October 2, 2025

Analysis

India in the New Global Order

Between hydrocarbon coalitions and the green electro-state

At the Polycrisis, we’ve taken a special interest in the question of how India has been positioning itself in the new world order that has been emerging since 2022. Our inaugural essay featured India’s nonalignment in the Ukraine war as a bargaining chip for trade, investment, security, and technology deals from both the West and the Russia-China bloc. We interviewed Navroz Dubash on the developmentalist turn in global climate politics that owes much to Indian intellectuals and the aspirational pressures of 1.4 billion people. We talked with Ravinder Kaur on Hindu nationalist designs and globalist visions. We wrote about Modi’s bid for technology transfers in the Biden era, at a time when the Western alliance was positioning India as a bulwark against China. Jairus Banaji analyzed the evolution of Indian big business for Phenomenal World.

For this edition of the Polycrisis, we asked Shreyas Shende, who runs the fantastic Indialog newsletter, and who works with Tim at Johns Hopkins, to analyse the momentous breakdown in India-US relations. In what follows, he asks whether or not India will accept Trump’s offer of being locked into a US-led carbon coalition or break free with its own green developmentalist growth model. — Kate Mackenzie and Tim Sahay

When President Trump announced an additional 25 percent tariff on imports from India in August—ratcheting up the total to 50 percent, among the highest in the world—he threw the bilateral relationship into peril. Writing in Foreign Affairs last month, Jake Sullivan and Kurt Campbell warned of the “unprecedented discord” threatening the future of the relationship; Evan Feigenbaum at the Carnegie Endowment highlighted the risk of “dismantling” a relationship “painstakingly built” over twenty-five years, and experts in New Delhi noted that “long-term damage of Trump’s policies” should not be underestimated. According to Trump, the new tariffs are punishment for India’s purchase of Russian oil, plus the longer standing protectionist nature of India’s market. To many analysts, there are also more personal reasons for the fallout between the two strongmen. What are the likely consequences of this significant diplomatic dustup?

A day after Trump’s tariffs announcement, India’s National Security Advisor Ajit Doval was at the Kremlin meeting with Putin and highlighting the “strategic and special partnership” shared by the two nations. Moscow was not the only recipient of New Delhi’s attention, which is seeking to consolidate ties with other economies and to demonstrate its autonomy on the world stage. In recent weeks, Chinese Foreign Minister Wang Yi made a visit to India, as did Singapore’s Prime Minister Wong and Germany’s Foreign Minister Wadephul. Leader-level calls were held with Brazil’s President Lula, French President Macron, and Finnish President Alexander Stubb, while Modi flew to Japan and China.

When it comes to diplomacy, New Delhi likes to have what foreign minister Subrahmanyam Jaishankar calls “multiple choices.” But a 50 percent tariff rate from the US means that New Delhi is left with one less choice. This has consequences, in turn, for the way India will be able to manage its energy ties with other powers, key among them China, Russia, and the EU.

Engagements with Russia and China

Though recently circulating images of Modi-Putin-Xi bonhomie suggest strong ties, the relationship between India and Russia has been in decline for some time. It’s in that context, and from a position of weakness, that India is now re-engaging with China.

