October 30, 2025

Analysis

Mexico’s Big Green State

Claudia Sheinbaum plans to repurpose the country's state-owned enterprises towards decarbonization

At Claudia Sheinbaum’s first State of Affairs speech, the President announced the passage of fourteen new energy sector laws after only eleven months in office. Sheinbaum’s series of reforms mark a new era for state-coordination in the energy sector, a vision that has triggered a wave of criticisms from the business community and beyond.

Take, for example, the opinion of Mexican leading climate expert Dr. Adrián Fernandez, who, at the time of Sheinbaum’s election, told the Washington Post that Sheinbaum’s climate views “are incompatible with her promises to continue many of López Obrador’s energy policies […] like strengthening the national oil and electricity companies.” The comment suggests that ambitious decarbonization efforts are incompatible with an energy sector characterized by dominant state-owned enterprises. It is the latter with which many business leaders are primarily concerned.

Critics of the active state in Mexico allege that market intervention generates underinvestment. Furthermore, they claim that Mexican state-owned enterprises (SOEs) are not adequate to competently navigate new waves of technology. And, in the wider North American context, SOEs are thought to put Mexico’s industry in jeopardy by triggering mechanisms of investment protection.

The suspicion of SOEs—whether in general, or specific to the green transition—is unfounded. Most private investment in renewable energy across the globe has been facilitated by long-term supply contracts from SOEs or central government agencies. Out of all solar and wind energy projects, two-thirds are held by Chinese SOEs (incidentally, China has recently confirmed an impressive target of 3,500 Gigawatts of solar and wind by 2035). And new forms of intervention in the energy sector are welcome by investors searching for low-risk investments with long-term return profiles.

Moreover, utility SOEs have played a crucial role in technological renovation worldwide. In Mexico, the Federal Electricity Commission (CFE) transformed the natural gas supply system in 2015, following two decades of failure by the private sector in a liberalized gas market. Regionally, the existing regulatory environment will necessarily need to adapt as new technologies join the portfolio of solutions in energy generation, storage, and demand management. While risks are high under a shifting regime, the US’s gradual turn towards a negotiated approach to technological change may minimize the impacts.

Far from representing an obstacle to Sheinbaum’s climate objectives, it is precisely through SOEs that the President is pursuing her vision for the green transition. Her administration has reinforced AMLO’s program to revive Mexico’s SOEs—Pemex and CFE—with new decarbonization and industrial policy ambitions.

On some policy issues, the difference is one of means rather than ends. For example, in order to increase the share of low-carbon electricity by 10 to 20 percent—a commonly agreed policy aim—Sheinbaum’s government has tasked SOEs with orchestrating investment, and turned to state regulatory capabilities to ensure private sector investment. In other cases, the ends themselves have become more ambitious: in the absence of private investment in the EV market, the government has initiated a new business venture, Olinia, to manufacture small urban EVs and launched a lithium battery industry.

Under Sheinbaum’s leadership, CFE has committed to investing in concentrated solar power, PEMEX has announced entry into lithium extraction in oil brines, and a revamped railway agency has commandeered unused infrastructure and land rights to create a state-owned nationwide network of passenger trains. These policies have been pursued with a redistributive orientation. Sheinbaum’s government has pledged to achieve universal electricity access largely with solar PV, as well as to provide free solar panels to low-income populations vulnerable to heat stress at no cost, with federal funding but through the implementing capacity of CFE.

From a governance perspective, the most striking change has been the creation of an Energy Planning Council tasked with coordinating investment and steering the development of technology to resolve endemic problems of energy access and poverty. As I’ve argued with electricity sector expert Naxcitli Calva, Sheinbaum’s government has made planning a pillar of governance as important as regulation—which was traditionally the only form of governance in the electricity sector 1 Under the previous governance model, the Ministry had a consultative council on clean energy which, at its height, contributed to reviewing renewable energy goals and proposed specific incentives policies for renewable energy, serving to legitimize policy making through NGO and academic participation. These types of stakeholders had formal positions in the council, and could see their specific proposition being included in policy documents stating lists of actions intended during the administration, called sectoral or special programs. For participants having to provide proof of impact to donors, these documents could become critical evidence of influence. .

