December 5, 2025

Analysis

Missed Opportunities

Lithium and green extractivism in Argentina

Argentina has one of the largest supplies of lithium worldwide and a unique potential to harness it. The northwestern provinces of Salta, Jujuy, and Catamarca account for 13 percent of proven reserves globally. In the salt flats of this long neglected region, four mines produced 72,000 tons of lithium carbonate equivalent (tLCE) for export last year. With two extra mines now ramping up production and five others under construction, this figure is projected to increase to 600,000 tLCE—transforming Argentina into the second largest lithium exporter on earth.

So far, Argentina has predominantly been a passive supplier of the resource: producing it primarily for export without industrial promotion or value addition. The country’s mining and business laws have helped to ensure this subordinate role in the global economy. But with demand for lithium surging thanks to the energy transition, there is now an opportunity to boost industry and create quality jobs. This key metal, which is essential for the expansion of green technologies, could provide a lever for growth and productive diversification in a nation historically afflicted by dependency, poverty, and unemployment. The state could pursue active policies aimed at developing the value chain in new strategic sectors such as batteries and their components.

But not all that glitters is gold. Along with these vast reserves, Argentina also has a government with a deep ideological opposition to internal development. Rather than using lithium to set in motion a process of reindustrialization, President Javier Milei’s hardline neoliberal project aims to attract foreign investment by repealing regulations and imposing austerity, thereby paving the way to “green extractivism.” Its effect will be to reinforce the dynamics of underdevelopment, leading to more primarization and deindustrialization, and aggravating the social problems that flow from them.

Growth prospects

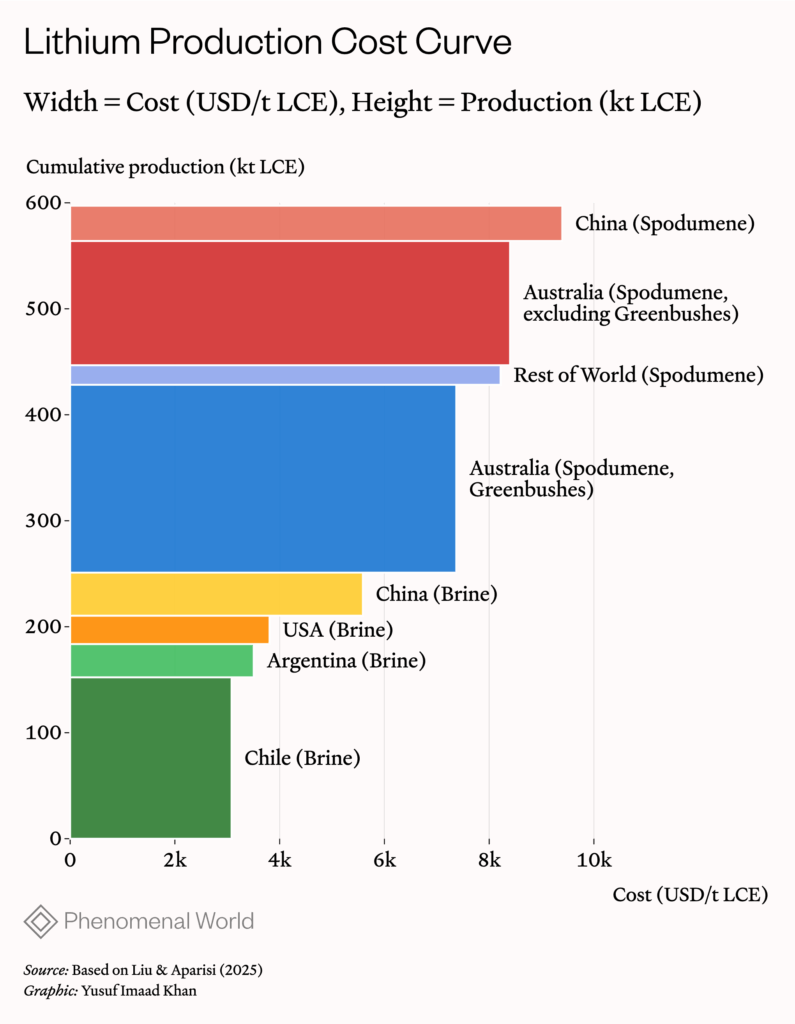

Argentina mainly produces lithium carbonate from brines extracted from these northwestern salt flats. Of the four active mining projects, the two oldest, Olaroz and Fénix, were recently acquired by the multinational mining giant Rio Tinto. The newer ones are the Cauchari-Olaroz mine—whose domestic owner, Minera Exar, is partnered with Ganfeng, the largest lithium mining company in China—and the Sal de Oro mine, owned by South Korea’s Posco. Current production levels may seem modest compared to Chile’s 260,000 tCLE, Australia’s 468,000 tCLE, or even Zimbabwe’s 117,000 tCLE. But what sets Argentina apart is its growth prospects. In addition to the eleven mines that are either fully operational or still in progress, there are also fifty additional projects, from exploration to feasibility studies, at various stages of development, plus reserves vast enough to sustain extraction for decades.

