October 29, 2025

Analysis

Policy-Constrained Growth

Government spending and economic recovery in Brazil during Lula's third term

Despite headwinds from higher interest rates in the US and at home, the Brazilian economy is nevertheless emerging from a period of prolonged stagnation. After growing an average of 0.2 percent a year between 2015 and 2022, national growth averaged 3.3 percent annually during 2023–2024, the first two years of President Lula’s third term. Though quite modest in comparison to the massive social needs of a developing country, this is still better than expected.1In order for developing countries to catch-up to the level of GDP per capita of the advanced economies, not only its GDP but also its GDP per capita must grow sufficiently faster than they do for very long periods of time. Therefore the many government statements that it plans to grow at the same rate of world economy is clearly unsatisfactory. Part of Brazil’s recent positive performance has been due to growing exports, to be sure. But the bulk of Brazil’s current economic growth stems from a cause the government itself has been reluctant to recognize: expansionary fiscal policy, which has generated sufficient demand to counteract these forces of contraction.

There are reasons to celebrate this growth performance. First, it marks a great improvement on Brazil’s recent bleak past. Between 2015 and 2022, fiscal austerity and neoliberal reforms reduced the level of domestic demand and produced stagnant GDP growth: by the end of 2022, the internal market was smaller than it had been in 2014. Since 2023, it has begun to increase again, leading to higher business investment, which grew faster than GDP in 2024. Finally, because of rapid changes in demographic dynamics, the growth rate of GDP per capita in Lula’s third term (2.9 percent a year) is nearly the same as the one obtained from 2003 to 2010, in the previous—and relatively prosperous—Lula era (3.0 percent a year).2The growth rate of population has lately been decreased sharply, from an average of 1.0 percent during the first two presidential mandates of Lula (2003–2010) to 0.4 percent now.

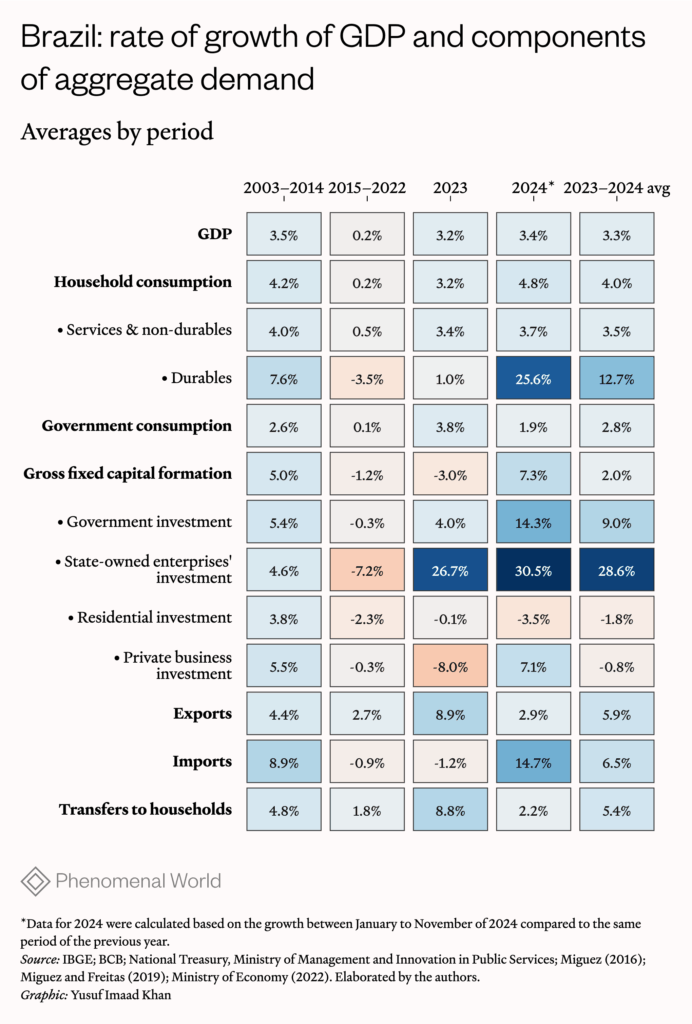

The table below summarizes the main components of aggregate demand in Brazil since 2003.