Sheinbaum’s proposed SOEs reforms are part and parcel of a “Big Green State,” one that redefines the role of traditional energy SOEs and establishes their importance in manufacturing to pull the private sector into strategic business ventures. If successful, Sheinbaum’s bet will ensure that strategic assets of decarbonization are owned and operated by the government.

The formation of this Green State is important not just because Mexico stands as the largest fossil fuel consumer south of the United States. It’s also important because it presents an opportunity to explore innovative approaches to mobilizing state capacity for decarbonization and expanding the notion of what is feasible in the international policy landscape.

Liberalization without Decarbonization

Mexico’s post-war energy sector was built on the pillars of state ownership. This gradual process began with the nationalization of the oil industry in 1937 and culminated with the nationalization of the electricity industry in 1960. Generation capacity grew primarily through investments by the state-owned company, Comisión Federal de Electricidad (CFE), in hydro, fossil fuel, and geothermal power plants. It wasn’t until the late 1980s that CFE developed its first (and only) nuclear energy project that opened in 1994.

A turning point would come in the 1990s, when the government of Carlos Salinas oversaw legislative approval of reforms that enabled private ownership in energy generation to more closely align with a US growth model. The financial crises of 1994 and 1997, coupled with the electoral victory of a right-wing President Vicente Fox in 2000 after over seventy years of dominant party rule, accelerated this liberalization process 2 However, these governments lacked the political support needed to amend the Constitution until 2013 .

Between 2013 and 2015, a center-right legislative coalition (which in 2024 would become the anti-Morena electoral coalition) approved constitutional reforms and a long list of legal changes to open energy markets. The energy model promised to double the size of oil and gas extraction by private companies and refocus the electricity utility towards the energy transport business, diminishing its role in power generation.

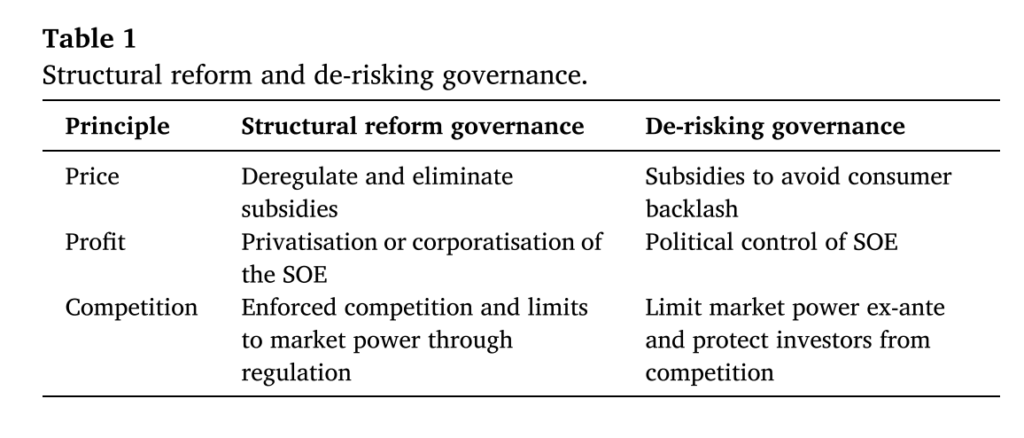

But before the ink could dry, the utility was already signing contracts to derisk the most significant historic expansion of natural gas transportation from the United States—making the company one of the largest purchasers of US natural gas. One after the other, new segments of energy markets developed under a state-derisking model, first gas contracts and then long-term electricity contracts. As illustrated in Table 1, the Mexican Right and Liberal approach to derisking through utilizing state-owned enterprises should not be confused with a structural reform approach, as it relied on SOEs to balance conflicting political goals. But it nevertheless represented a liberal derisking model focused on public-private partnerships and a thin regulatory state.