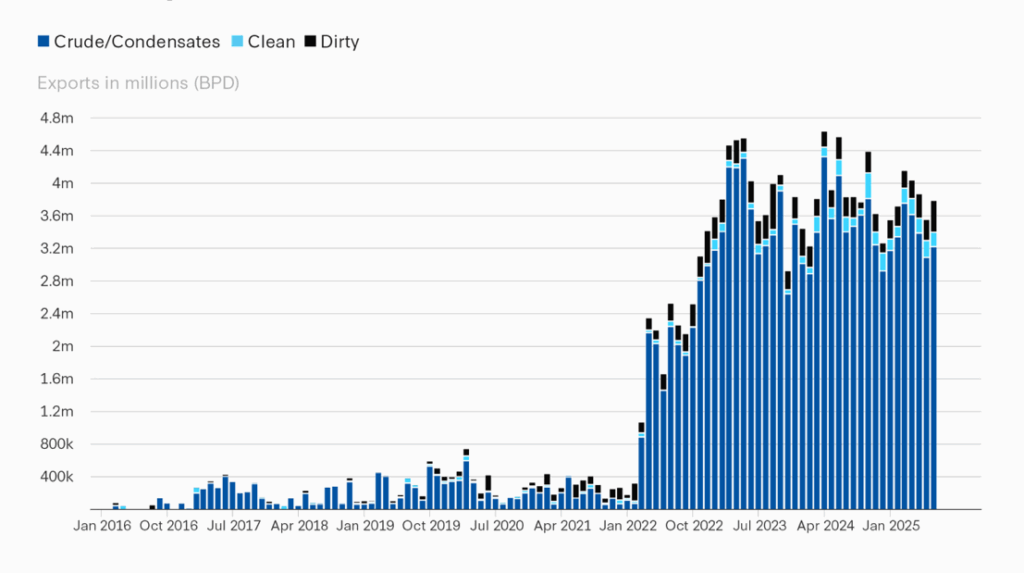

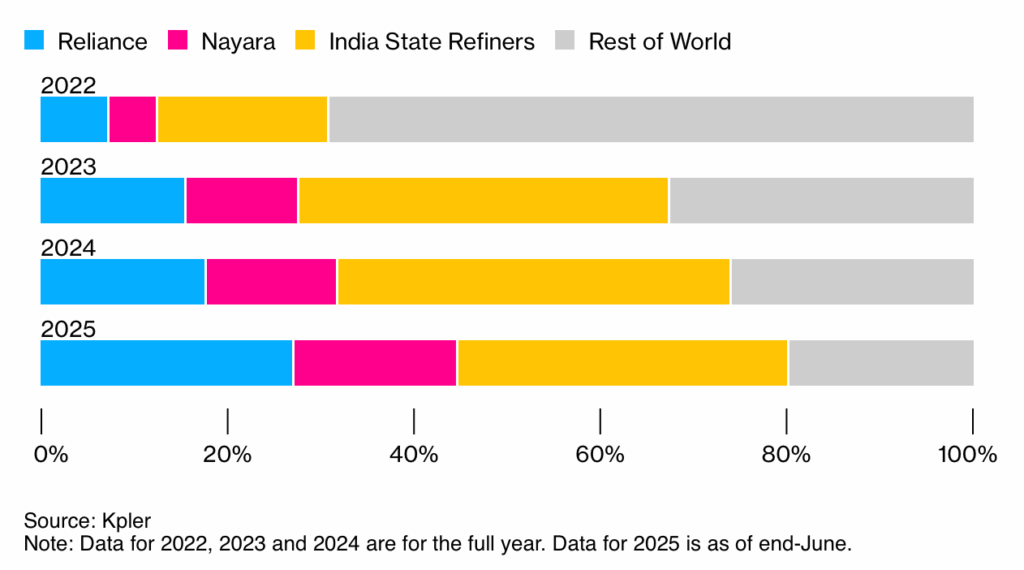

For two consecutive years, in 2022 and 2023, India and Russia failed to hold their joint annual summit. Russia’s invasion of Ukraine in February 2022 meant steep hikes in food and fuel prices in India, and a time when it was still dealing with the economic fallout from Covid. It was at this time that India’s imports of Russian oil began to surge. In 2021, Russia accounted for just 2 percent of India’s oil imports; by May, it supplied 40 percent of India’s oil.

India bought Russian oil at a discount, below the $60 a barrel price cap, and domestic firms (including the Russian-backed Nayara Energy) refined it both for domestic consumption and for external markets. Under Biden, these high imports of Russian oil were criticized but they were also seen as a stabilizing factor; the US “wanted somebody to be buying Russian oil,” as the then Ambassador to India put it. Under Trump, all this has changed but as the world’s third largest energy consumer and second-largest net importer of crude oil, access to cheap fuel remains key to India’s energy security.

As Indo-US relations have floundered, New Delhi has sought to strengthen its ties with China, which remains a key source of critical industrial materials. In 2020, simmering tensions between the neighboring countries erupted when soldiers violently clashed at the contested Galwan border but in more recent months, things have begun to improve. Last month, Modi made his first visit in seven years to Tianjin for the annual Shanghai Cooperation Council Summit. There, he stated that the China-led grouping could “play a guiding role in promoting multilateralism and an inclusive world order.” This belies the stark difference between India and China’s view of the global order and their respective ambitions therein. On top of this, the disputed border remains unresolved; each side views the other’s activities in the subcontinent and the Indian Ocean with suspicion, and India remains wary of China’s support for Pakistan (exemplified in May during the latest India–Pakistan clashes).

