July 5, 2025

Analysis

Monetizing Primacy

Trumponomics, dollar diplomacy, and multipolarity

Donald Trump’s second term as President of the United States has not been very good for the dollar. The most recent blow to the currency came when the ratings agency Moody’s stripped the US of its AAA rating. When Standard & Poor’s downgraded the US in 2011, the dollar rallied and Treasury yields fell. This time around, however, the market reaction was different—an extension of the pattern established immediately following the announcement of sweeping global tariffs on April 2. In 2011, the Eurozone crisis was reaching a crescendo, making the dollar the safest haven in the international system. In 2025, the voluntary nature of the crisis has triggered considerably different market behavior. Contrary to the expectations of most economists (including administration officials charged with economic policy making), the so-called Liberation Day tariffs led to a sharp weakening of the dollar and momentary spiking of Treasury yields.

This in turn has fueled speculation of a broader flight from US assets, marked by a Munchian cover story in The Economist raising the shrieking specter of a dollar crisis. There has also been a mounting stream of stories and commentary that US policies were fueling a broader turn in sentiment against the currency—as suggested in this article about China looking at alternatives to US Treasuries, in invocations by Japan’s finance minister of the country’s US bond holdings as a possible negotiating card, and warnings that Asian countries could decide to reduce their exposure to US assets to the tune of $7.5 trillion.

The months since April 2 have clarified the multiple contradictory desires of the Trump administration vis-a-vis its position in the global economic hierarchy. It likes US military dominance, low interest rates, and the extraterritorial powers flowing from dollar centrality, and it would like to keep them. It dislikes trade deficits, supply chain vulnerabilities, deindustrialization, and technological catch-up in its adversaries, and would like to stop or slow them. While these goals are framed largely in terms of the intersection of domestic politics and geopolitics, there are also occasional hints of more traditional—and largely benign—macroeconomic preoccupations at the Treasury. These take the form of a desire for global rebalancing, where economies with large trade surpluses in Northern Europe and East Asia simply increase domestic consumption rather than purely relying on exports for growth.

On the specific question of the dollar itself, Trump administration policy can be characterized as confused. It wants a weak dollar to spur reindustrialization in the US and a strong dollar to offset any inflationary pass-through from tariffs. It certainly does not want a combination of dollar weakness and higher bond yields, which is generally interpreted as a crisis of confidence in the currency. In addition, this administration is increasingly concerned that high bond coupons will increase the deficit and debt, and seems to think that large foreign inflows into US bonds could help hold down interest rates. Finally, it is absolutely determined to retain the centrality of the dollar in the international monetary system, even though several key administration officials believe—mistakenly—that dollar centrality leads to undesirable dollar strength.

Monetizing primacy

Stephen Miran, Donald Trump’s head of the Council of Economic Advisors, has argued that the dollar’s dominance in the international monetary and financial system comes at a cost. In his post-Liberation Day remarks at the Hudson Institute, he said, “While it is true that demand for dollars has kept our borrowing rates low, it has also kept currency markets distorted. This process has placed undue burdens on our firms and workers, making their products and labor uncompetitive on the global stage.” But he simultaneously understands centrality as an essential pillar of American statecraft, because it enables the extraterritorial projection of power through measures like primary and secondary sanctions, along with export controls. In his now-infamous December 2023 memo heralding a coming “Mar-A-Lago Accord,” Miran writes:

If the reserve asset is the lifeblood of the global trade and financial systems, it means that whoever controls the reserve asset and currency can exert some level of control on trade and financial transactions. That allows America to exert its will in foreign and security policy using financial force instead of kinetic force.