Liberalization did not lead to decarbonization. In fact, the liberalization trajectory coincided with the global shift towards natural gas combined cycle (NGCC) power generation technologies. And since the US had emerged as a leading producer of natural gas from shale deposits by the 2010s, between 1999 and 2016, Mexico’s SOE contracted more than 15 GW of NGCC capacity. Private entities developed a similar amount of capacity through self-supply and bilateral contracts. This was followed by more than 11 GW under long-term contracts, mostly for wind and solar power. Yet, the reliability of the system still depended on the portfolio of generation and electricity grid owned by the state.

Betting on state prevalence

This is the model that the AMLO government sought to contest. Instead, it argued for the need for SOEs that could invest, own, and operate their power plants and use the public company balance sheet to protect the final consumers from the instability of global and regional energy markets.

Sheinbaum’s reforms intend to implement this vision through an orchestrated transformation of the governance paradigm, focusing on coordination as well as the creation of a strong (but not independent) regulatory apparatus benefiting from the new planning system.

In 2024, over 60 percent of the country’s electricity generation came from NGCC, with clean energy under 20 percent 3 This was in the midst of a historical drought that cut hydropower a couple of percentage points from total power generation , as described in Table 2. But Sheinbaum’s announced plans would put clean power generation at 38 percent by 2030 with both state and private sector participation.

Table 2: Power generation (2024)

| Technology | GWh | TWh | % | Category |

| NGCC | 212,819 | 286 | 81% | Thermal |

| Thermal (other) | 44,092 | |||

| Coal | 12,968 | |||

| Nuclear | 11,978 | |||

| CHP | 3,912 | |||

| Hydro | 23,800 | 67 | 19% | Clean |

| Wind | 19,987 | |||

| Solar PV | 18,640 | |||

| Geothermal | 3,576 | |||

| Bioenergy | 533 |

These decisions bear important implications both for domestic consumers and for the international business community. While electricity consumption in the UK has diminished by one fourth since the Great Financial Crisis of 2008-9 (309TWh in 2023), Mexico’s has grown by one third in the same period and could easily double or triple by mid-century (358 TWh in 2023). Mexico is one of the largest growing energy markets outside the US and China.

Where is additional demand going to come from? Prior to AMLO’s government, the lack of direct investment in generation by CFE left a growing share available for private sector supply. Sheinbaum’s legislative reforms have affirmed the political commitment to maintaining 54 percent of power generation in state hands through direct investment from the SOEs, state control over special purpose vehicles with power generation assets, and new forms of co-investment. To avoid the consolidation of debt onto government books, the latter must maintain more than 50 percent ownership by the state but less than 75 percent.

Under AMLO, the government negotiated the purchase of the Spanish conglomerate Iberdrola’s IPPs power plants as a way to resolve a legal and regulatory conflict with the company. The result was a significant increase in assets and generation owned by the state, even if not directly by the state-owned CFE, but through and special purpose vehicle hosted by FONADIN, the National Infrastructure Fund. That particular choice initiated what might turn out to be a wave of innovations in financial engineering within the government and CFE.

According to the latest electricity sector plans, the first under President Sheinbaum’s new legislative package, in 2026 state-controlled assets will generate 54 percent of power, which might grow to 59 percent by 2030, from 41 percent in 2022, as presented in Table 3.

Table 3: Evolution of power generation from state-controlled assets

| Category | Control | 2022 | 2026 | 2030 |

| State | CFE | 41% | 42.6% | 47.5% |

| FONADIN (former Iberdrola IPPs) | 10.7% | 7.0% | ||

| PEMEX | 0.6% | 4.6% | ||

| % State control | 54% | 59% | ||

| Privates | Private IPPs | 58% | 16.3% | 10.1% |

| Privates | 29.7% | 30.9% | ||

| % Private control | 46% | 41% | ||

| Central Planning scenario (TWh) | State control | 139.7 | 201.6 | 243.3 |

| Private control | 197.6 | 171.7 | 169.1 | |

| Gross Generation | 340.7 | 373.3 | 412.4 |

This degree of state intervention might risk triggering a capital strike. The announcement of Iberdrola’s decision to sell all remaining assets in Mexico earlier in the summer of 2025 led several experts to conclude, precisely, that such a capital strike was taking place. Ultimately, another Spanish company, Cox, purchased the remaining fifteen power plants and the pipeline of projects for 4.2 billion, signaling there is a much more diversified ecosystem of investors with the appetite to try out Mexico’s new set of rules.