We shall argue that apart from exports (where growth accelerated alongside the process of ‘re-primarization’), the bulk of Brazil’s recent positive performance has been due to its expansionary fiscal policy. The growth of government spending and business investment, however, was not entirely by design. The explicitly stated economic policy priorities for Lula’s third term are monetary policy guided by an inflation target, and the priority of stabilizing the ratio of public debt to GDP. But a peculiar conjunction of events has fortuitously pushed fiscal policy toward expansion. Detailed below, the Brazilian economy’s transition from Bolsonaro’s program briefly allowed the government to raise the level of aggregate demand, despite both Treasury guidance toward slowing the growth of public debt and interest rates dramatically higher than at any time over the last decade.3Note that such ratio in reality creates no actual problem as it is paid in local currency at interest rates largely under control of the Brazilian central bank.

Nevertheless, Finance Minister Fernando Haddad has been arguing that Brazilian growth can continue without further fiscal expansion, led by household consumption and private investment—as if these factors were not highly influenced by fiscal policy. The central bank, too, blames expansionary fiscal policy for a presumed overheating of the Brazilian economy in hiking the country’s basic interest rate. Despite massive underemployment and informality, the low unemployment rate and growth of real wages are understood as inflationary problems to be solved by constraining demand.

It appears that the official federal program is guided by the theory that potential output grows independently of aggregate demand. Official justifications for fiscal-monetary tightening assume that growth will continue—at a rate as low as 2.5 percent—if demand is constrained by policy. It is government spending and a stronger currency, however, that have propelled Brazilian growth. Overall, the impact of fiscal expansion on demand was stronger than the contractionary effects of a tighter monetary policy, whose negative (but limited) effects were mainly felt in residential investment. The fallout of higher interest rates was probably more than offset by changes in the exchange rate, which contributed to higher real wages and increased consumption—the latter also driven by the policy of minimum wage increases and lower unemployment rates.

Beyond demand: external conditions and monetary policy

Since 2022, rising interest rates set by the US Federal Reserve have made it more difficult for many emerging economies to sustain expansionary policies amid balance of payments constraints.4Serrano, F., Summa, R., & Aidar, G. (2021). Exogenous interest rate and exchange rate dynamics under elastic expectations. (<)em(>)Investigación económica(<)/em(>), (<)em(>)80(<)/em(>)(318), 3-31. Brazil, however, has continued to face quite favorable external financial conditions during this recent period. Since the mid‐2000s, despite persistent current account deficits, Brazil has accumulated massive foreign exchange reserves and substantial capital inflows. The ratio of the country’s short-term external debt to its foreign reserves remains below 30 percent. Over the past decade, total external debt has averaged around 71 percent of reserve assets, meaning that the country’s overall external position has remained relatively comfortable.

A key aspect of improvement in the Brazilian external accounts has been the process of “de-dollarization” of its external liabilities. This means that now a large share of Brazilian external liabilities (such as public bonds and shares held by non-residents) are denominated in Brazil´s own currency, making creditors bear the exchange rate risk and making the economy less vulnerable to large exchange-rate movements. These facts allowed Brazil to finance sizeable current account deficits in 2023-24 without creating vulnerabilities.

The structure of Brazil’s large current account deficits reflects net profit, dividend and interest outflows in excess of the country’s trade surplus. In balance of payments accounting, an excess of payments out over receipts is financed by capital and financial inflows, which usually require higher interest rate differentials to attract.5For a detailed explanation, see: Summa, Ricardo; Haluska, Guilherme and Serrano, Franklin. Actual government spending and the resumption of growth in Brazil: 2023-24. Working paper (2025).While the nominal exchange rate appreciated around 10 percent in 2023, linked to an improvement in the current account and a higher interest rate differential, both reversed in 2024 amid growing imports due to stronger economic growth, a recovery in business investment, and a smaller interest rate differential. The nominal exchange rate thus depreciated 10 percent between January and September 2024. By the end of 2024, the nominal exchange rate had sharply depreciated by an additional 13 percent.6Three main factors account for that: 1) the fact that firms usually remit profits and dividends abroad in December; 2) a “flight to the dollar” driven by uncertainties around the US elections; the initial lack of intervention in the foreign exchange rate market by the Brazilian central bank—which, later, acted to reverse this trend. Again, see Summa, Haluska and Serrano (2025). This has led the central bank to sell dollars and raise the base interest rate significantly, which again increased the differential and helped the currency appreciate.