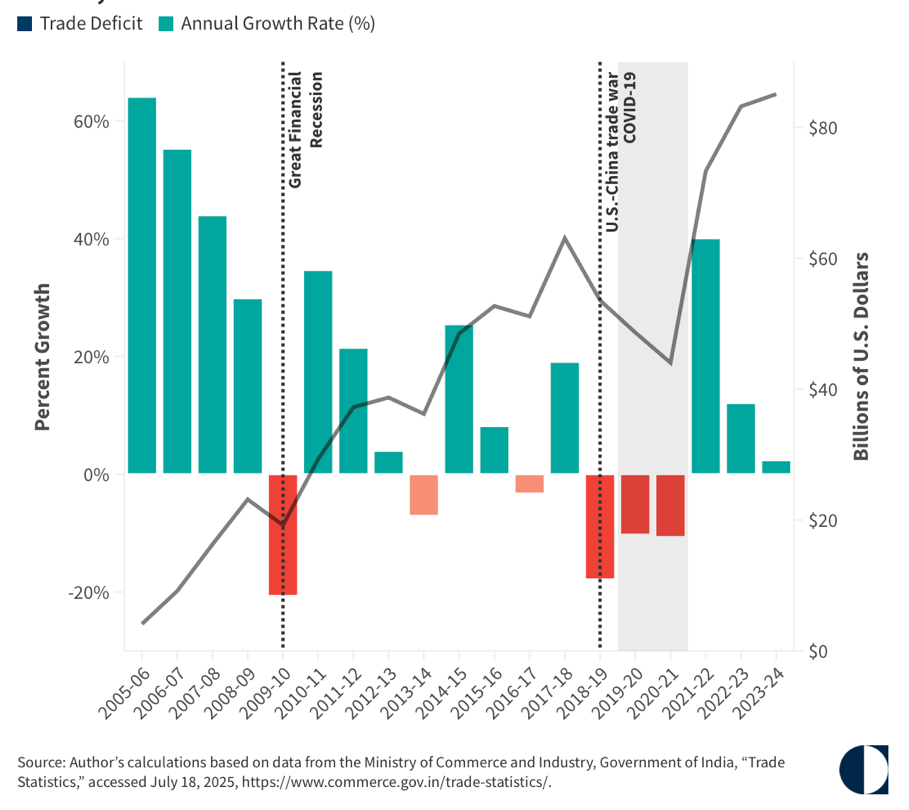

What of the two countries’ economic relationship? China remains India’s largest goods trading partner and total trade between the two is increasing; it shot up from $86.4 billion in 2020–21 to $127.71 billion in 2024–25. The relationship is asymmetrical however, with India’s exports to China decreasing as imports from China rise. This has given rise to a staggering trade deficit of $99.21 billion in 2024–25.

There are sections of India’s elite advocating for greater economic ties between the two powers. As one Indian government official noted last year, “China is the world’s factory” and so it “cannot be dispensed with.” This was followed by the Ministry of Finance’s annual Economic Survey, which argued that, “to boost Indian manufacturing and plug India into the global supply chain, it is inevitable that India plugs itself into China’s supply chain.”

Since then, business groups have successfully pushed for streamlined visa policies for Chinese engineers and technicians, and senior government officials have advocated for Sino-Indian joint ventures. This has borne some fruit, including prominent partnerships between battery manufacturers. Indian firms recognize that across a number of clean tech sectors, China is dominant and India needs access to advanced Chinese tech and know-how. The 2023–24 Economic Survey also pointed out that “well-chosen imports with investments from China raises the prospect of creating domestic know-how down the road.”

China, for its part, is dealing with economic headwinds and reining in what it calls “involution”—or excessive competition leading to deflation—in clean tech sectors such as EVs and solar. Crucially, as Gerard DiPippo has argued, even though the Chinese economy has grown to a point where it is “too big to rely on exports for a large share of its growth,” it still depends on external markets. In this context, neighboring India is especially attractive.

The strategy has its limitations, however. Indian officials understand that they are dealing with China from a position of weakness; as the Economic Survey puts it, it has to choose between “second and third-best choices.” and there is a risk of economic coercion. To list a few examples, since October 2024 when the normalization of bilateral ties was first announced, China has at various points blocked the exports of tunnel boring machines, specialty fertilizers, and specialized manufacturing equipment. It has pulled Chinese workers and technicians from India to stall Apple Inc’s manufacturing push in India, and reportedly encouraged “regulatory agencies and local governments to curb technology transfers and equipment exports to India.”