Another factor that distinguishes Argentina is the high grade of the resource. In economic terms, the country is not a marginal producer; its salt flats are one of the lowest-cost sources of extraction in the world. According to various estimates, the average pre-tax cost of lithium extraction in Argentine projects is below USD $4,000/ton: only slightly higher than extraction costs in Chile’s Atacama salt flat, and far below the current world price around $9,000/ton.1Cochilco (Chilean Copper Commission) in its 2024-2025 Market Report, Benchmark Minerals Intelligence, corporate reports from mining companies, and Liu and Domenech Aparisi (2025). The price of lithium is highly volatile. This is the average value for the month of September 2025. Lithium in these South American nations is worth only a fraction of its price in places such as Australia, Brazil, Zimbabwe, or China.

It is not just about the quantity of the resources, however. Argentina has other capacities that could underpin a more strategic approach to the lithium sector: a robust scientific and technological system, strong national universities and research centers, a sophisticated industrial apparatus in manufacturing (including the chemical, metalworking, and automotive industries), skilled workers, and labor organizations committed to the goals of industrial development. All this makes it possible for the state to make active interventions in the lithium value chain, particularly in storage applications.

Over the past decade, a group of actors within these networks has explored such avenues for development. They have created centers near the salt flats with the aim of researching technologies such as direct lithium extraction and extraction methods that minimize environmental harm. They have also supported advances in battery chemistry, cell manufacturing, recycling, and battery safety. In 2022, the National Institute of Industrial Technology (INTI) and the Chamber of Metalworking Companies (Adimra) received funding from the Ministry of Science and Technology to create a lithium battery quality control center—CENBLIT—aimed at building capacity in battery quality regulation.

This research has led to advances in direct lithium extraction technologies, studies on the hydrogeological characteristics of Argentine salt flats, and the continent’s first battery cell manufacturing plant. The manufacture of lithium iron phosphate (LFP) batteries2These are the fastest growing batteries in the last five years and do not require cobalt. The use of this chemistry has led to a significant reduction in battery prices, while the expansion in production scale has resulted in multiple improvements in performance (stability, energy density, charging speed, etc.). by the company Y-TEC, and the installation of a plant (UNILIB) to manufacture battery cells in association with the National University of La Plata, are two salient examples.

Between 2012 and 2021, the state invested $5.7 million in projects related to lithium and its value chain through competitive public funding. If we add the work carried out through national universities, the CNEA, the INTI, and the UNILIB plant with funding from Y-TEC, the monetary efforts are multiplied several times over. Such state-led ventures were not always adequately funded, nor could they bring about a decisive transformation in the sector’s development prospect, but they were nonetheless effective in expanding the country’s technological capabilities, and signaled a clear intention to seize this developmental opportunity.

Obstacles

Yet there was a much wider range of actors with little interest in this project. In the private sector, the dominant multinational mining companies cannot be expected to revive the country’s industrialization or improve its geoeconomic position. They base their calculations on the quality of the resource and ease of access to mining properties, rather than any broader considerations. Today, mining firms such as Rio Tinto, Minea Exar, and Ganfeng have one primary aim: to guarantee the supply of critical minerals in the face of growing fragmentation of supply chains, trade wars, and disputes over productive hegemony in critical sectors such as batteries and electromobility.

Nor are many politicians willing to pursue a long-term industrial strategy. Argentina’s 1994 constitutional reform defines the provinces as the owners of the natural resources in their territories and gives them authority over their use: a provision which gives provincial leaders significant power to resist national government intervention in fiscal, environmental, and industrial matters.3For example, in terms of environmental or fiscal control, some provinces did not support the EITI (Extractive Industries Transparency Initiative) initiative, whose adoption was promoted by the national government with the aim of increasing transparency in the operations of extractive companies. Since they stand to benefit from attracting foreign investment in the exploitation of new salt flats, many of them oppose the kind of state policies that would incorporate local added value or develop suppliers and technology transfer. They argue that such development planning would discourage investors and help the productive center more than the extractive provinces.4 For example, they strongly criticized the installation of the YTEC battery plant (see below) in the province of Buenos Aires. Their position aligns with that of national politicians who similarly favour capital inflows—used to develop salt flats and expand exports of lithium carbonate, chloride, or hydroxide—over creating higher value-added links in the chain that stretches from natural resources to battery production.