Central bank management of Brazil’s exchange rate is relevant for understanding the country’s inflation dynamics because Brazil is a price taker in many international markets. Its nominal costs of production largely depend on the price of tradable goods in dollars converted into local prices by the exchange rate. Both the evolution of international prices and nominal exchange rate dynamics are, therefore, major sources of cost-push inflation for the country.7Other cost-side factors are government-regulated prices and labor costs that increase as a result from nominal wage bargaining. This accounts for monetary policy being so tight in 2023–24.

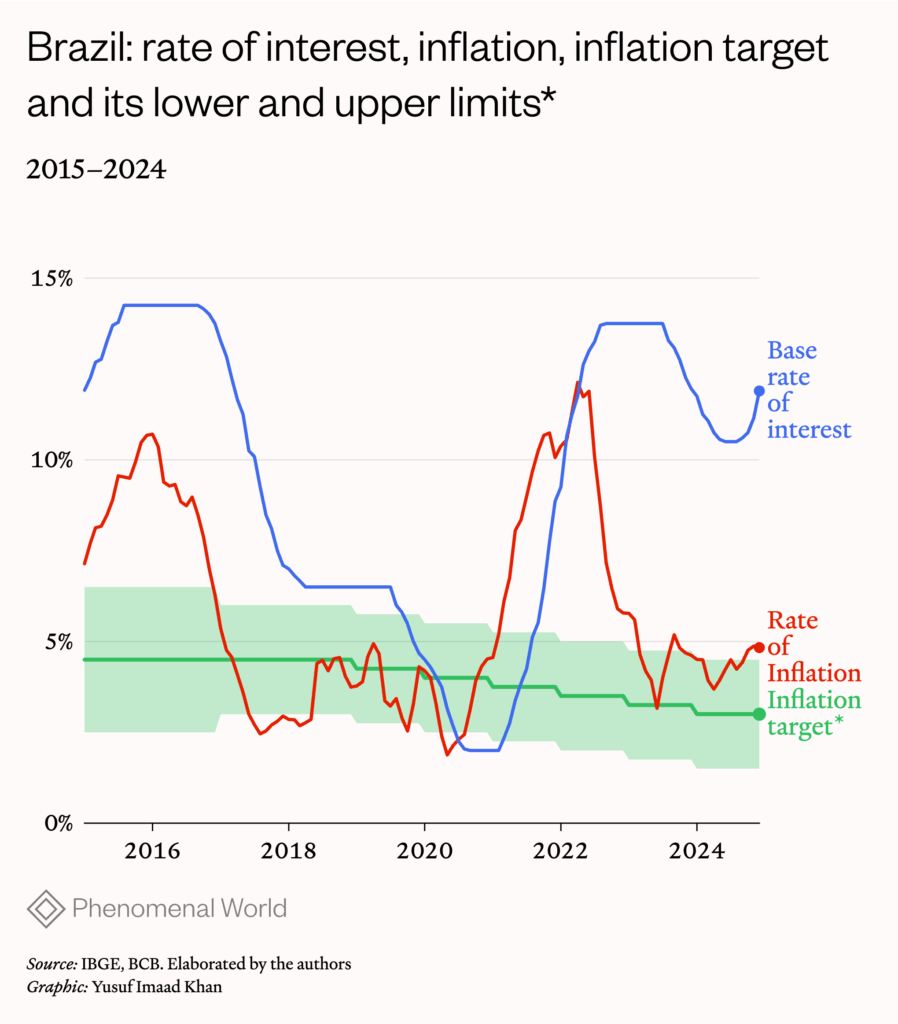

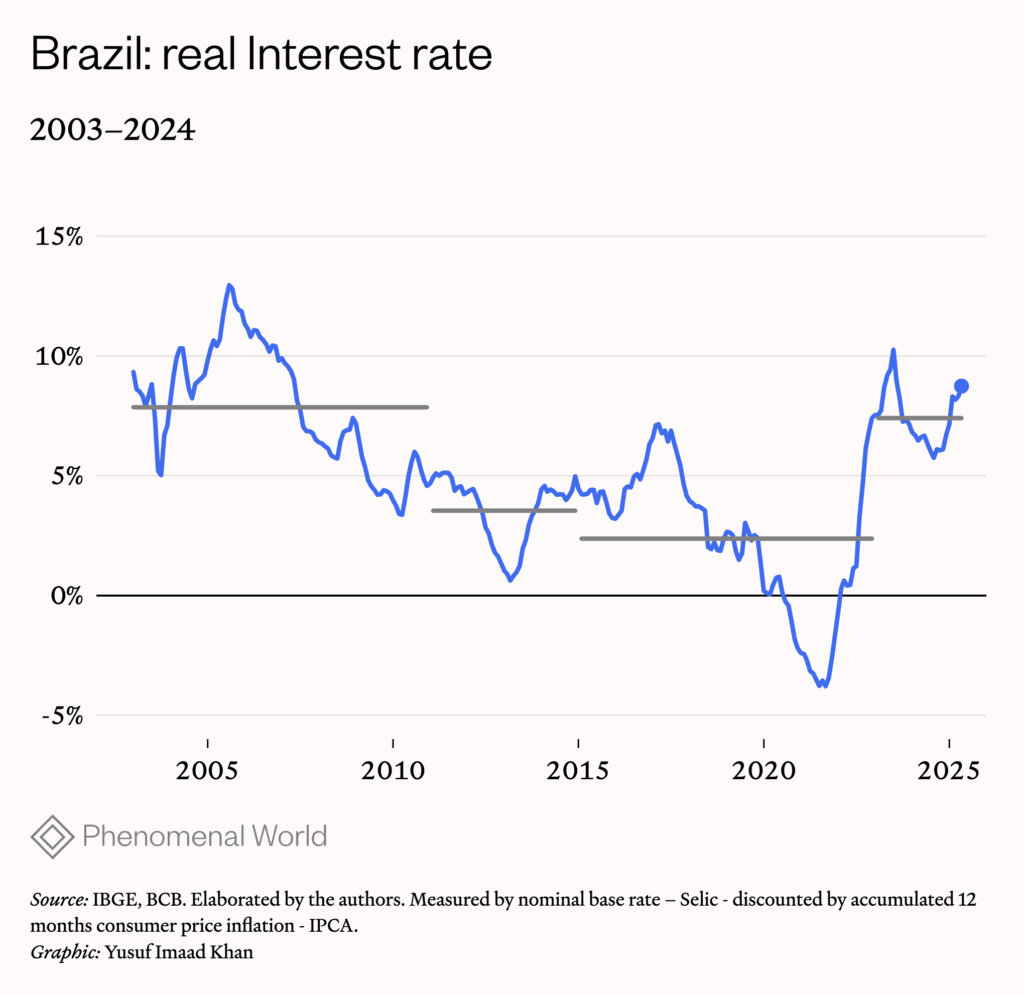

In fact, monetary policy in the recent period has been significantly tighter than in 2015–2022, when the economy was stagnating. In 2021–2022, simultaneous increases in commodity prices in US dollars and sharp exchange rate depreciation pushed inflation up to 12 percent. The central bank reacted by increasing the base interest rate, which reached 13.75 percent by the end of 2022. Figure 1 presents the rate of inflation, the inflation target (and its upper and lower limits), and the nominal policy interest rate in Brazil from January 2015 to January 2025. Figure 2 shows the behavior of the ex-post real interest rate, adjusting the nominal rate for inflation, from 2003 to 2024. It shows the real interest rate today to be much higher than the average