India’s industrial policies and the clean energy boom

India’s relationship with China, as with Russia and the United States, needs to be examined in the context of its energy security needs, its decarbonization goals, and its initiatives to build out clean energy capabilities. The Indian government has set the target of meeting “50 percent of its installed electrical capacity from non-fossil sources” by 2030—a goal it achieved five years ahead of schedule. Beyond this, it wants to become “self-reliant” in the energy sector by 2047, and reach net-zero emissions by 2070.

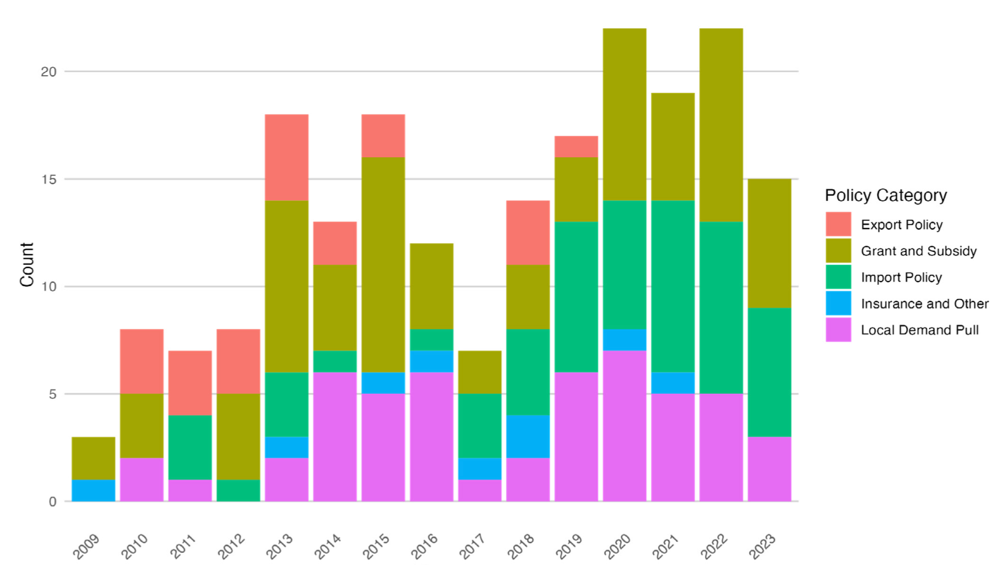

There are several key components of India’s clean-energy ambitions. They include the National Steel Policy (2017), the National Policy on Biofuels (2018, revised in 2022), the National Mission on Transformative Mobility and Battery Storage (2019), the Production Linked Incentives (PLI) scheme (2020), and the National Green Hydrogen Mission (2023). The PLI scheme has focused on the twin goals of boosting India’s manufacturing capabilities and reducing import dependence on China. It targets a range of industries, including specialty steel, high-efficiency solar PV modules, and advanced chemistry cell (ACC) batteries.

While there has been notable success in the large-scale electronics manufacturing sector, PLI has struggled to make gains in the clean-energy sector. This is partly thanks to the way that the policy was designed to favor larger firms, and some targeted sectors such as textiles actually saw their exports decrease. Scholars have questioned the painfully slow rate of subsidy disbursal, the scheme’s complex regulatory regime, the spread of incentives across a disparate range of arguably non-strategic sectors, and the lack of focus on more fundamental market and land reforms, with government officials (anonymously) noting that “excessive red tape and bureaucratic caution” stall the scheme’s effectiveness.

Perhaps the most searing indictment of the PLI scheme, and broader attempts at boosting manufacturing over the past decade, can be found in the data on the value add of manufacturing as a percentage of GDP. Through the PLI scheme, the government hoped to raise the share of manufacturing to 25 percent by 2025. But in 2024, the value add of manufacturing dipped to 13 percent—the lowest figure since 1967. With the percentage of value added in PLI-targeted sectors still in single digits, the government is planning to let the scheme lapse for all sectors except electronics manufacturing.