Miran also acknowledges that dollar centrality can lead to lower interest rates, “because there is a persistent reserve-driven demand for UST securities, the United States may be able to borrow at lower yields than would otherwise be the case.” He connects the interest burden to the US provision of a global defense umbrella and suggests, borrowing an idea from macroeconomic analyst Zoltan Poszar, that beneficiaries of such protection can be encouraged to finance it by swapping current holdings of short-dated instruments for long-dated debt at below market interest rates: “they could simply write checks to the Treasury that help us finance global public goods.” (This, by the way, is exactly what happened in the second quarter of 1992, when the US ran its only current account surplus as a percent of GDP since 1983, as checks from Gulf allies in the first Iraq war arrived.)

How should we understand this policy mix? Miran’s goal might best be described as an attempt to monetize the US’s primacy. In his words, “The world can still have the American defense umbrella and trading system, but it’s got to start paying its fair share for them.” The desired outcome of his vision retains the United States’ position as global policeman and reserve provider, while making allied nations “participate in bearing the costs.”

But Washington’s current foreign policy trajectory does not seem to be in the business of making allies. Washington has imposed tariffs on a broad swathe of countries, and thrown the status of NATO into question—the preeminent commitment to a US-led international security order. Facing frank expressions of a starkly transactional and hierarchical view of diplomacy—as in the case of Trump’s statement that the US should sell allies aircrafts at a quality discount, in case they aren’t always allies—and extreme economic policy volatility, disincentives are mounting for countries tied financially to this security provider.

The quest for lower US interest rates and for persistent dollar centrality could create international spillovers. On June 17, in a victory for the bipartisan, $119 million 2024 congressional campaign spending spree by the crypto sector, the US Senate passed the GENIUS Act, providing a first step toward a regulatory framework for stablecoins. The global expansion of dollar-based stablecoins—privately-issued digital currency that promises redemption at par—is meant to entrench dollar primacy in the international monetary system and create, per Trump’s crypto czar David Sacks, “trillions of dollars” of additional foreign demand for US Treasuries, thus holding down interest rates. The theory is that this would expand the dollar’s global footprint and the issuers of such liabilities would have to hold US government debt as the counterpart asset. If the theory is proven correct, it would raise a host of financial stability issues both in the US and abroad.

In countries where stablecoins are available legally (or accessible through illegal means), currency substitution or capital flight will be made easier—potentially provoking banking crises as deposits evaporate electronically. This could be especially problematic in portions of the global South, where stablecoins could cripple financial stability and enable corruption on a massive scale.

But it is important to note that the financial stability risks might not be so completely asymmetric that the US is completely immune from them. Anyone fleeing into dollars might decide to flee out of them—if not into their own currencies then into euros, Swiss francs, or crypto. This could happen for market reasons, or because of fears that assets will be blocked or seized—whether as a function of domestic politics in the US or of geopolitical conflict. And should flight like that happen, then the question of the liquidity of the underlying assets and their current valuation could become an issue, particularly if the issuers have (as yet at least) no recourse to traditional lender of last resort facilities. These systemic problems could be minimized if the stablecoin issuer buys nothing but very short-dated Treasury bills, but that is at cross-purposes with the goal of ensuring cheap long-dated funding for the US government—the Washington obsession that ostensibly justifies the stablecoin strategy to begin with.

To sum up, what the administration wants is for the US to remain the world’s dominant military power; the dollar to remain the world’s central currency (because this is an attribute that adds extraordinary powers of economic suasion in the service of maintaining a lead in military technologies); and regular inflows of foreign funds for the US government. These inflows could take the form of revenues (“writing a check”), outsize purchases of American defense equipment by US allies, or long-dated loans from foreigners at low interest rates. Primacy is to be preserved—and it is to be paid for by the rest of the world. In other words, primacy is not just to be maintained, but also monetized.

Does centrality mean strength?