for the previous periods of 2011–2014 and 2015–2022.8We follow the periodicity as proposed in Serrano and Summa (2015) and Haluska et al (2025). The period 2003–2010 mark Lula’s presidential terms, where growth rates were higher due mainly to expansionary fiscal policy, despite a higher average real interest rate. The period 2011–2014 mark the deceleration of growth in Dilma’s first mandate, as an attempt to control fiscal expansion and compensate it by higher private spending, which supposedly would come from a lower interest rate and a depreciated real exchange rate. The third period marks fiscal austerity policies that started in the second term of Dilma Roussef (cut short by the 2016 impeachment) and continued in the Temer and Bolsonaro administrations, leading to high unemployment and falling real wages and inflation. The ensuing lower real interest rates were associated with GDP stagnation. Finally, the period 2023–24 is the one under analysis in this article.

During 2023, global commodity prices fell and the domestic currency appreciated, weakening external inflationary pressures. The central bank then started to reduce the base interest rate, to 10.5 percent in mid-2024. However, the depreciation of the nominal exchange rate in 2024 brought prices higher, particularly of food and tradable goods—which under the central bank’s inflation target meant an increase in interest rates to their current highs.9For more details on the causes of the exchange rate devaluation in Brazil in 2024, see: Marins, N., Summa, R. & Consul, D. (2025) The behavior of the nominal exchange rate between the Brazilian Real and the dollar in 2024. (<)a href='https://nakedkeynesianism.blogspot.com/2025/03/the-behavior-of-nominal-exchange-rate.html'(>)Naked Keynesianism blogpost(<)/a(>).

The Brazilian inflation that peaked at 12 percent annually in early 2022 was driven by cost-push factors particularly among tradeables. Because workers were unable to adjust their nominal wages to rising prices—inflation outpaced wage growth—there was a decline in real wages. Likewise, the decline in inflation the following year reflected cost-side elements, rather than changes to aggregate demand: inflation continued downward despite falling unemployment, an increase in the minimum wage, and the return of GDP growth. In 2024, inflation rose slightly to 4.8 percent, almost the same as 2023, reflecting a depreciating currency and a modest increase in international prices.

A crucial factor in the Central Bank’s interest rate setting and the resulting level of the real interest rate is the government’s inflation target. In 2018, monetary policy targeted 4.5 percent annual growth in prices with an upper limit of 6 percent. It has since been progressively reduced. By 2024, the target was 3 percent with an upper limit of 4.5 percent. Even though annual inflation in 2024 was almost similar to the number registered in 2023, the target was not met and so interest rates were increased.