Moreover, the severe constraints on the Argentine economy, which have only gotten worse as Milei has deepened the country’s external indebtedness, give politicians an extra incentive to attract mining companies—as a means of generating foreign exchange and thereby loosening the stranglehold of debt. Yet this is ultimately a self-defeating strategy whose aggregate effect is to deepen such financial instability. Historical experience shows that foreign investment, when concentrated in the production of raw materials and the creation of export enclaves, tends to accentuate structural problems with the balance of payments rather than resolve them. Once investments mature, the foreign exchange balance can even become negative—creating a situation of volatility that is compounded by changes in international commodity prices.

Enter Milei

Despite the urgent need for an expansion and diversification of Argentina’s exports, the policies of the Milei government, which came to power in 2023 on a right-wing libertarian platform, are now pushing in the opposite direction. Contrary to the prevailing global trend of active industrial policies and protection of strategic resources, Milei last year implemented the Large Investment Promotion Regime (Régimen de Fomento a las Grandes Inversiones, or RIGI), which provides extraordinary incentives for extractivist projects—consolidating a liberal regulatory framework that works in their favour, and militating against previous attempts to build a different model. Precursors to the current law include the Mining Code and the Mining Investment Law: the former regulates the conditions for granting concessions and is specifically aimed at protecting the extractive business from state “discretion,”5The provinces can dictate their administrative procedures and grant concessions. However, the law requires provincial administrations to accept applications that comply with the law. Once granted, these concessions can be transferred without prior authorization. This situation encourages the proliferation of projects and a high degree of fragmentation of the mining cadastre, leading to significant real estate speculation. while the latter, in addition to providing fiscal stability and tax exemptions, sets a ceiling on royalties of 3 percent of the value at the mine mouth, which translates into less than 2 percent of the export value.

Along with the Basic Law—Milei’s Omnibus bill of December 2023, aimed at deregulating the economy and privatizing public companies and agencies—the RIGI represents the relinquishment of all sovereign capacity to define industrial development objectives around extractive projects. It encourages investment in mining (especially lithium) as well as hydrocarbons,6Seven projects have so far been approved: two related to hydrocarbons, two related to renewable energy, one related to steel, and two lithium projects belonging to the Australian companies Galán and Rio Tinto. It is important to note that the lithium project presented by the Chinese company Ganfeng was not approved. offering tax exemptions and tax and customs stability, while allowing projects under its purview to avoid bringing foreign currency from exports into the country.7 In other words, income from strategic exports is exempt from being deposited and settled in the foreign exchange market in the following proportions: during the first year, 20 percent of exports will be freely available; during the second year, 40 percent; and from the third year onwards, 100 percent of export income will be freely available. It curtails the prospect of an effective industrial policy, closing off strategic paths to onshore higher stages of lithium’s value chain—for instance by preventing the national government from implementing quotas or export bans. It also limits local content requirements, local supplier development, and even R&D or technology transfer. Finally, the bill cedes sovereign powers by giving different international bodies the authority to settle commercial disputes, with investors able to choose between the Arbitration Rules of the PCA (Permanent Court of Arbitration), the Arbitration Rules of the International Chamber of Commerce, or the ICSID (International Centre for Settlement of Investment Disputes) of the World Bank.

The RIGI thus transforms Argentina into one of the countries in the region with the most lax mining regimes. This makes for a stark contrast with neighbouring Chile, where the National Lithium Strategy ensures that only joint ventures with state-owned companies, such as Codelco and Enami, are granted access to Special Lithium Operation Contracts (CEOLes) in new salt flats. Whereas Rio Tinto is the sole actor in a lucrative RIGI project, for example, just across the mountain range it must partner with Codelco to access the resource—giving the state a more central and strategic role. Existing projects in Chile meanwhile face sliding royalties of between 6.8 and 40 percent of the sale value, as well as being required to contribute to the communities in which they operate and to invest in R&D requirements. In order to sell at a preferential price on the domestic market, they must make 25 percent of their production available. With this value-added policy, the Boric government hopes to dramatically increase national capacity for the production of battery materials and components.

