June 14, 2025

Analysis

Industrial Policy and Imperial Realignment

Growing asymmetries in global development

More than 2500 industrial policies were recorded in 2023—more than half of them from the US, Europe, and China. Advanced economies and developing countries alike are embracing more interventionist policies and engaging in policy experimentation.

Across the former, industrial policy now drives advances in artificial intelligence (AI), semiconductors, quantum computing, and clean energy; strengthens supply chain resilience; and “reshores” critical production. Across the latter, industrial policy is leveraged to integrate firms into global value chains, attract foreign investment, and enable “green industrialization” through critical minerals extraction and renewable energy production.

The normalization of industrial policy could mark a historic shift for developing countries. Over the past four decades, their ability to autonomously deploy industrial policies has been severely restricted, in a process described by Ha-Joon Chang as “kicking away the ladder” of catch-up development. A new consensus that re-legitimizes these tools could provide them with greater policy space to pursue instruments and practices hitherto off limits.

Yet the multiplication of industrial policies signals neither normalization nor consensus. Rather, industrial policy is increasingly the object of contestation over the norms and practices of state interventionism. Key actors—including advanced economies, emerging powers, and global governance institutions—diverge over (1) its appropriate form (2) its governance (3) its scope, (4) its objectives, and (5) the policy space available for state-driven experimentation.

In practice, industrial policy is being deployed asymmetrically across the global economy. Both the capacity to pursue transformative industrial policies and the form that enacted industrial policies take remain enormously shaped by global financial and monetary hierarchies, integration into global supply chains, and geopolitical positioning. The pace at which advanced economies and less-developed countries are adopting industrial policies is diverging, with the former better positioned to take advantage of the current period of turbulent change. The policy tools and instruments primarily mobilized by advanced and less-developed economies also differ significantly, reflecting unequal capacities for industrial policy experimentation. These differences are reflective of structural imbalances of state agency within the global economy: advanced economies operate with few restrictions, geostrategically significant emerging economies enjoy selective flexibility, while low-income countries face continued marginalization.

A transforming policy space

As critical development scholars have long argued, the past four decades have seen a significant erosion of “development policy space”—the ability of states, particularly in the global South, to autonomously design and implement national development strategies. Such constraints have been particularly acute in industrialization efforts, where developing states encounter legal, financial, and institutional barriers to deploying interventionist policies.

These constraints have stemmed from three primary sources: (1) the dominance of neoliberal policy norms, entrenched through structural adjustment programmes and conditional lending under the Washington Consensus; (2) binding international economic law, particularly within multilateral trade and investment agreements; and (3) provisions embedded in bilateral and regional trade and investment agreements. Collectively, these constraints have severely limited the ability of developing countries to pursue industrial policy, effectively impeding catch-up development.

The renewed interest in industrial policy may signal a loosening of these constraints. First, the ideological dominance and—perhaps more accurately—coherence of neoliberalism have waned, weakening the appeal of policies that prioritize limited state intervention and the primacy of the private sector in development. As a result, spurning industrial policy has become increasingly difficult, particularly as advanced economies themselves adopt more interventionist strategies. While a coherent alternative paradigm to neoliberalism has yet to emerge—with emergent forms of state capitalism intersecting with extant market-oriented imperatives—we may be entering what Ilene Grabel terms a period of “productive incoherence” in global economic and financial governance, a phase of unsettled development norms in which policy experimentation is increasingly possible. The absence of a coherent and effective disciplinary framework arguably expands policy space and the scope for experimentation with instruments that diverge from the “traditional” neoliberal playbook. Further, there is scope for such experimentation to shape the formation of new global norms on the issue.

Second, the erosion of the multilateral trade regime offers potential flexibility for developing countries to implement industrial policies. The World Trade Organization’s (WTO) dispute system has been effectively neutralized by the US blockage of all new Appellate Body appointments. As Kristen Hopewell highlights with regards to Indonesia and India’s export restrictions and subsidy programs that violate WTO rules, developing countries have exploited this legal vacuum—what she terms “appealing into the void”—to continue industrial policy practices deemed inconsistent with WTO rules. This could embolden policymakers in the global South to pursue industrial strategies without immediate fear of legal repercussions or consequences.