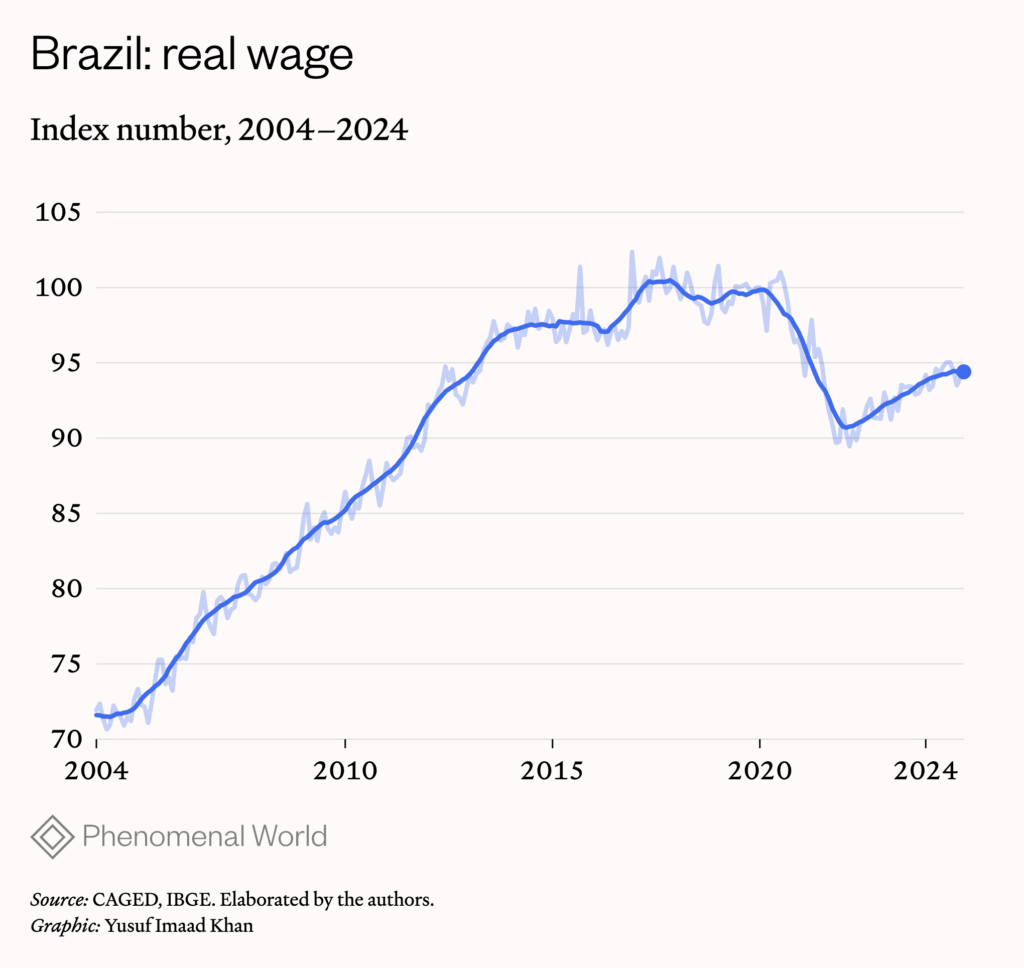

In 2023–24, average real wages from formal jobs grew around 1.7 percent each year. Nevertheless, real wage levels remained 3 percent below their level in 2014, right before the economy started to stagnate. The gradual reduction in inflation targets was associated with flatlining and then decreasing real wages. At the same time, as a result of these changes, real interest rates have gone up. Why, in that case, has Brazilian growth accelerated under Lula’s third term?

Aggregate demand and its components

Exports are only a small part of the answer. Despite a more appreciated real exchange rate in 2023–4, exports grew at 5.9 percent annually, faster than the growth rates of either world GDP (3.3 percent) or global goods and services trade (1.9 percent). The growth of exports was particularly impressive in 2023, as Brazil benefited from both a very good harvest and, as an effect of the war in Ukraine, increased oil exports.

Imports grew on average 6.5 percent over the two years, mostly because of the rapid rise of imports in 2024, following the delayed but strong recovery of business investment.

