June 29, 2022

Analysis

Geographies in Transition

Mining-based development and the EU's critical raw materials strategy

Though it failed to resolve a number of contentious issues, the COP26 meeting in Glasgow solidified a consensus around the need for a global transition to clean energy. Implicated in this transition is the wide-scale adoption of renewables: we must build larger wind turbines, produce more electric vehicles, and phase down coal factories in electrifying rapidly growing cities. Climate negotiations often refer to the “common but differentiated responsibility” that countries bear in promoting this transformation. But in reality, its protagonists are European governments and high-tech manufacturing companies involved in the production of renewable goods. And their policies have a cost—if the world meets the targets of the Paris Agreement, demand is likely to increase by 40 percent for copper and rare earth elements (REES), 60–70 percent for cobalt and nickel, and almost 90 percent for lithium over the next two decades.

The EU’s proposed Green Energy Deal secures critical minerals through open international markets, necessitating mineral extraction at a faster and more intense pace. But if it is to mitigate or overturn historical imbalances between North and South, the clean-energy transition cannot reproduce the same extractive relations underpinning industrial production. In what follows, I examine the green transition both as an opportunity and a challenge for resource-rich countries in the Global South. Importantly, I argue that we need to look beyond traditional growth-oriented industrial policies and the successful “catch up” of East Asian economies to develop inclusive and sustainable green development.

New geographies of extraction

The clean-energy transition is a historically significant moment for resource producers. It involves the intensive and extensive extraction of “rare metals”—metal minerals produced in low quantities and utilized as intermediate inputs in the manufacturing of digital, renewable, and energy technologies. These have also been identified by the US and EU as “critical raw materials” (CRMs), which are both strategically important for industrial competitiveness and at high risk due to possible supply gluts and changes in world markets. The US lists thirty-five critical minerals in order of their importance for national security and wider supply-chain vulnerabilities. EU Commission reports identify thirty critical raw materials, found in Table 1. In this ordering, critical minerals are grouped into three major categories: heavy rare earths (HREEs), light rare earths (LREEs), and platinum group metals (PGMS). The list also includes various ferrous and non-ferrous metals.

Table 1: Current Global Share of Production and Processing of Critical Minerals

Material | Stage | Main global supplier | Share |

| Antimony | E | China | 74% |

| Baryte | E | China | 38% |

| Bauxite | E | Australia | 28% |

| Beryllium | E | USA | 88% |

| Bismuth | P | China | 80% |

| Borate | E | Turkey | 42% |

| Cerium | E | China | 86% |

| Cobalt | E | Congo,DR | 59% |

| Coking coal | E | China | 55% |

| Dysprosium | E | China | 86% |

| Erbium | E | China | 86% |

| Europium | E | China | 86% |

| Fluorspar | E | China | 65% |

| Gadolinium | E | China | 86% |

| Gallium | P | China | 80% |

| Germanium | P | China | 80% |

| Hafnium | P | France | 49% |

| Ho,Tm,Lu,Yb | E | China | 86% |

| Indium | P | China | 48% |

| Iridium | P | S. Africa | 92% |

| Lanthanum | E | China | 86% |

| Lithium | P | Chile | 44% |

| Magnesium | P | China | 89% |

| Natural graphite | E | China | 69% |

| Natural rubber | E | Thailand | 33% |

| Neodymium | E | China | 86% |

| Niobium | P | Brazil | 92% |

| Palladium | P | Russia | 40% |

| Phosphate rock | E | China | 48% |

| Phosphorus | P | China | 74% |

| Platinum | P | S. Africa | 71% |

| Praseodymium | E | China | 86% |

| Rhodium | P | S. Africa | 80% |

| Ruthenium | P | S. Africa | 93% |

| Samarium | E | China | 86% |

| Scandium | P | China | 66% |

| Silicon metal | P | China | 66% |

| Tantalum | E | Congo, DR | 33% |

| Terbium | E | China | 86% |

| Titanium | P | China | 45% |

| Tungsten | P | China | 69% |

| Vanadium | E | China | 39% |

| Yttrium | E | China | 86% |

| Strontium | E | Spain | 31% |

| Legend | |

| Stage | E = Extraction stage, P = Processing stage |

| HREEs | Dysprosium, erbium, europium, gadolinium, holmium, lutetium, terbium, thulium, ytterbium, yttrium |