Another example of greater interventionism from outside the region is Zimbabwe, which since 2022 has been promoting restrictions on exports of unprocessed minerals with the aim of increasing export value and improving local industrial capabilities. The government recently announced that it will ban the export of lithium concentrates from January 2027, extending its value-added strategy in a similar vein to that which Indonesia is pursuing with nickel. Such policies have not stopped investment or undermined production in either Chile or Zimbabwe. Chile went from exporting 114,000 tCLE in 2020 to 261,000 tCLE in 2024, charging royalties of around 40 percent during the international price boom that took place during this period. Zimbabwe went from 2,000 tCLE to 117,000 tCLE between 2020 and 2024.

The results in terms of value added remain variable: while Chile’s use of quotas has not yet brought any meaningful investment, Zimbabwe has had more success in driving investment in processed products such as lithium sulfates as part of its industrial strategy. But regardless, these examples from abroad illustrate the extent to which Argentina is failing to lay the foundations for a new dynamic core of industrial and technological development. Milei’s anti-industrial outlook is also clear from his government’s underfunding of science and technology and its dismantling of institutional and industrial capacities. His abandonment of initiatives like YPF’s lithium and battery project, combined with his singular focus on attracting large investments in extractive industries, will have profound social and environmental implications.

Reprimarization, deindustrialization

The energy transition is reshaping production paradigms globally. Significant cost reductions and improvements in the efficiency of clean technologies suggest that, even in the context of the current climate denialism promoted by Trump and other reactionary leaders, the spread of transition technologies will accelerate over the coming years, particularly in renewable energies supported by stationary batteries and electromobility.8Over the last 15 years, renewable wind power generation costs have fallen by 65 percent (from USD 135/Mw to USD 50/Mw), while solar photovoltaic costs have fallen by 83 percent (from USD 359/Mw to USD 61/Mw). Although it is difficult to estimate due to product variability and the specificities of national markets, the International Energy Agency estimates that electric vehicle prices fell by up to 11 percent between 2023 and 2024, which, added to the drop of up to 30 percent in battery charging systems, is significantly reducing the total cost of ownership of an electric car. Batteries have played a key role in this trend, with prices falling by more than 90 percent over the last 15 years. In turn, the fall in the price of lithium and the shift towards LFP (lithium iron phosphate) batteries (which do not contain cobalt) have been the driving forces behind the decline in prices. These are mature technologies that reduce emissions in the most polluting sectors, such as transportation and electricity generation, which together account for more than 60 percent of global emissions. For many countries, the adoption of these technologies is a matter of vital energy security, because it limits dependence on fossil fuel imports.

Without active industrial policies, though, the possibility of participating in these sectors will fade from view. Without a means of structuring competition and production, states will merely reaffirm the existing global division of labor and diminish their industrial capacities. This will entail not only the primarization of Argentine exports, but also the deindustrialization of its entire productive structure. Amid the energy transition, national sectors such as automotive, metalworking, and capital goods are at risk, either because of their growing obsolescence and lack of alignment with global environmental standards, or because of their low level of local integration and a widening technological gap. How to avoid this fate is a question of increasing political urgency.

