—the largest amount since the Covid-19 pandemic.

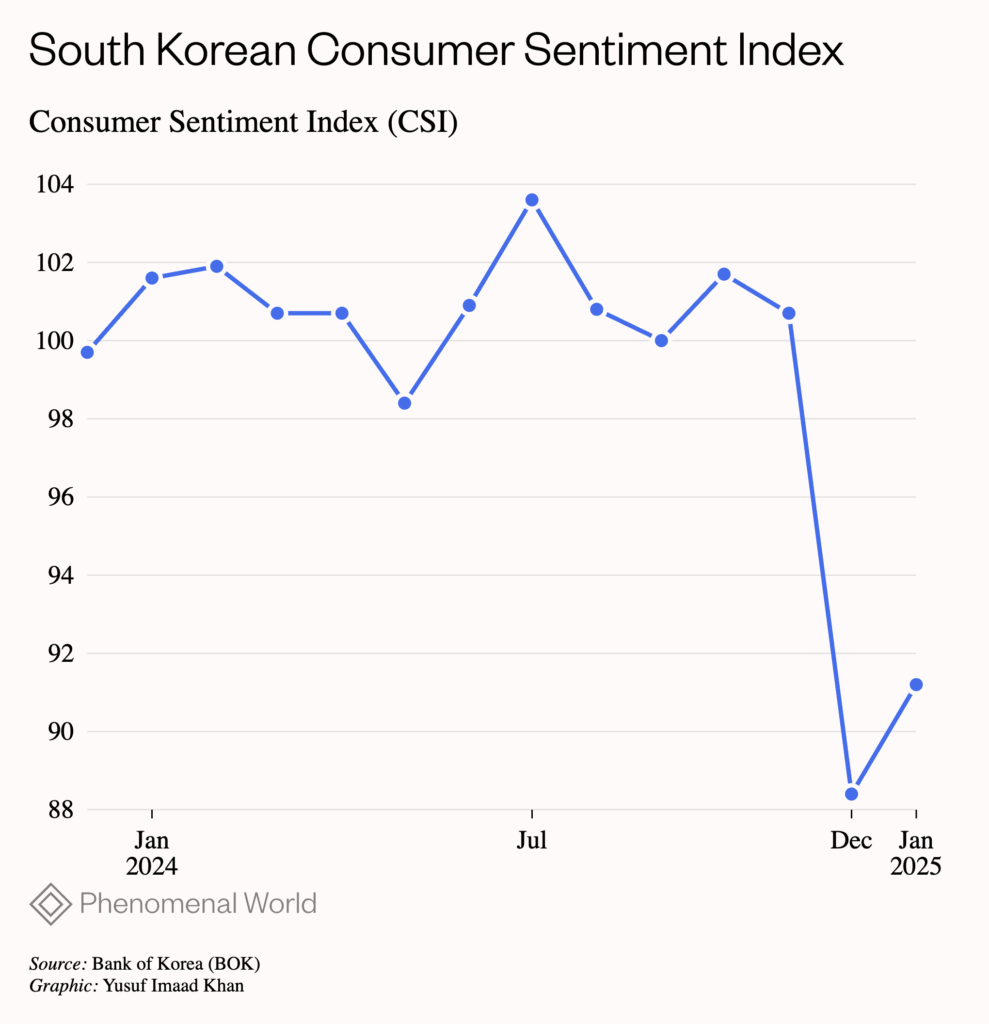

The negative economic impact of the political crisis is evident in stagnating domestic consumption. As the figure below demonstrates, Composite Consumer Sentiment Index has fallen rapidly since December 2024.

The retail sales index has also fallen 2.1 percent since December 2023, according to Statistics Korea. This downward trend is unlikely to reverse until the impeachment process concludes.

The current turmoil has already dampened corporate investment, with corporate lending declining since December 2024. Business sentiment has also worsened, with the Composite Business Sentiment Index for all industries falling from 91.8 in November 2024 to 87.3 in December 2024 and 85.9 in January 2025, according to the Bank of Korea (BOK). The overall Economic Sentiment Index, which includes both businesses and consumers, also showed a decline in December. Finally, the Business Survey Index (BSI), which reflects the real situation of businesses, dropped in December. These trends paint an overall picture of stagnating investment.