Persisting constraints

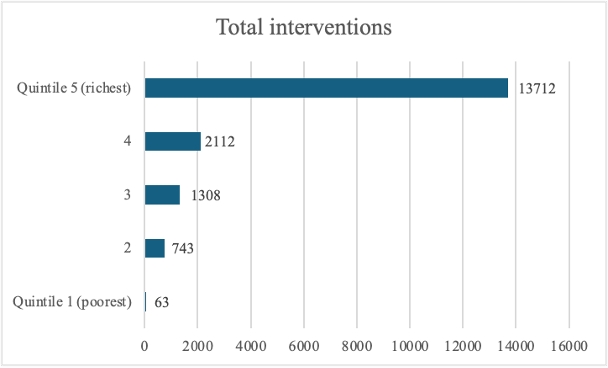

Despite its promise, the revival of industrial policy space cannot be divorced from broader structures of power in the global financial and monetary system. Empirical evidence confirms a stark asymmetry in industrial policy deployment, with wealthier countries implementing significantly more interventions than their lower-income counterparts.

Table 1: Global incidence and distribution of industrial policy according to country-income quintile (GDP per capita), 2010-2022.1Adapted from Juhász, Lane and Rodrik (2023)

The ability to deploy industrial policy is deeply shaped by financial and monetary constraints. Compared to advanced economies, emerging and developing economies (EMDEs) face greater fiscal limitations, including lower tax revenues and an inability to borrow in domestic currencies. Consequently, they depend on external financing for development and industrialization—often under restrictive conditions that constrain policy autonomy. Under conditions of “international financial subordination,” developing countries are particularly vulnerable to financial and exchange rate instability, sudden shifts in global liquidity conditions, and precarious sovereign borrowing. Sustaining external capital inflows typically requires offering high returns to international investors, reinforcing incentives to adhere to conservative economic policies despite the growing space for industrial policy experimentation. In developing contexts where foreign investment is perceived as risky, even minor deviations from economic orthodoxy risk triggering the risk of capital flight and/or non-investment, making policy experimentation a costly prospect.

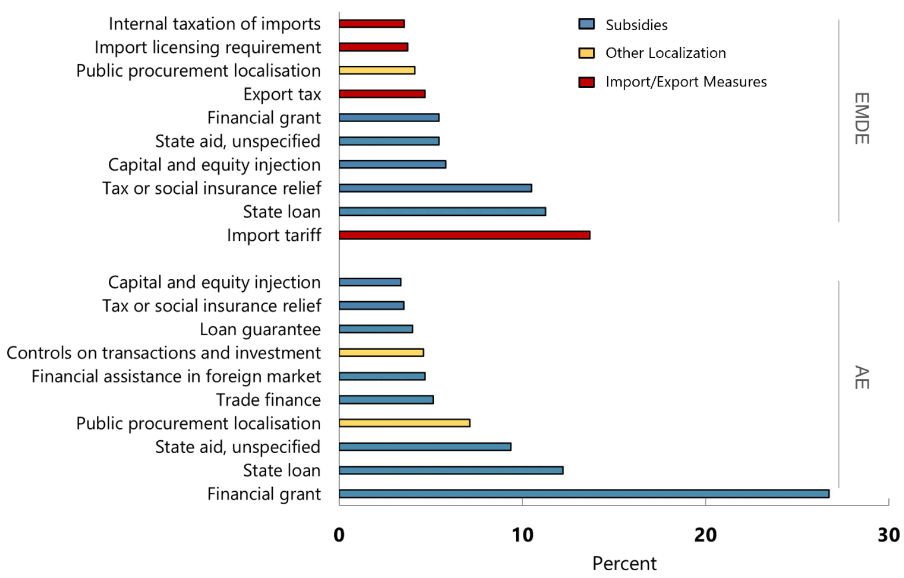

Moreover, the form industrial policy takes—namely the concrete mix of policy tools, instruments, institutional arrangements, and regulatory frameworks—differs markedly between EMDEs and advanced economies. As Figure 1 illustrates, EMDEs primarily rely on “trade-distortive” measures, such as import and export restrictions, whereas advanced economies make greater use of direct financial grants and state aid—policy instruments that depend on government expenditure. While this general trend has been complicated by the Trump administration’s recent implementation of a raft of trade-distortive tariff measures, and the specter of concomitant in-kind responses by advanced economies worldwide, it is nevertheless true that there is a North-South divide in terms of the form of industrial policy implemented.

Figure 1: Trade Distortive Industrial Policy Tools in 2023 by Income Group2Evenett et al., 2024

This divide is also a consequence of the South’s financial subordination. Where industrial policy is deployed by countries dependent on external investment, policy packages are likely to rely more on “carrots”—such as generous subsidies, grants, tax incentives, subsidized loans, and guarantees—rather than ‘sticks’ like hard rules, limits, or penalties. Industrial policy in these contexts is also more likely to rely on price signals and market coordination rather than a strong state-led directive or disciplinary approach. It is also likely to adopt a narrow form of government intervention focused on adjusting risk-return profiles in strategic industries and sectors, or “de-risking” projects as a means to crowd-in private investment. However, the widespread use of such de-risking strategies entrenches financial dependencies, particularly for countries already structurally subordinated within global financial and monetary hierarchies, further increasing their risks of and exposure to debt distress and sudden capital flight.