Lurking behind the administration’s multiple policy goals and its insistence on dollar centrality, there is also a complaint that the currency is too strong. But the simple fact is that the causal links drawn between persistent dollar centrality and persistent dollar strength are far more tenuous than claimed. A freely-floating dollar has been central in the international monetary system for about fifty-two years and it has spent long stretches of that time depreciating (the 1970s; 1986–94; and 2002–2008). What seems to drive extended periods of dollar strength (1981–85; 1995–2002; and 2014–present) is less its centrality than investor expectations of the comparative rate of return on US assets. These rates of return were seen as favorable to the dollar in Reagan’s first term, marked by Paul Volcker’s high interest rates and a series of institutional changes vastly more favorable to capital; during the late 1990s tech boom, which coincided with the Asian financial crisis; and, most recently, the massive increase in US energy production that resulted from the shale revolution. The latter changed America’s balance of payments dynamics and dispelled the worry that the dollar could be a poor international store of value for buyers of commodities priced in dollars.

The common argument regarding dollar appreciation asserts that the search for “safe assets” drives the value of the dollar upwards, which leads to boosted imports and reduced exports. The idea is that, through the channel of dollar strength, large capital inflows lead to a widening of the trade deficit, but this is at odds with what happened between 2002 and 2008. During that period, the US current account deficit widened dramatically, reaching the record point as a share of US and world GDP, and yet the dollar fell from 82 US cents to 1.60 against the euro. Thus, the underlying causal mechanism that purports to connect every single instance of outsize American trade deficits to capital inflows that strengthen the dollar seems not to have held in the early 2000s. US trade deficits have widened alongside a strong dollar (1981–85; 1995–2002), and alongside a weak dollar (the 1970s, and 2002–2008), when private investors sold the dollar hand over fist, worried that it was a poor store of international value.

Another common argument is that the US financial services industry has an interest in currency strength. The claim echoes complaints that London pushed the UK back onto the gold standard at its prewar parity in 1925, thus deepening a British economic slump. But an essential feature of dollar centrality is that banking systems outside the US play a larger role in global dollar intermediation than the US banking system. For example, according to the BIS, cross-border claims of the US banking system denominated in dollars amounted to 2.8 trillion at the end of Q3 2024. But cross-border dollar claims of the Eurozone banking system approached $4 trillion and were roughly $3.1 trillion in Japan, $1.75 trillion in the UK, and about $900 billion in Switzerland. And as noted above, the dollar has remained central in the international monetary system through periods of both strength and weakness. Dollar-centric financialization around the world has continued to expand dramatically since the end of the Bretton Woods system in 1971, furthered by banks in the US, Europe, and Japan, even as the dollar itself has waxed and waned in value. A world of fiat currencies with a single dominant incumbent that serves as a cross-border vehicle for all the world’s banks is very different from the gold standard era, when the links between national banking systems and their currency’s perceived credibility were much tighter.

Indeed, it is the activity of private global entities rather than the denomination of public reserve assets that is the defining feature of dollar dominance. And that has persisted through periods of weakness and strength. Its role as the leading denomination for both cross-border invoicing and cross-border debt is why the dollar persists as the central currency in the system. For all his reservations about excessive dollar strength, Trump himself has made it clear that he wants the dollar to remain central, threatening 100 percent tariffs against any country that “leaves” it. And this is the bipartisan view in much of official Washington. The architecture of American sanctions, export controls, and extraterritoriality depends on the threat of exclusion from dollar-based financial networks levied not just against primary targets but even those who might transact with them. As technological prowess becomes a critical arena of great power rivalry, the ability to threaten exclusion against entities (whether at home or abroad) believed to be furthering a competitor’s advantage has become an ever bigger part of Washington’s geopolitical toolkit.

For all of the complaints about the dollar’s centrality being an exorbitant burden, the evidence of it being a macroeconomic problem is historically patchy, and there is little doubt that it is treated in Washington as an extremely valuable geopolitical tool. This might be just an academic aside, were it not for the fact that the joint behavior of the dollar and of US bond yields in recent months has suggested that the exorbitance of the burden might in fact be easing—which might be welcome if it were, in fact, more a burden than a privilege.