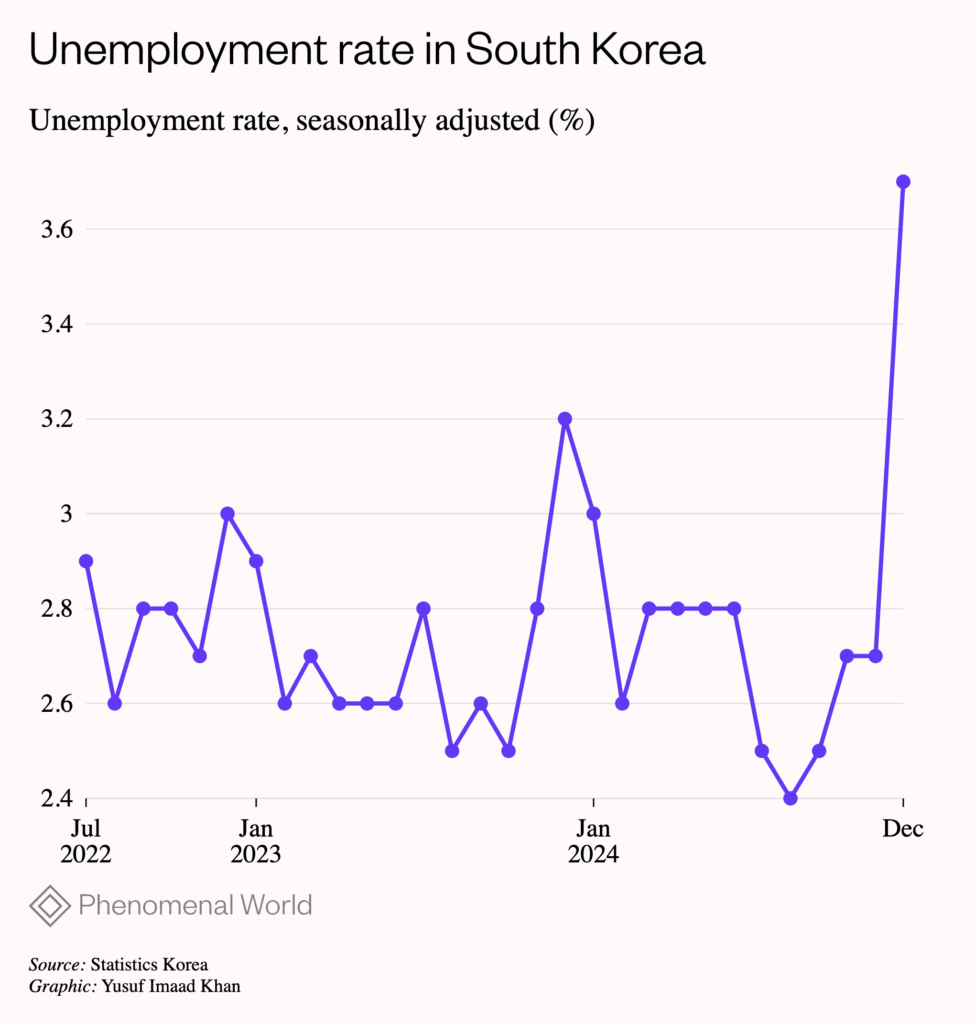

Labor markets are also feeling the impact. Employment numbers for December fell compared to the same month of the previous year, and the seasonally adjusted unemployment rate rose to 3.7 percent—the highest since December 2021. This marks a 1 percentage point increase from November and a 0.5 percentage point rise compared to December 2023.

These rather momentary trends are part of a broader economic slowdown. The annual real GDP growth rate for 2023 stood at only 1.4 percent. And while the quarterly real GDP growth rate rebounded to 1.3 percent in the first quarter of 2024, it fell to -0.2 percent in the second quarter and remained weak at 0.1 percent in the third and fourth quarters, reflecting sluggish domestic demand and a recent decline in exports. Private consumption contracted by 0.2 percent in the second quarter compared to the previous quarter, primarily due to stagnant real wages. Meanwhile, construction investment and exports declined by 3.6 percent and 0.2 percent, respectively, in the third quarter. Notably, net exports contributed a negative 0.8 percentage points to economic growth in the third quarter.

The stagnation continued in the fourth quarter, with domestic consumption and construction investment growing by just 0.2 percent and contracting by -3.2 percent, respectively. As a result, the quarterly growth rate in the fourth quarter was a mere 0.2 percent, reflecting the worsening economy, partly due to the political crisis. The annual economic growth rate for 2024 is now expected to be 2 percent, lower than the earlier projections by the Korean government and the Bank of Korea (BOK). The performance of both the stock market and the currency in 2024 has also underperformed compared to major economies.

The numbers suggest that the Korean economy faces challenges on two fronts: weak domestic demand, driven by stagnating real wage growth, and looming difficulties in the external sector, linked to changes in the global economy. Real wage growth has been negative in 2022, 2023, and the first quarter of 2024, exerting pressure on domestic consumption. The government’s fiscal austerity policies have only worsened the situation. Small business owners, particularly those in restaurants and retail, are bearing the brunt of the downturn in private domestic consumption, with a recent rise in bankruptcies.

Annual and Quarterly Economic Growth in Korea (%)

| 2023 | 2024 | 2024/Q1 | 2024/Q2 | 2024/Q3 | 2024/Q4 | |

|---|---|---|---|---|---|---|

| GDP | 1.4 | 2 | 1.3 | -0.2 | 0.1 | 0.1 (1.2) |

| Private Consumption | 1.8 | 1.1 | 0.7 | -0.2 | 0.5 | 0.2 (1.2) |

| Government Consumption | 1.3 | 1.7 | 0.8 | 0.6 | 0.6 | 0.5 (2.7) |

| Construction Investment | 1.5 | -2.7 | 3.3 | -1.7 | -3.6 | -3.2 (-5.3) |

| Facilities Investment | 1.1 | 1.8 | -2 | -1.2 | 6.5 | 1.6 (4.9) |

| Exports | 3.6 | 6.9 | 1.2 | 1.2 | -0.2 | 0.3 (3.1) |

| Imports | 3.5 | 2.4 | 1.6 | 1.6 | 1.6 | -0.1 (2.7) |

Source: Bank of Korea. The numbers in parentheses represent the growth rate compared to the same period in the previous year.