This is not to suggest that developing countries lack agency in designing and implementing industrial policy plans in pursuit of strategic visions. It does however reveal that industrial policy operates within a global political economy shaped by power asymmetries and the subtle violence of the global monetary and financial system. The critical question is, therefore, not simply whether industrial policy space is expanding, but rather what kind of industrial policy is being pursued, under what conditions, and at what costs; particularly regarding public transfers to the private sector and the reinforcement of existing power and economic inequities.

Geopolitical competition

Intensifying geopolitical competition is both driving and shaping many of the structural imbalances. Technologically advanced economies are engaged in a process of competitive emulation, where industrial policies are strategically and continually deployed in response to the policies deployed by geoeconomic rivals. This industrial policy race generates a multiplier effect particularly evident in subsidy competitions—such as the “green subsidies race”—and escalating defensive trade measures, including tit-for-tat tariffs on electric vehicles.

Certain developing countries are particularly well-positioned to benefit from this geopolitical competition. Referred to as “connector countries” by the IMF or “geopolitical swing states” by Goldman Sachs, nations such as Hungary, Poland, Morocco, Vietnam, Indonesia, Malaysia, and Mexico stand to gain due to their geostrategic proximity to key markets and/or possession of strategic assets, including critical transition minerals, established export-oriented industries, and abundant skilled labor (or combinations thereof). These countries are also prime candidates for “China+1” strategies, whereby firms seek to reduce exposure to geopolitical risks by diversifying production beyond China.

The EU Green Deal, for instance, promotes domestic cleantech investment while sourcing renewable energy from African countries such as Morocco, Namibia, and South Africa. Further, and even prior to the recent raft of tariff measures by the Trump administration, the US has been restructuring strategic supply chains to reduce reliance on Chinese firms through “reshoring” and, more significantly, “friendshoring”—deepening economic ties with allied states. Heightening US-China tensions may benefit countries such as India, where Apple is now looking to source the entirety of the more than 60mn iPhones sold annually in the US by the end of 2026.

Many “connector countries” and others in the global South are actively scaling up their industrial ambitions in response to this evolving geoeconomic landscape. Some have adopted a strategy of “polyalignment,” leveraging diverse financial partnerships to fund industrial development while avoiding alignment with any single country or geopolitical bloc. Their objective is to attract investment by positioning themselves as stable and strategic partners for multiple global powers.

Morocco, for instance, is courting investment from a wide range of partners—including France, Germany, Spain, the US, China, the UK, Portugal, Turkey, the UAE, Saudi Arabia, Israel, South Korea, and Russia—to finance its green industrial policy. This “polyalignment” strategy has been highly successful so far, with announced greenfield FDI in Morocco surging from $3.8 billion in 2021 to $20.4 billion in 2023. Similarly, Vietnam has attracted substantial FDI inflows in manufacturing from Singapore, Japan, the US, Korea, and China, recording $4.33 billion in January 2025 alone—a 48.6 percent year-on-year increase. Mexico has also seen a wave of investment in its electric vehicle (EV) sector by Tesla (US), CATL (China), alongside European and Korean firms. Likewise, Indonesia has pursued an aggressive strategy of attracting foreign investment into “new developmentalist” projects in nickel mining and downstreaming, which saw FDI reach $55 billion in 2024, a 21 percent increase on the previous year, with the top four sources being Singapore, China, Malaysia and the US. Thus the combined expansion of industrial policies driven by competition over advanced technological sectors may, in turn, spur further industrial policy experimentation in some global South countries.

Rebuilding the ladder?

Though it presents new opportunities, this new context preserves the overwhelming power imbalances that characterize the global economy. Developing countries remain dependent on policy shifts and changing priorities of the wealthier nations in the global North.

For example, having made a concerted effort to utilize its nickel deposits to develop industries producing key components of clean-energy technologies—such as EV batteries—Indonesia found itself partly locked out of its biggest intended market, the US, once the Inflation Reduction Act (IRA) was passed in 2022. The IRA excluded from its subsidies any products made by entities with more than 25 percent Chinese ownership. With Chinese companies constructing 90 percent of Indonesia’s nickel smelters and establishing several battery-focused processing plants, this left the country’s industrial strategy stranded, and despite several attempts at negotiating exemptions, the US refused to budge on the issue, insisting that Indonesian significantly reduce China’s role in the industry, a difficulty given the paucity of alternative funding sources.