Furthermore, contrary to the prevailing accounts, Mexico is not wholly dependent on FDI for access to capital and technology, nor are foreign investors unwilling to accept long-term strategic partnerships with states that control key assets. Mexico’s domestic financial environment has changed dramatically since the 1990s: its pension funds have grown to constitute 19.1 percent of GDP in 2024, development banks now contribute 5 percent of GDP in assets (and financed the purchase of Iberdrola assets), and SOEs have encouraged the private sector to embrace financial innovations by funding infrastructure like transmission without affecting the central government balance sheet. Thus, the political economy configuration is open, and the government is in a position to choose which form of private investment will be best suited to participate in the decarbonization of the industry.

CFE will be able to leverage its recent experience in building a 1GW solar PV project in the northern state of Sonora. Having completed its first, the company could replicate these large-scale projects as well as break them down into hundreds of mid-size plants across the country. During the last week of August, CFE announced two projects for concentrated solar power in the region of Baja California Sur, an an electric island disconnected from the country’s grid. Though the plant’s construction has been complicated by weak US technology, it nevertheless underscores the government’s appetite for new technological ventures from the SOE.

For the private sector, the newly announced regulations have opened new areas for exploration in the modernization of the electricity system—from distributed generation to storage and controllable demand. In addition to its 44 percent market share, these new areas underscore the expectation that the private sector’s role is to push the boundaries of market innovations.

What’s in a promise?

Where critics see danger, we should see an open horizon of new opportunities for green investment. The capacity of the state to reconfigure its economic role requires carefully threading creative experiments to push the boundaries of what key actors (credit agencies, investment dispute arbiters, and others) deem reasonable before a backlash from national and international investors materializes.

Two critical tensions emerge from the promise of the Green State. The first and more obvious is opposition by corporate interests whose business depends on the long-term ownership and operation of critical assets in energy and infrastructure: global utility companies and asset management firms. The second is the long-term commitment from SOEs to existing fossil fuel value chains. At the moment, CFE’s overcommitment to natural gas trade represents a short-term barrier to the expansion of renewable energy, unless industrial growth and electrification of the economy create enough demand to make room for CFE’s gas commitments and renewable energy.

But Sheinbaum’s model opens a new constellation of possible strategic alliances. It introduces opportunities to generate competition from technology, construction, and development companies, and it positions PEMEX to manage the scaling down of fossil fuel reliance in the long run. The basis of opposition to this platform, then, is not reflective of the threats it poses to decarbonization. It is instead reflective of the country’s recent history of liberalization, a history which must be challenged and overcome.

Citizens and investors are witnessing (and requesting) a more active role for the state in coordinating and sustaining investment in decarbonization. What is different in Sheinbaum’s platform is not only the scale of expected engagement from SOEs, but the fearless commitment to the underlying principles a Green State requires: trust in the centrality of politics over technocracy and state coordination over markets. Importantly, it demonstrates confidence in the possibility that a developing country can, with the right tools, reach the pinnacle of the technological frontier.

Further Reading

The Fourth Transformation

The political economy of Claudia Sheinbaum’s popularity

As anti-incumbent sentiment toppled governments around the world in 2024, Mexico’s Morena won in a landslide, and the presidency was passed from Andrés Manuel López...

Green Dreams

Towards a green industrial policy made in Mexico

“Industrial policy is suddenly fashionable again; even those who once condemned it now claim they always supported it.” —Ha-Joon Chang For decades, Mexican leaders have...

New Triangular Relations

Security-shoring and trade between Mexico, China, and the US

The confrontation between the two largest global economies leaves Mexico in a fragile and complex triangular relation.