A world in which the dollar is falling might be appealing to the administration but a world in which the dollar is falling and long yields are rising is decidedly not. As noted above, this is a situation that has spurred not just lots of recent market commentary but also the attention of the Federal Reserve, as noted by Fed Governor Adrianna Kugler. In her words, “the historical relationships and the observed moves in the VIX and interest rates of AFEs would have been associated with a decrease in long-term yields for US Treasury securities and an appreciation of the dollar. As the global economic landscape shifts, it is crucial to examine how possible changes in the role of US financial assets as a safe haven might affect financial stability both domestically and internationally.”

Macroeconomics and multipolarity

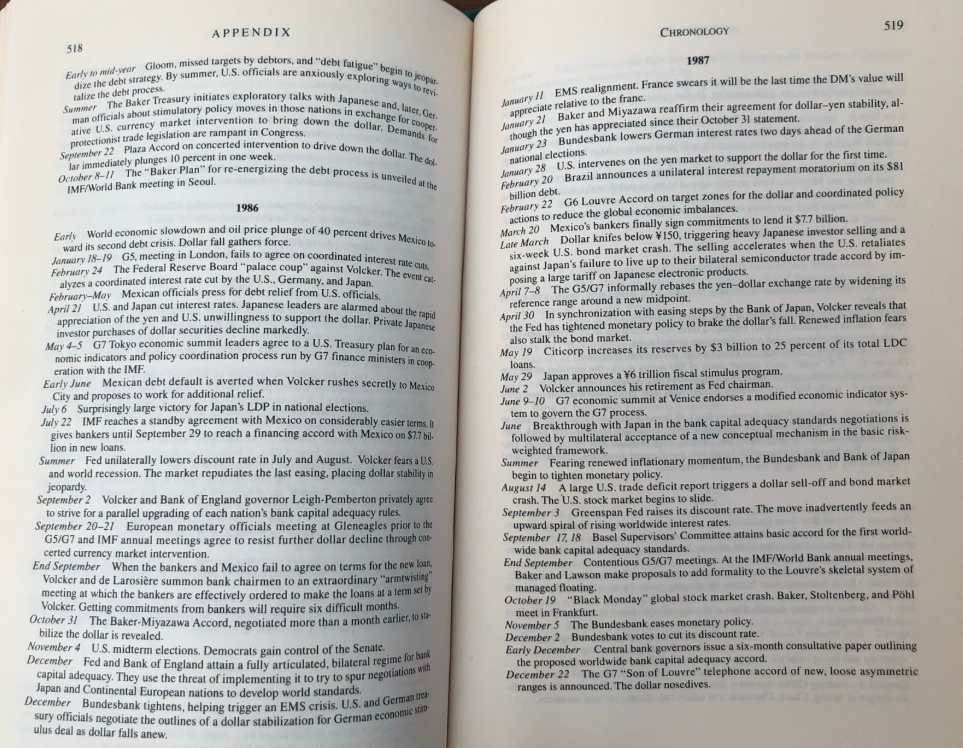

It is important to note that the historical relationship between the dollar and US rates that Governor Kugler alludes to only dates to the late 1990s and the aftermath of the Asian financial crisis. For more than two decades after that, the world was marked by relatively more austere policymaking in East Asia and the Eurozone, disinflationary impulses from trade globalization, and the dominant shocks stemming from an insufficiency of demand rather than of supply. However, in earlier periods, including the 1970s and the period between the Plaza Accord in 1985 and Robert Rubin taking over as Treasury Secretary in 1995, neither the dollar nor US Treasuries were treated as an automatic safe haven. Steven Solomon’s magisterial book, The Confidence Game, chronicles this phenomenon in detail—which in turn may help contextualize James Carville’s famous comment about wishing to be reincarnated as the bond market. Just to give an example of both the scope of the book and the history of how US currency and bond markets traded in that period, I have excerptedhere is a screenshot of two pages of the chronology below.1From Solomon, Steven. 1995. (<)em(>)The Confidence Game(<)/em(>). (<)/p(>) (<)p class='wp-block-paragraph'(>)1986 (<)br(>)(<)br(>)(<)em(>)Early(<)/em(>) World economic slowdown and oil price plunge of 40 percent drives Mexico toward its second debt crisis. Dollar fall gathers force.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)January 18–19(<)/em(>) G5, meeting in London, fails to agree on coordinated interest rate cuts.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)February 24(<)/em(>) The Federal Reserve Board “palace coup” against Volcker. The event catalyzes a coordinated interest rate cut by the US, Germany, and Japan.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)February–May(<)/em(>) Mexican officials press for debt relief from US officials.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)April 21(<)/em(>) US and Japan cut interest rates. Japanese leaders are alarmed about the rapid appreciation of the yen and US unwillingness to support the dollar. Private Japanese investor purchases of dollar securities decline markedly.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)May 4–5(<)/em(>) G7 Tokyo economic summit leaders agree to a US Treasury plan for an economic indicators and policy coordination process run by G7 finance ministers in cooperation with the IMF.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)Early June(<)/em(>) Mexican debt default is averted when Volcker rushes secretly to Mexico City and proposes to work for additional relief.