Competition may also cannibalize developing countries, particularly those within the same region, as they compete for investment and industrial opportunities. For example, Hungary, Czechia, Slovakia, and Poland are competing to position themselves as an EV production and export base connecting East Asian and European supply chains to rich western European markets. But ultimately, French, German, Korean and Chinese automakers will choose to invest in a limited number of production sites. Hungary, Serbia, Slovakia, Poland, and the Czech Republic simply cannot all become critical nodes of EV production networks in Central and Eastern Europe. Similarly, in Asia, not everyone can benefit from “China+1” strategies. India, Vietnam, Thailand, Cambodia, Malaysia, and others fiercely compete over key segments of the semiconductor, photovoltaics, and electronics supply chains, with risks of a race to the bottom. Further, China already dominates key supply chain nodes and actively pursues industrial policy. Its monopolized control over critical machinery, heavy equipment, and critical transition minerals makes it especially difficult for other countries to establish high-value manufacturing.

In recent months, China has tightened its formal and informal export controls on EV battery and critical mineral processing technologies in response to the US and EU’s increasingly aggressive tariffs on EVs and other commodities. This is not only hampering the ability of Taiwanese, American, and other firms to move part of their manufacturing and assembly operations out of China in response to geopolitical risks, but the Chinese party-state is also explicitly targeting India in a bid to prevent the latter from positioning itself as a privileged destination for the relocation of manufacturing operations. In short, China is using its control of strategic economic networks to sabotage another country’s attempt at polyalignment.

The chaotic return of Trump to the White house also adds considerable risks and uncertainty to the economic prospects of “connector countries.” The problem is not only Trump 2.0’s erratic behavior and his systematic use of bullying as a mode of power, it is also that his reckless deployment of tariffs to reshape the contours of the world order risks upending the global trading system and the international financial architecture. Needless to say, this would not bode well for polyalignment strategies and export-oriented industrial policies in the global South.

Finally, while environmental goals, manufacturing jobs, and economic growth are often framed as complementary, their pursuit through competitive industrial policy in fact creates tensions between them. Green development depends on effective industrial policy, yet its uneven application poses broader risks, particularly as wealthier nations’ climate policies remain unilateral, highly competitive, and often exclusionary. By limiting the diffusion of key technologies, intellectual property, and know-how, and erecting trade and investment barriers in the name of geopolitical competition, these policies risk making clean technology more expensive and slowing the global energy transition. Thus, for example, by excluding Chinese EVs from its market, the US has little chance of meeting its emission reductions targets, given the underdeveloped state of the industry in America. In short, when multiple countries pursue green industrialization policies simultaneously, success in (re)industrialization for some may come at the expense of others.

Towards a three-tiered hierarchy of global industrial policy

Taken together, these dynamics may deepen and ultimately consolidate a three-tiered hierarchy of global industrial policy deployment. At the top of this hierarchy, rich technologically-advanced economies with vast fiscal capacities and strategic control of global value chains may enjoy wide latitude in deploying increasingly muscular industrial policies as they aggressively compete with each other, while attempting to contain economic crises, domestic political polarization, and accelerating climate change. These already structurally advantaged nations would consolidate and extend their economic lead and technological supremacy.

The second group would comprise geostrategically significant large emerging economies with selective flexibility to deploy industrial policy to position themselves as key nodes in restructured production networks, rather than passively integrate into global markets. Their success would depend on their ability to secure technology transfers and favorable financing terms, particularly with respect to clean tech and climate finance. It would also depend on their ability to navigate a turbulent geopolitical context and rapid realignments in the imperialist hierarchy of global capitalism. This in turn will influence their ability to craft ambitious, long-term green industrial strategies that promote structural transformation, ecological sustainability, and broad-based development.

For many other developing countries, however, policy space is likely to remain severely constrained and policy experimentation will carry heightened risks. External conditions will continue to demand deference to the perceived exigencies of private investors and these countries may be increasingly vulnerable to the whims of hegemons old and new.

The greatest risk, then, is that the contemporary industrial policy revival does not rebuild the ladder of catch-up development, but raises it further out of reach. In sum, it may not only leave some countries behind, but marginalize them further.

Further Reading

Development, Growth, Power

An interview with Amit Bhaduri.

Amit Bhaduri was internationally selected professor at Pavia University and visiting Professor at the Council for Social Development, Delhi University. His six books and more...

Industrial Experiments

Variants of industrial policy in the global South

The turn of the twenty-first century brought a reassessment of development economics. The global commodity boom of the 2000s ushered in windfall profits for resource-rich...

Sectoral Strategy

Free trade and the resurgence of industrial policy in Africa

Industrial policy in Africa is back. Beginning last January, Nigeria moved forward with the second phase of its “Sugar Master Plan,” a flagship industrial policy...