| LREEs | Cerium, lanthanum, neodymium, praseodymium and samarium |

| PGMs | Iridium, palladium, platinum, rhodium, ruthenium |

Among the minerals listed above, the most significant are rare earth elements (REEs). Table 2 summarizes these seventeen chemically similar metals and their applications across various industries. These metals share a strategic importance due to their numerous industrial applications, mostly as intermediate outputs like alloys and components which are then assembled into higher value-added industrial goods such as electric motors and drones. Rare metals are essential inputs for clean technologies, notably in the mass production of wind turbines, photovoltaic panels, as well as hybrid and electric vehicles.1Patrícia Alves Dias, Silvia Bobba, Samuel Carrara, and Beatrice Plazzotta. 2020. “The Role of Rare Earth Elements in Wind Energy and Electric Mobility.” EUR 30488. Luxembourg: Publication Office of the European Union; Nakano, Jane. 2021. ‘The Geopolitics of Critical Minerals Supply Chain’. Washington, D.C.: Center for Strategic and International Studies.

Table 2: Rare Earths Elements and their Industrial Applications

| Name | Symbol | Atomic No. | Applications and products |

| Scandium | Sc | 21 | Aerospace materials, consumer electronics, lasers, magnets, lighting, sporting goods |

| Yttrium | Y | 39 | Ceramics, communications systems, lighting, frequency meters, fuels additive, jet engine turbines, televisions, microwave communications, satellites, vehicle oygen sensors |

| Lanthanum | La | 57 | Catalyst in petroleum refining, television, energy storage, fuel cells, night vision instruments, rechargeable batteries |

| Cerium | Ce | 58 | Catalytic converters, catalyst in petroleum refining, glass, diesel fuel additive, polishing agent, pollution control systems |

| Praseodymium | Pr | 59 | Aircraft engine alloy, airport signal lenses, catalyst, ceramics, coloring pigment, electric vehicles, fiber optic cables, lighter flint, magnets, wind turbines, photographic filters, welder’s glasses |

| Neodymium | Nd | 60 | Anti-lock brakes, air bags, anti-glare glass, cellphones, computers, electric vehicles, lasers, MRI machines, magnets, wind turbines |

| Promethium | Pm | 61 | Beta source for thickness gages, lasers for submarines, nuclear powered battery |

| Samarium | Sm | 62 | Aircraft electrical systems, electronic counter measure equipment, electric vehicles, flight control surfaces, missile and radar systems, optical glass, permanent magnets, precision guided munitions, stealth technology, wind turbine |

| Europium | Eu | 63 | CFL, lasers, televisions, tag complex for the medical field |

| Gadolinium | Gd | 64 | Computer data technology, magneto-optic recording technology, microwave applications, MRI machines, power plant radiation leaks detector |

| Terbium | Tb | 65 | CFL, electric vehicles, fuel cells, televisions, optic data recording, permanent magnets, wind turbines |

| Dysprosium | Dy | 66 | Electric vehicles, home electronics, lasers, permanent magnets, wind turbines |

| Holmium | Ho | 67 | Microwave equipment, color glass |

| Erbium | Er | 68 | Color glass, fiber optic data transmission, lasers |

| Thulium | Tm | 69 | X-ray phosphors |

| Ytterbium | Yb | 70 | Improving stainless steel properties, stress gages |

| Lutetium | Lu | 71 | Catalysts, positron emission tornography (PET) detectors |