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)July 6(<)/em(>) Surprisingly large victory for Japan’s LDP in national elections.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)July 22(<)/em(>) IMF reaches a standby agreement with Mexico on considerably easier terms. It gives bankers until September 29 to reach a financing accord with Mexico on $7.7 billion in new loans.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)Summer(<)/em(>) Fed unilaterally lowers discount rate in July and August. Volcker fears a US and world recession. The market repudiates the last easing, placing dollar stability in jeopardy.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)September 2(<)/em(>) Volcker and Bank of England governor Leigh-Pemberton privately agree to strive for a parallel upgrading of each nation’s bank capital adequacy rules.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)September 20–21(<)/em(>) European monetary officials meeting at Gleneagles prior to the G5/G7 and IMF annual meetings agree to resist further dollar decline through concerted currency market intervention.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)End September(<)/em(>) When the bankers and Mexico fail to agree on terms for the new loan, Volcker and de Larosiere summon bank chairmen to an extraordinary “armtwisting” meeting at which the bankers are effectively ordered to make the loans at a term set by Volcker. Getting commitments from bankers will require six difficult months.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)October 31(<)/em(>) The Baker-Miyazawa Accord, negotiated more than a month earlier, to stabilize the dollar is revealed.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)November 4(<)/em(>) US midterm elections. Democrats gain control of the Senate.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)December(<)/em(>) Fed and Bank of England attain a fully articulated, bilateral regime for bank capital adequacy. They use the threat of implementing it to try to spur negotiations with Japan and Continental European nations to develop world standards.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)December(<)/em(>) Bundesbank tightens, helping trigger an EMScrisis. US and German treasury officials negotiate the outlines of a dollar stabilization for German economic stimulus deal as dollar falls (<)/p(>) (<)p class='wp-block-paragraph'(>)1987(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)January 11 (<)/em(>) EMS realignment. France swears it will be the last time the DM’s value will appreciate relative to the franc.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)January 21(<)/em(>) Baker and Miyazawa reaffirm their agreement for dollar-yen stability, although the yen has appreciated since their October 31 statement.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)January 23(<)/em(>) Bundesbank lowers German interest rates two days ahead of the German national elections.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)January 28(<)/em(>) February 20 US intervenes on the yen market to support the dollar for the first time. Brazil announces a unilateral interest repayment moratorium on its $81billion debt.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)February 22(<)/em(>) G6 Louvre Accord on target zones for the dollar and coordinated policy actions to reduce the global economic imbalances.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)March 20(<)/em(>) Mexico’s bankers finally sign commitments to lend it $7.7 billion.