Insofar as it aimed to reduce dependency on China, the PLI can be counted unsuccessful. Reuters reported that eight of the twelve firms selected for the scheme, including units of Reliance and Adani Group, were unlikely to meet their targets according to sectoral analysis conducted by the Ministry of New and Renewable Energy (MNRE). However, PLI scheme misfires don’t accurately represent the progress in India’s renewable energy sector as policymakers have deployed a broader industrial policy toolkit.

India’s installed renewable energy capacity grew roughly three-fold from 76.37 GW in March 2014 to 226.79 GW in June 2025, with renewable energy generation’s share in overall power generation increasing from 17.2 percent to around 22.2 percent in the same period. The growth in solar in particular has been strong with capacity rising from 2.82 GW in 2014 to 110.9 GW in 2025. In the decade from 2014 to 2025, India’s solar PV module capacity rose from 2.3 GW to 88 GW, and solar PV cell capacity from 1.2 GW to 25 GW.

This growth in manufacturing capacity parallels an investment surge in renewables; in 2024, 83 percent of power sector investments were in clean energy. The Indian government has instituted a range of industrial policies to improve its clean-energy manufacturing capacity and lower its reliance on Chinese imports. These include demand pull interventions, tariffs on solar modules and cells from China and parts of Southeast Asia, and the Approved List of Models and Manufacturers (ALMM) that mandates the use of listed solar PV models and module manufacturers for domestic solar projects.

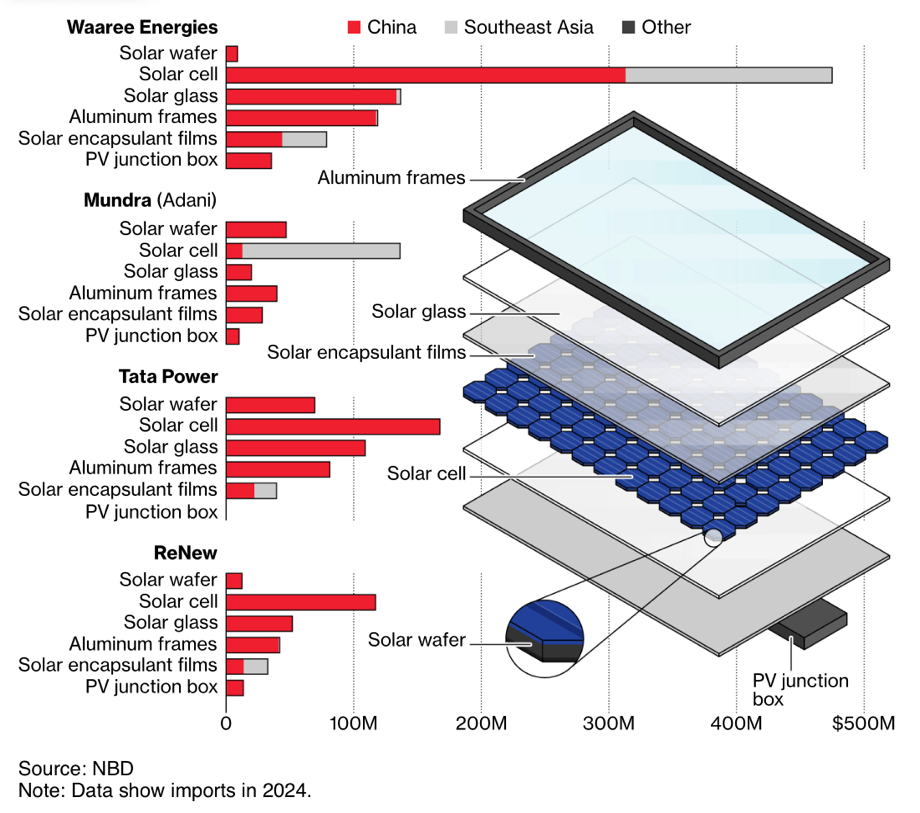

The challenge is that as India’s solar manufacturing capabilities have expanded, it remains dependent on China for key inputs. India’s imports of solar PV cells from China rose 141 percent from about 1.89 billion units in 2023–24 to 4.55 billion in 2024–25. MNRE officials have attributed the rise in imports to the increase in manufacturing capacity for domestic solar PV modules. While India’s solar PV cell capacity rose to 25 GW in 2025, it remains unable to meet the total demand for solar modules.