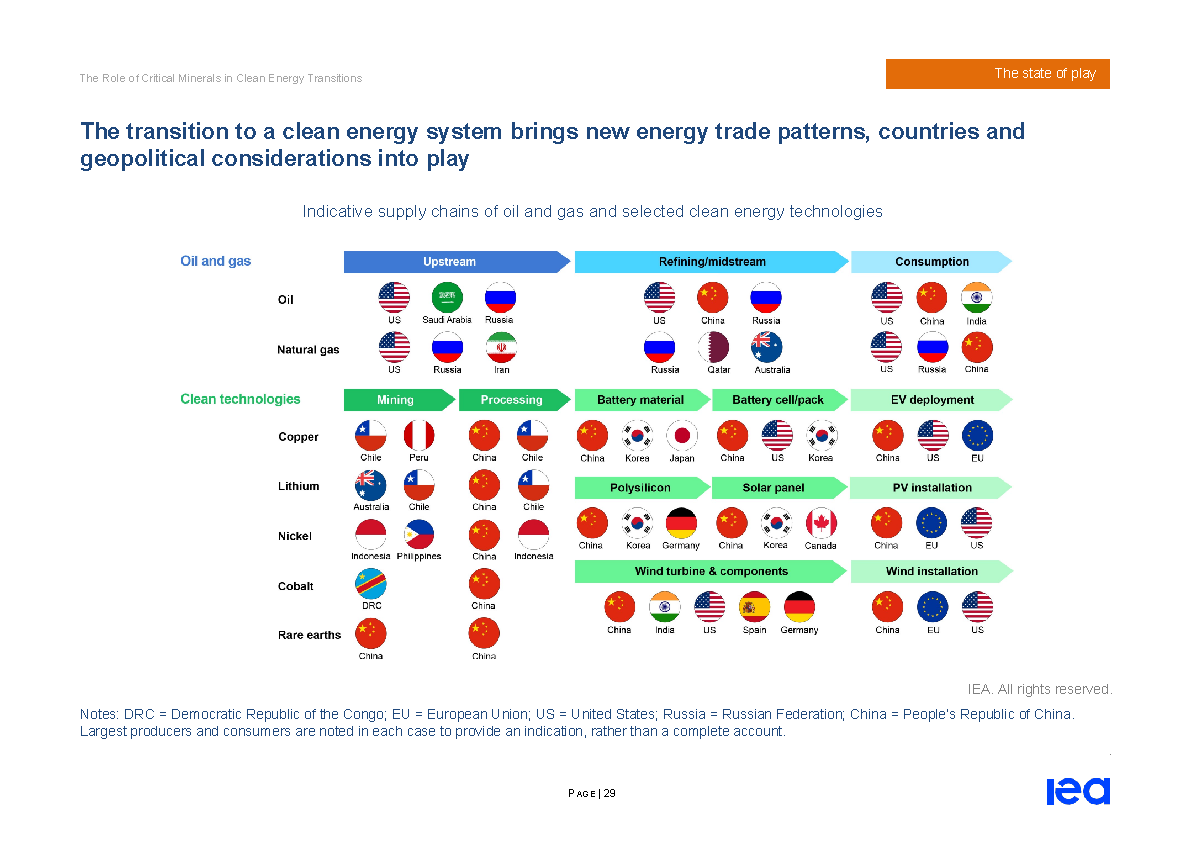

Although mining has long been a staple input for industrialization, mineral extraction for renewables generates new patterns of trade in the energy sector. For example, resource-poor but industrialized East Asian countries like Japan, Korea, and Taiwan compete directly with European and American capital when it comes to renewables. Their car manufacturing, digital and ICT, and intermediate sectors like permanent magnets and semi-conductors all rely on access to raw materials from China and the rest of the developing world. By contrast, EU and US governments have been principally concerned with the fact that non-democratic regimes like China and Russia hold such significant market power in controlling CRM reserves and production. As the clean-energy transition accelerates, East Asia, the EU, and the US are all repositioning themselves in a rapidly changing global-value chain, deploying various diplomatic, trade, and industrial strategies to maintain, if not strengthen, their competitive advantage in a new global economy marked by competition for raw materials, technological innovation, and new manufacturing capabilities.

The logic of Europe’s CRM strategy

The EU views the challenge of accessing critical minerals through a market lens: resource-producing countries simply need to sell their commodities at a higher price on world markets in order to resolve the supply constraint. While this means that the bloc might pay higher prices during commodity swings, critical minerals will remain available in the global market. Such a perspective assumes that market players will separate their economic and political interests. This, indeed, is what has happened since the 1980s, when European governments managed to secure gas from Russia and oil from the Middle East.

But as Figure 1 shows, the current energy transition involves more veto players—key among them China. As a result, the EU is forced to reassess its relationship with Africa and Latin America, where substantial reserves of base metals, lithium, cobalt, and platinum are located. Nickel—a major metal needed for the construction of bigger wind turbines, EV cars, and solar panels—is concentrated in the Philippines and Indonesia. Consequently, some strategic repositioning is required for the EU to secure future minerals for green technology.

Of all the strategic considerations, a growing dependence on China remains the most important. As Table 1 and Figure 1 illustrate, China not only holds the most extensive rare earth reserves, it also exercises control over REE production and processing. China’s share of global production of other key metals—Graphite, Magnesium, Tungsten, Vanadium—further reveals the EU’s dependence. Moreover, recent waves of resource nationalization have suggested that emerging markets are willing and able to bargain for better terms of trade and investment.