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)Late March(<)/em(>) Dollar knifes below ¥150, triggering heavy Japanese investor selling and a six-week US bond market crash. The selling accelerates when the US retaliates against Japan’s failure to live up to their bilateral semiconductor trade accord by imposing a large tariff on Japanese electronic products.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)April 7–8(<)/em(>) The G5/G7 informally rebases the yen-dollar exchange rate by widening its reference range around a new midpoint.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)April 30(<)/em(>) In synchronization with easing steps by the Bank of Japan, Volcker reveals that the Fed has tightened monetary policy to brake the dollar’s fall. Renewed inflation fears also stalk the bond market.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)May 19(<)/em(>) Citicorp increases its reserves by $3 billion to 25 percent of its total LDC loans.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)May 29(<)/em(>) Japan approves a ¥6 trillion fiscal stimulus program.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)June 2(<)/em(>) Volcker announces his retirement as Fed chairman.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)June 9–10(<)/em(>) G7 economic summit at Venice endorses a modified economic indicator system to govern the G7 process.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)June(<)/em(>) Breakthrough with Japan in the bank capital adequacy standards negotiations is followed by multilateral acceptance of a new conceptual mechanism in the basic risk-weighted framework.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)Summer(<)/em(>) Fearing renewed inflationary momentum, the Bundesbank and Bank of Japan(<)/p(>) (<)p class='wp-block-paragraph'(>)begin to tighten monetary policy.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)August 14(<)/em(>) A large US trade deficit report triggers a dollar sell-off and bond market crash. The US stock market begins to slide.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)September 3(<)/em(>) Greenspan Fed raises its discount rate. The move inadvertently feeds an upward spiral of rising worldwide interest rates.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)September 17, 18(<)/em(>) Basel Supervisors’ Committee attains basic accord for the first worldwide bank capital adequacy standards.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)End September(<)/em(>) Contentious G5/G7 meetings. At the IMF/World Bank annual meetings. Baker and Lawson make proposals to add formality to the Louvre’s skeletal system of managed floating.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)October 19(<)/em(>) “Black Monday” global stock market crash. Baker, Stoltenberg, and Pohl meet in Frankfurt.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)November 5(<)/em(>) The Bundesbank eases monetary policy.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)December 2(<)/em(>) Bundesbank votes to cut its discount rate.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)Early December(<)/em(>) Central bank governors issue a six-month consultative paper outlining the proposed worldwide bank capital adequacy accord.(<)/p(>) (<)p class='wp-block-paragraph'(>)(<)em(>)December 22(<)/em(>) The G7 “Son of Louvre” telephone accord of new, loose asymmetric ranges is announced. The dollar nosedives.