Domestic manufacturers expect a substantial growth in cell manufacturing capacity in the coming years, with plans to ramp capacity up to 100 GW by 2030. Even as India strengthens its solar manufacturing capacity and shifts its dependence on China further upstream, challenges will remain. For instance, the current wafer manufacturing capacity stands at 2 GW (expected to rise to 40 GW by 2030) and wafer imports are rising to cater to cell production. In addition to this, Indian regulators are investigating an anti-dumping case on Chinese solar cell imports, while China instructs its local firms to “rein in overcapacity and cut-throat pricing.” China also retains a “near-monopoly on cutting-edge wafer manufacturing systems” which are restricted from being exported to India.

India’s expansion of clean energy manufacturing capabilities will help with energy diversification while strengthening its manufacturing base. A key challenge, however, will be China’s chokehold on the sector.

India in the new global (green?) order

More than a third of the countries that have placed sanctions and set price caps on Russia since 2022, including the United States, import a substantial chunk of oil products from the Jamnagar refinery in India. This Reliance-owned refinery is the world’s largest and most complex single-site refinery, with a capacity to process 1.4 million barrels per day. It was built using US equipment and technology financed by a $500 million loan guarantee from the Export-Import Bank of the United States with Bechtel, one of the US’s oldest and largest infrastructure and construction companies, which plays a critical role in the creation and then expansion of the refinery complex.

Many of New Delhi’s policy challenges turn on the issue of energy security. Despite the response from the US, India has no plans of turning away from Russian oil. On the contrary, Indian refiners have been pressuring Russian sellers to reduce prices and state-owned refiners have reportedly “snapped up September- and October-loading cargoes.”

The United States’s diktats about where Indian can and can’t procure its energy from will only have the effect of increasing New Delhi’s drive to diversify its energy sources and strengthen its domestic clean energy manufacturing base. Indian policymakers are acutely aware of the need for energy security, especially in light of the vast gulf in per capita energy consumption between developing and developed nations. An average American, for example, consumes in a month roughly the same amount of energy as an average Indian does in a year.

While India has ramped up energy purchases from the United States in the first half of 2025 and promised to establish the latter as a “leading supplier of crude oil and petroleum products and liquified natural gas” to the former, the fact remains that Washington D.C. wants to stall decarbonization globally. On the other hand, Beijing is “reducing costs and accelerating uptake of clean electro-technologies in other countries” as Ember has outlined.

In the midst of this new geopolitics of the green transition, India’s green industrial strategy is significant. Navigating these new dynamics whilst pursuing clean-energy goals is no simple task. India’s policymakers will seek to stabilize trading relationships, ensure access to cheap energy sources and, more generally, maintain good ties with leading powers. . To shore up its clean energy ambitions, there are a number of steps available to policymakers, as outlined by the Net Zero Industrial Policy Lab. These include focusing on solar, steel, and batteries, embracing the process of industrial strategy where failure is part and parcel, and appropriately investing in its innovation ecosystem.

There are no perfect solutions. Even as New Delhi’s relations with Moscow and Washington realign, policymakers need to be wary of substituting reliance on one hydrocarbon power with another. In the pursuit of its clean-energy ambitions, India will need to work with China, but the past has made it clear that over-reliance on Chinese products comes with a significant cost. Might a new green developmentalist model be possible? What provides India greater freedom of choice and sovereignty? Locking into hydrocarbon coalitions or doubling down on investments for a green electro-state track? How India chooses to address this question will shape the destiny of its 1.4 billion citizens—and the world.

Further Reading

Governing the Climate

An interview with Navroz Dubash on COP28, the history of international climate diplomacy, and the developmentalist turn in climate politics

Indian Big Business

The evolution of India’s corporate sector from 2000 to 2020

Washington-Paris-London Calling

Modi, Mottley, Zelenskyy’s attempts to change the existing world order

Further Reading

Governing the Climate

An interview with Navroz Dubash on COP28, the history of international climate diplomacy, and the developmentalist turn in climate politics

An interview with Navroz Dubash on COP28, the history of international climate diplomacy, and the developmentalist turn in climate politics

Indian Big Business

The evolution of India’s corporate sector from 2000 to 2020

“The systemic, long-term nexus between the political elites and big business will not go away anytime soon,” wrote journalist M. K. Venu in 2015. Writing...

Washington-Paris-London Calling

Modi, Mottley, Zelenskyy’s attempts to change the existing world order

On June 22, three leaders of developing countries made expeditions to three different Western capitals to plead their case for greater support from the rich...