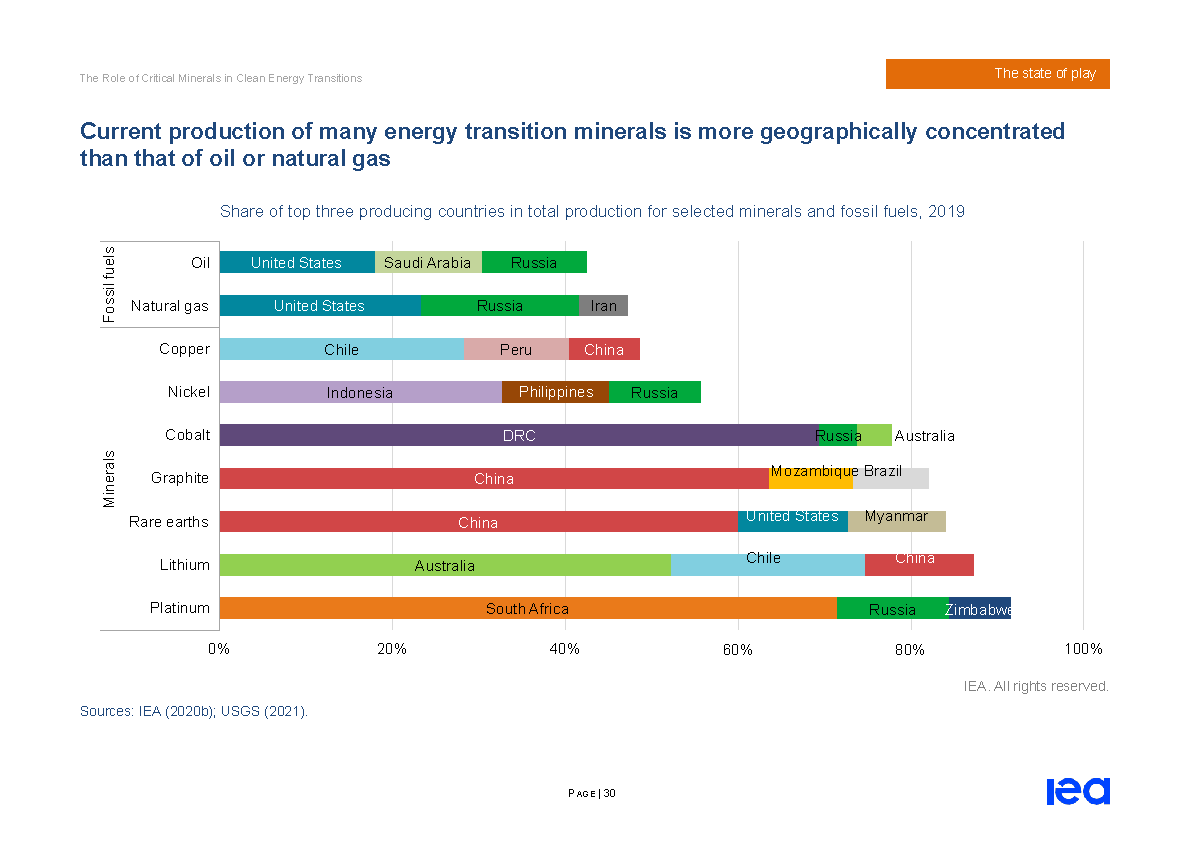

The EU’s CRM scarcity is an indicator of its potential vulnerability. This is compounded by the concentration of energy-transition minerals. For cobalt, lithium, and REEs, the top three producing countries control about three-quarters of current global outputs. The costs of extracting transition minerals have also increased in response to environmental pressures. For example, Chilean copper ore quality has declined by 30 percent over the past fifteen years. These trends place significant pressures on the EU’s response. Its Strategic Foresight Report recognizes the need to address the redistribution of global power as the geo-economic center of gravity moves definitively eastwards. Consequently, the EU is charting its path to coping with increased competition for resources and rivalry for influence from emerging economies.