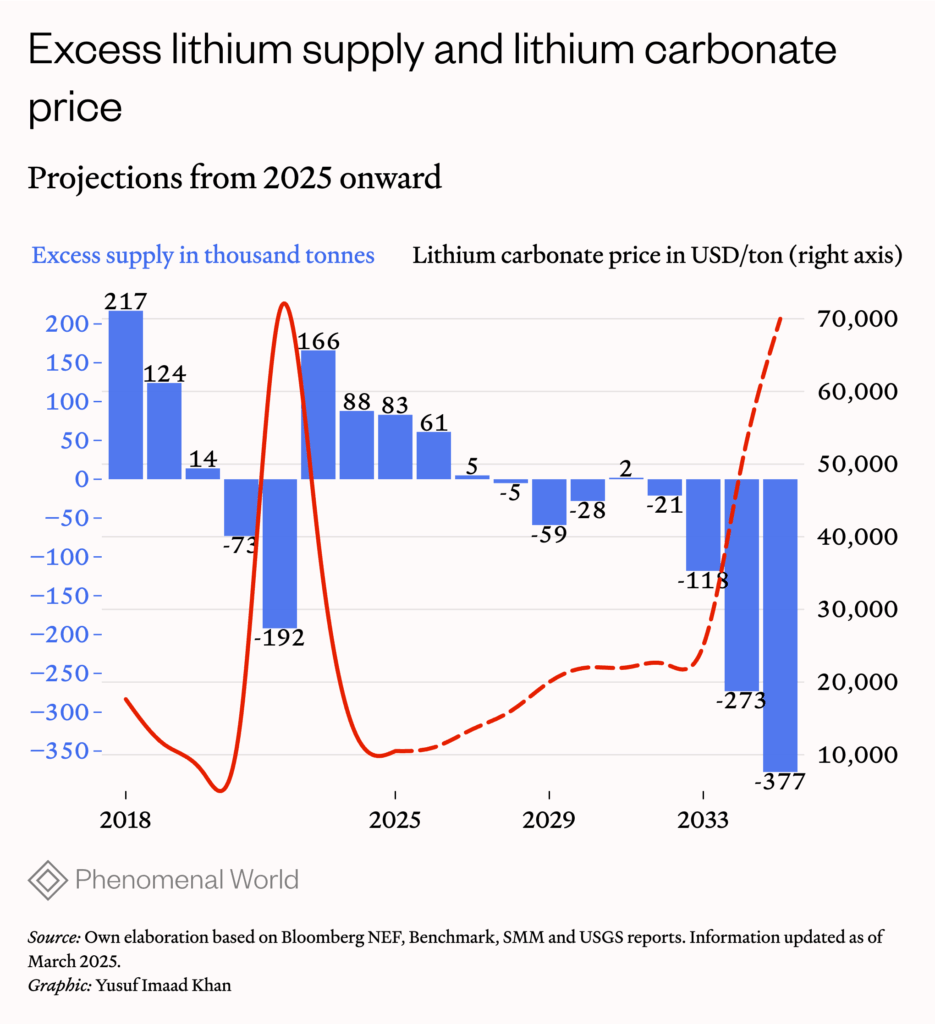

One point of agreement across the spectrum is that Argentina’s productive destiny is tied to its strategic energy and mineral resources. In 2024, exports from hydrocarbons and mining accounted for 20 percent of total exports; it is estimated that this will rise to 30 percent by 2030. The argument made by Milei’s supporters, that the best way to stimulate these sectors is simply to reduce the tax burden and offer other incentives, does not stand up to scrutiny given the international direction of travel. If current predictions are correct, demand for lithium will multiply by a factor of 1.6 over the next five years and 2.5 over the next decade, rising from the current 1.2 million tons of CLE to 3.8 million tons in 2035. This means that, despite the current phase of low lithium prices caused by excess supply, soon enough demand will once again exceed supply and the price will be above USD 20,000/ton.9 Cochilco, S&P Global, Benchmark Minerals Intelligence, among others.

One possible effect of such global trends could be to improve the balance of power for countries like Argentina as they negotiate with companies and investors who are desperate to access such resources. Nations in the Global South could build new strategic capabilities by exploiting this aspect of the energy transition: securing better trade terms and using investment to their strategic advantage. A state like Argentina need not force battery production at source, but it can make consistent progress at successive links of the value chain.10 According to Benchmark Minerals Intelligence, as of July 2025, the price of LFP was around USD 4,900/ton, while that of lithium carbonate was around USD 9,000/ton. However, each ton of lithium carbonate can produce between 3 and 4 tons of LFP. This means that one ton of lithium carbonate transformed into LFP can increase the export value by between 1.8 and 2.4 times. The lithium chain includes various intermediate phases that would represent a quantitative leap in terms of value generation and offer significant opportunities for technological enhancement. In terms of the balance of payments, each ton of lithium exported in the form of LFP cathode material could represent twice as much foreign exchange.11This segment is where much of the product innovation and therefore technological learning is concentrated. For example, in July of this year, China implemented restrictions on LFP exports.

And yet, the horizon of industrial development of lithium is now being eclipsed by the green extractivism of the RIGI. If Milei succeeds in reversing the tentative gains that Argentina has made in this arena, it is hard to see how the country will exercise its considerable bargaining power as the demand for lithium continues to grow. A new cycle of deindustrialization is looming. The time to avoid it is limited.

Further Reading

Lithium Experiments

Chile’s mineral strategy and geopolitical realignment in the global energy transition

Gabriel Boric's government has revived industrial policy to upgrade Chile's role in the green transition. Yet serious obstacles remain.

The Chainsaw and the Miracle

Milei's structural adjustment program.

Argentina's midterm elections have given Milei a renewed mandate to slash the state, working in concert with the IMF and US Treasury.

Argentina’s Debt Trap

Milei’s return to the IMF

After publicly endorsing Javier Milei’s economic achievements since coming to power in December 2023, the IMF has approved a new Argentine bailout package of $20...