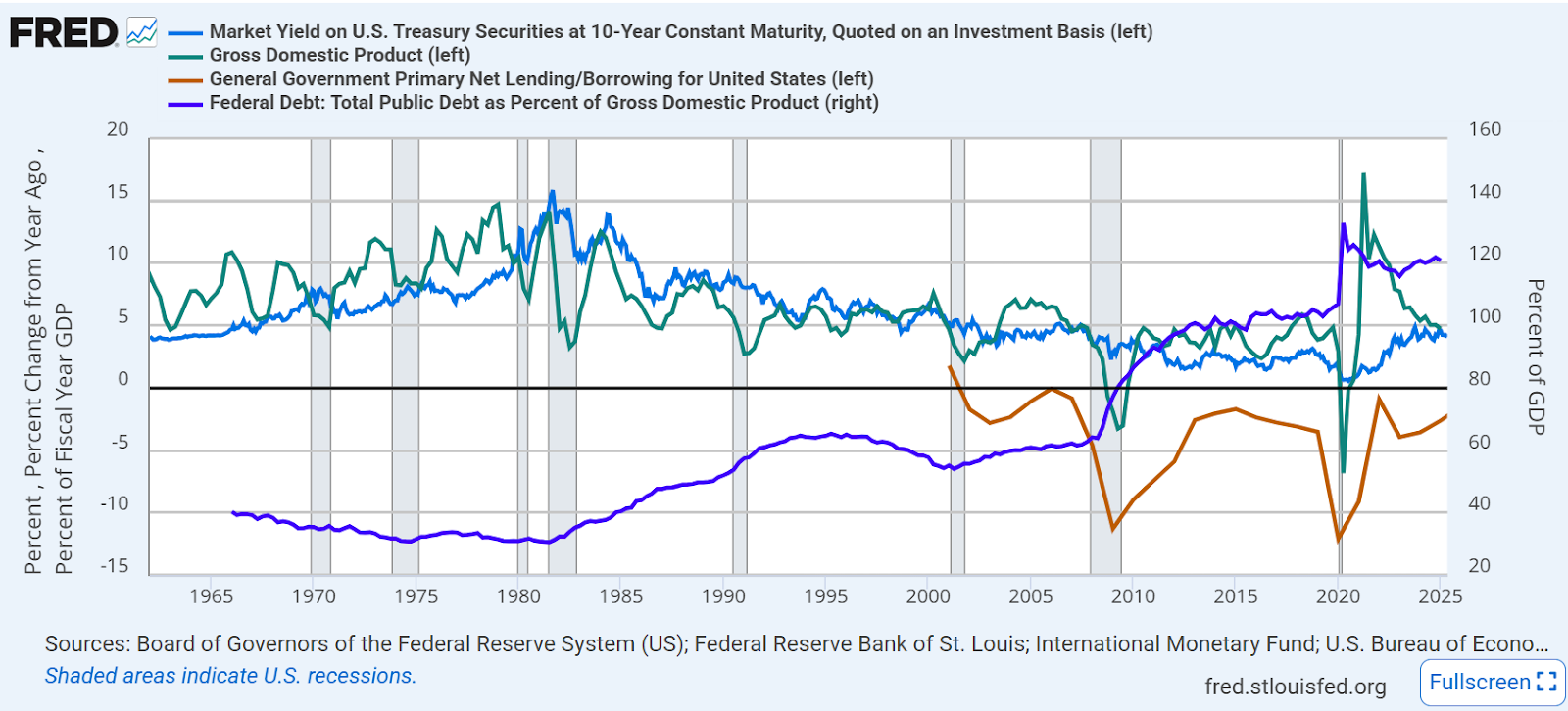

The world of disinflationary insufficient demand that followed the Asian financial crisis might also have had certain benefits for the US, particularly in the relationship between US nominal growth and US interest rates—two key factors that determine a country’s debt trajectory, with the third being the so-called primary balance or the government deficit/surplus excluding interest payments. The basic arithmetic is that a rate of nominal growth above the rate of interest on government debt should lower debt/GDP unless the primary fiscal deficit is large. Conversely, running a large primary deficit will lead to faster increases in debt/GDP unless the rate of interest is below the rate of nominal growth. The below chart looks at these three variables over the last five decades and shows why an administration that wants enormous tax cuts is so interested in getting lower long-term US interest rates and/or higher government revenues from foreign sources, whether through expedients like the “century bond,” or foreign governments “writing the US a check.”

Even so, the administration’s policies are leading to changes outside the US that are putting some other contenders in a better position to mount a partial challenge to the dollar. If the “Century Bond” scheme was an attempt by the US to monetize primacy by pricing the export of its security umbrella, it seems to be impelling a movement toward import substitution because of concerns about the predictability of American defense guarantees. (Europe in particular has declared its intent to boost defense spending in reaction to US signals.)