Perhaps unsurprisingly, EU strategy thus appears to be a defense of the current world order. In the past, European powers defended international trade under the guise of comparative advantage. Agricultural and mineral production in developing countries were taken for granted; African and Latin American states were expected to sustain mineral production for the world economy while industrialized countries would sell their manufactured goods. The recently concluded EIT Raw Materials Conference in Brussels in November 2021 reflects a similar free-trade logic. The Commission clearly articulated their intention to promote multilateralism, open access to world markets, and economic globalization. The panel on EU-Africa relations, for instance, emphasized the need to promote “European values” as a public good that African leaders might choose over China’s debt diplomacy. The report cogently captures this:

Openness, as well as rules-based international and multilateral cooperation, are strategic choices…The history of the European project demonstrates the benefits of well-managed interdependence and open strategic autonomy based on shared values, cohesion, strong multilateral governance and rules-based cooperation [emphasis added].

But the benefits of the open-market strategy for the Global South are dubious at best. As dependency theorists have argued since the 1960s, trade with global hegemons has often denied policy space for countries in the Global South to transcend their role as primary-commodity producers. Accordingly, commodity exporters are likely to lose against manufacturing based economies due to the price difference of their products in international trade.

As one of my interviewees suggests, the EU’s lack of knowledge regarding the minerals in its own borders is a direct reflection of its colonial past. Reluctant to embrace mineral production in their own territories, European governments have leveraged the language of comparative advantage to place the responsibility of mineral production on the shoulders of poor, resource-rich countries. The EU’s current framework similarly seeks to justify extractive relationships with world markets through a liberal language. In the 2021 State of the Union Speech, President Ursula von der Leyen presented the bloc’s EU-Indo-Pacific strategy as a preventative measure against the influence of autocratic regimes. The EU Global Gateway—its answer to China’s Belt and Road Initiative (BRI)—emphasized the importance of European values:

We want investments in quality infrastructure, connecting goods, people and services around the world. We will take a values-based approach, offering transparency and good governance to our partners…We want to create links and not dependencies! [emphasis added].”

To seriously engage with the historical legacy of colonialism, the EU’s future cooperation and infrastructure strategy must recognize Europe’s historical responsibility for the lack of industrialization in the developing world. This would legitimate demands for more value added from resource-rich states. Crucially, it might help correct the colonial logic of extraction that is deep-seated and widely embedded in European institutions and public debates. If anything, the current shift eastwards could tame the intrinsically Eurocentric perspective dominant in mainstream social sciences.

Critical minerals: Curse or blessing?

Resource producers in Africa, Latin America, and Southeast Asia are well-positioned to take advantage of soaring demand for CRMs. For instance, Mongolia, the Philippines, and Indonesia hold significant nickel and copper reserves which can complement the contribution of Latin American producers like Bolivia, Peru, and Chile. The danger lies in the political and economic dynamics of resource dependence. Scholars of the “resource curse” have argued that increased reliance on natural resources for exports and revenues yields slower economic growth, higher propensity for corruption and rent-seeking, and increased likelihood of political violence. 2Beblawi, Hazem, and Giacomo Luciani, eds. 2016. (<)em(>)The Rentier State(<)/em(>). London and New York: Routledge.; Collier, Paul, and Anke Hoeffler. 2004. ‘Greed and Grievance in Civil War’. (<)em(>)Oxford Economic Papers(<)/em(>), no. 56: 563–95. Though its theoretical and methodological assumptions have come under scrutiny,3Di John, Jonathan. 2011. ‘Is There Really a Resource Curse? A Critical Survey of Theory and Evidence’. (<)em(>)Global Governance(<)/em(>) 17 (2): 167–84.; Di John, Jonathan. 2014. ‘The Political Economy of Industrial Policy in Venezuela’. In (<)em(>)Venezuela Before Châvez: Anatomy of an Economic Collapse(<)/em(>), edited by Ricardo Hausmann and Francisco Rodríguez, 321–70. University Park: Pennsylvania State University Press. the resource curse continues to persuade donor agencies who associate corruption, economic mismanagement and predatory behavior with resource-rich national governments.