Another challenge stems from external shocks—particularly with the election of Donald Trump in the US. Trump’s tariff wars could significantly undermine an increasingly export-oriented economy. As a share of GDP, exports grew steadily after the 2000s, driven in part by a growing Chinese market for capital and intermediate goods.

Korea’s export-oriented growth model has suffered setbacks since mid-2022, when a protectionist global turn combined with China’s economic downturn and the development of its domestic industries to replace imports from Korea weakened demand for Korean products. While export growth recovered in late 2023, it has again stalled in recent months. Most notably, Trump’s election and his implementation of tariff hikes, including reciprocal tariffs, pose a significant shock to the Korean economy. Additionally, the announcement to reduce government subsidies for foreign companies under the Inflation Reduction Act (IRA) could negatively impact key Korean companies in the battery industry.

As a result, Korea’s growth prospects for 2025 appear dim. The BOK projected a growth rate of 1.9 percent for 2025 in November 2024, and lowered it to 1.5 percent in February 2025. International investment banks have presented even gloomier outlooks for 2025, with Goldman Sachs predicting a growth rate of 1.5 percent in March 2025. The BOK recently stated that the first-quarter growth rate might be negative, and the annual growth rate could fall below 1.5 percent. In April, the International Monetary Fund (IMF) lowered its 2025 growth rate forecast to 1 percent, down from 2 percent in January.

These bleak economic prospects are compounded by structural trends, not least of which is the demographic shift. According to the Korean government, the share of the elderly aged 65 and older stood at 17.4 percent in 2022, and this figure is projected to rise to 25.3 percent in 2030, 34.3 percent in 2040, and 40.1 percent in 2050, making Korea one of the fastest-aging countries in the world. Furthermore, Korea’s birth rate is the lowest in the world, recorded at just 0.72 in 2023. This trend is attributed to economic insecurity among young people, difficulties in raising children, high real estate prices, and other factors. The relatively high level of inequality, stemming from the dual labor market, combined with limited government redistribution, further exacerbates the low birth rate. As a result, Korea’s working-age population will decline sharply, leading to slower economic growth in the future. Without significant improvements in productivity, the country’s potential GDP growth rate is expected to fall below 1 percent by the 2040s.

A way forward

The Yoon administration has done little to effectively address these challenges. Relying on the outdated approach of trickle-down economics, it has implemented tax cuts for businesses and the wealthy, arguing that economic growth should be driven by the private sector.

Alongside these tax cuts, the Yoon government has pursued fiscal austerity. Reducing the government debt ratio appears like an odd objective for a country whose public debt stands at about 53 percent of GDP in 2024—significantly lower than that of many other advanced economies. The administration limited government spending increases to 2.8 percent in 2024 and 3.2 percent in 2025, lower than the nominal growth rate. However, the administration’s tax cuts have led to a shortfall in tax revenue compared with that in the original budget, with a gap of 56 trillion won (about 2.5 percent of GDP) in 2023 and a shortfall of about 31 trillion won in 2024, ultimately increasing its fiscal deficit. The fiscal deficit recorded 1.5 percent and 1.7 percent of GDP in 2023 and 2024 respectively, running against the government’s goals. Even as Keynesian demand stimulus is back on the table in much of the West, Korean governing elites remain attached to an outdated Anglo-Saxon model. Commitment to the model dates back to the 1997 financial crisis and the subsequent neoliberal restructuring of the South Korean economy.

If Korea is to avoid the worst consequences of this failing economic strategy, it must undertake robust fiscal stimulus and public investment, not only to improve social welfare but also to promote emerging green industries. While there is rising support for a supplementary budget, the leading presidential candidate from the liberal opposition party has both advocated for tax cuts and voiced support for efforts to boost a corporate-led vision of economic growth, making his policy orientation somewhat unclear. What is certain is that Koreans have an opportunity to dramatically alter the course of the Korean economy in favor of sustainable and inclusive growth, based on higher taxation and more active government investment in industrial policy. They should not let this opportunity go to waste.

This article is an updated version of the author’s previously published article.

Further Reading

Kishida’s New Capitalism

Wage stagnation and the echoes of Abenomics

In September 2021, Japanese Prime Minister Kishida Fumio was elected on an ambitious platform: “New Form of Capitalism.” As leader of the Liberal Democratic Party,...

Technocracy and Crisis

Stagnation and technocratic rule in Italy

On September 25, Italians will be called to elect a new Parliament. The snap election follows on the heels of the forced resignation of the...

The Falling Lira

Turkey’s state of permanent crisis

Since late 2021, the Turkish economy has been shattering conventional economic expectations. With deeply negative real interest rates, high inflation, a large and persistent current...