The first market reaction to Europe embracing a more expansionary fiscal policy was to push both German bund yields and the euro higher (bund yields have come down since, but the euro continues to strengthen). The tandem of higher yields and a stronger currency is typically taken to be a sign of market confidence in a government’s policies. A domestic fiscal impulse is being treated as a sign that Europe has less need to rely on exports, and the expansion is not seen as heightening the risk of future repudiation through inflation or default (fears of either would tend to see the currency weaken). Meanwhile, China does seem to be reacting to the tariff threat by taking the need to boost domestic consumption through central government fiscal expansion somewhat more seriously than in the past. In this regard at least, Bessent already seems to be getting some of what he wanted—a shift in the balance of savings and consumption behavior outside the US. And if that persists and expands, that would be a profoundly healthy thing for the global economy by giving it more poles of final demand.

What would a multipolar global monetary system look like, with multiple poles of final demand and multiple currencies holding the functions of the reserve? Significantly, such a world would allow for greater synchronicity between real and financial cycles. As I have written elsewhere, the dollar’s central role in the international monetary system means it “drives the global financial cycle, and that is determined to a substantial degree by the Fed’s response to key macroeconomic aggregates within a relatively closed economy … A unipolar force driving the global financial cycle alongside multipolar forces driving local real cycles is a bad idea for financial stability … [suggesting] an argument for a multipolar global monetary system that avoids exactly such a divergence between real and financial cycles across hubs and spokes.”

But talk of dollar “replacement” is both premature and not necessary for a multipolar global economy. What is more likely is an acceleration of creeping regional displacement with the primary beneficiary, for now, being the euro. That is because it is the only rival that has most of the attributes of the dollar—an open capital account, a large stock of freely tradeable securities denominated in that currency, a massive internationally active banking system, and a central bank willing to act as a lender of last resort. What it has lacked thus far is a deep well of unequivocally safe assets denominated in that currency. The combination of fiscal expansion in Germany and beyond, some joint issuance, and a market sense that geopolitical considerations make the ECB more likely to serve as a backstop for national governments could all help the euro’s case. And European policymakers, including Christine Lagarde, seem to understand that the euro’s place at the table must be “earned.”

But replacing the dollar’s role in invoicing trade flows is easier than replacing its leading role in cross-border lending, particularly in the form of tradeable securities. This is the big issue with a Chinese challenge. As the currency of a country that is the world’s largest exporter and accounts for roughly a third of global manufacturing value-added, the renminbi has an implicit “real anchor” in terms of its valuation. However, the road to full capital account convertibility for the renminbi may be far away, and its capital markets are not fit for purpose when it comes to large-scale transactions by non-Chinese participants. Even so, it could create a more bank-lending-based renminbi zone with some capital market offshoots that bring in more of its closest trading partners, and provide them with electronic transactions pathways opaque to the US. The latter is not an economic challenge but would certainly be seen in Washington as a geopolitical one. However, the “BRICS currency” that has so aroused Trump’s ire is unlikely ever to get there: even before considering the significant divides between BRICS members that preclude deeper cooperation, a currency without a full-service central bank is a non-starter.

For more than a decade now, policywatchers have been warning that an increasingly expansive use of sanctions policy could increase the pressure on the dollar’s central role in the international monetary system. But that pressure was also contained by the reluctance of other contenders (above all, the euro area) to take the fiscal, monetary, and institutional steps that might allow their currencies to assume elements of that centrality. It won’t happen in a hurry, but the Trump Administration’s attempts to monetize and thereby perpetuate American primacy could bring forth the macroeconomic responses that make other currencies emerge as plausible alternatives to the dollar.

Further Reading

Money as Empire?

On Perry Mehrling’s “Money and Empire: Charles P. Kindleberger and the Dollar System”

Money makes the world go round, or as Karl Marx put it, Geldgespräche, Quatsch-Spaziergänge. How does this work at the global or international level? Perry...

America First?

Escalation and reverberations in the trade war

The reelection of Donald Trump to the presidency has sent shockwaves around the world. And just hours after results came in, the ruling three-party German...

Regime Change?

The evolution and weaponization of the world dollar

The centerpiece of shock and awe of the West’s economic response to Russia’s invasion and bombardment of Ukraine was the freezing of Russia’s central bank...