Unable to develop indigenous technology, build inter-sectoral linkages, or mitigate the social conflicts arising from unchecked resource exploitation, resource-rich countries also suffer from commodity specialization. Some have attributed this development malaise to the detrimental effects of external linkages with advanced industrialized countries: as long as resource producers remain commodity exporters, there are very few incentives to promote export diversification and to craft ambitious industrial plans that would break the cycle of extractivist growth. 4Burchardt, Hans-Jürgen, and Kristina Dietz. 2014. ‘(Neo-)Extractivism – A New Challenge for Development Theory from Latin America’. (<)em(>)Third World Quarterly(<)/em(>) 35 (3): 468–86.; Veltmeyer, Henry. 2013. ‘The Political Economy of Natural Resource Extraction: A New Model or Extractive Imperialism?’ (<)em(>)Canadian Journal of Development Studies / Revue Canadienne d’études Du Développement(<)/em(>) 34 (1): 79–95. The historical legacy of extractive-led growth heavily weighs upon the politics, institutions, and interests of these countries. 5Thorpe, Rosemary, Stefania Battistelli, Yvan Guichaoua, José Carlos Orihuela, and Maritza Paredes. 2012. (<)em(>)The Developmental Challenges of Mining and Oil: Lessons from Africa and Latin America(<)/em(>). Basingstoke: Palgrave Macmillan.

Nevertheless, there are important advantages to mining-based development. First, demands for base metals like nickel, copper, and iron are expected to steadily increase, granting governments time to protect their economies from cyclical boom and busts, design financial infrastructures which maximize mineral rents, and direct investment towards communities at the frontiers of extraction who face its grave socio-ecological consequences. Despite the preponderance of weak states in the Global South, there are notable examples of institutional innovation. For example, Peru has implemented comprehensive mining reforms which better distribute revenue between central and regional governments, alleviating the distributional pressures and socio-environmental consequences of localized resource curse.6Gustafsson, Maria-Therese, and Martin Scurrah. 2019. ‘Strengthening Subnational Institutions for Sustainable Development in Resource-Rich States: Decentralized Land-Use Planning in Peru’. (<)em(>)World Development(<)/em(>) 119 (July): 133–44.; Orihuela, José Carlos. 2018. ‘Institutions and Place: Bringing Context Back into the Study of the Resource Curse’. (<)em(>)Journal of Institutional Economics(<)/em(>) 14 (1): 157–80. Brazil, with its long history of institution-building, was able to promote renewable energy, impose flexible local content requirements to support domestic industrialists, and establish strict environmental licensing procedures in the oil and gas sectors.7Hochstetler, Kathryn, and Genia Kostka. 2015. ‘Wind and Solar Power in Brazil and China: Interests, State–Business Relations, and Policy Outcomes’. (<)em(>)Global Environmental Politics(<)/em(>) 15 (3): 74–94.; Massi, Eliza, and Jewellord Nem Singh. 2018. ‘Industrial Policy and State-Making: Brazil’s Attempt at Oil-Based Industrial Development’. (<)em(>)Third World Quarterly(<)/em(>) 39 (6): 1133–50.

Second, there is evidence for the success of the so-called ‘resource-based industrialization’ strategy. Brazil’s Petrobras, Norway’s Statoil, and Venezuela’s PDVSA prior to Chavez demonstrated how state enterprises can be utilized to achieve the ‘big push’, natural resources-intensive industrialization. Their emphasis was on developing indigenous technology to create a niche market and to obtain access to downstream networks of consumers, thereby, creating vertically integrated firms capable of competing against international oil companies.

Mineral states can pursue resource-based industrialization by promoting industrial policies aimed at processing critical minerals within their domestic markets. Indonesia’s ban on exporting raw nickel and its forcing of international companies to refine and process mineral ores inside the country is one example. Another method has been the strategic deployment of state-owned enterprises (SOEs) in managing natural resource assets—a policy often adopted by countries with limited production capacity. In the best possible conditions, states might also encourage domestic companies to directly compete with international mining companies in the exploration and production stages, as in the example of Brazil’s national oil company Petrobras and regional SOE Codemge. However, this approach requires sophisticated industrial strategies that only countries with sufficient planning and coordination capabilities can implement. Irrespective of the policy choice, the fundamental logic remains: mining is a high-risk industry, requiring enormous capital investments and regularly subject to market failures. States, taking a developmental longer-term horizon, must accept these risks to promote sectoral development.

Further Reading

The Whole Field

Markets, planning, and coordinating the green transformation

In recent years, an intense debate has unfolded over the policy and politics of the green transition. Politically, the tide appears to be receding: As...

Uneven Channels

Climate diplomacy and the global financial architecture

This year’s Conference of the Parties (COP), opening October 31, is hosted by the United Kingdom, whose agenda-setting privilege as host has made private finance...

Inside Out

Shaping the base of a renewable economy

The transition to a post-carbon energy economy will require extraction.