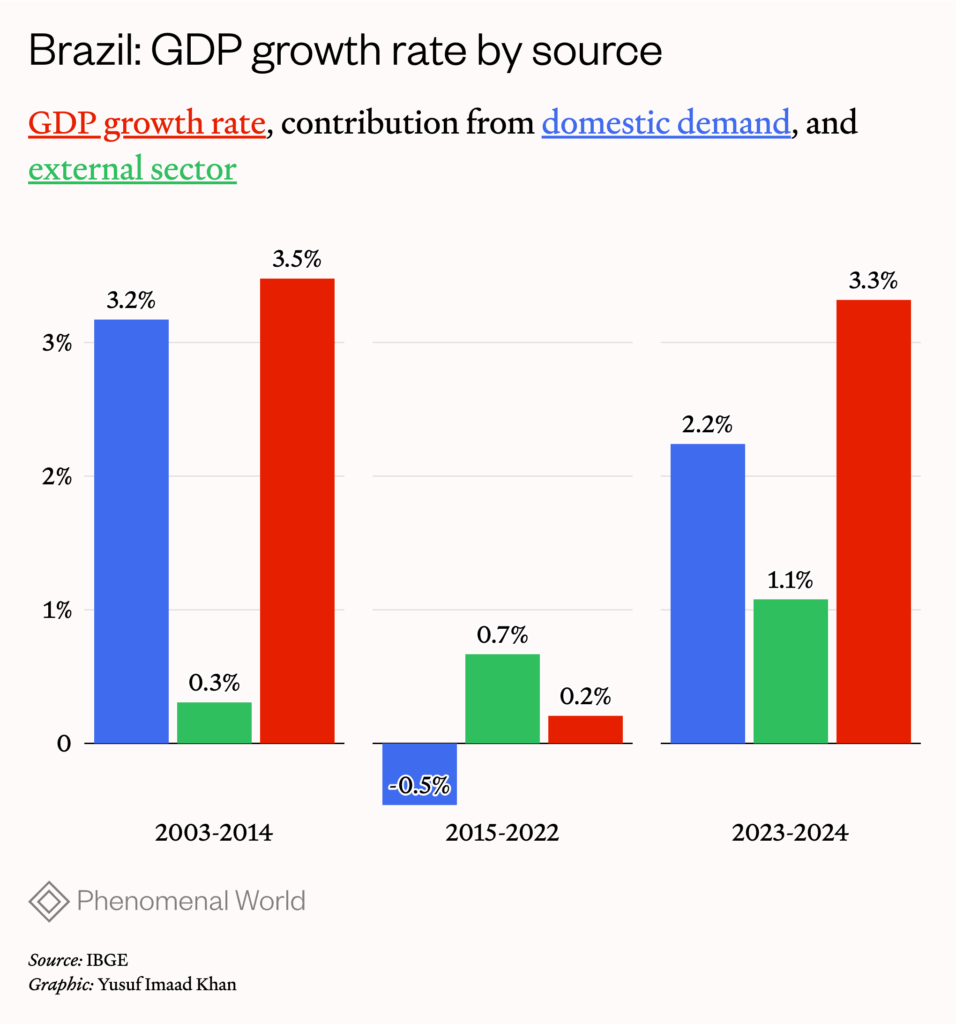

Brazil, however, is a continental country and has a small share of exports—about 18 percent—of GDP in 2023–24. The external sector is not capable of inducing high rates of growth of aggregate demand and GDP in the absence of increases in domestic components of demand.10Freitas, F. N., & Dweck, E. (2013). The pattern of economic growth of the Brazilian economy 1970–2005: a demand-led growth perspective. In (<)em(>)Sraffa and the Reconstruction of Economic Theory: Volume Two: Aggregate Demand, Policy Analysis and Growth(<)/em(>) (pp. 158-191). London: Palgrave Macmillan UK; Haluska, G. (2023). A economia brasileira no século XXI: uma análise a partir do modelo do Supermultiplicador Sraffiano. (<)em(>)Economia e Sociedade(<)/em(>), (<)em(>)32(<)/em(>)(2), 297-332; Campana, J. M., Vaz, J. E., Hein, E., & Jungmann, B. (2024). Demand and growth regimes of the BRICs countries–the national income and financial accounting decomposition approach and an autonomous demand-led growth perspective. (<)em(>)European Journal of Economics and Economic Policies(<)/em(>), (<)em(>)21(<)/em(>)(1), 17-41. If we look at the actual contributions to growth of the external sector and the domestic demand, we can see that the external sector contributed, on average, to 1.1 percentage point (pp) to the growth of GDP per year in 2023–2024, while the domestic sector contributed to 2.2 pp. Fully two thirds of recent GDP growth can be attributed to the expansion of domestic demand.

Fiscal Policy

We now turn to how the economic policies adopted produced this expansion of the domestic market. In 2023, Brazil abandoned the cap on federal government spending imposed seven years earlier by the right-wing government of Michel Temer. That year, Congress authorized the government to spend more than Temer’s cap. For 2024, the government changed the fiscal rule to target a ceiling on government spending growth of between 0.6 percent and 2.5 percent, and a ratio between the primary surplus (the difference between primary spending and receipts) and GDP.11The cap on federal spending approved in the Temer’s government was included in the Brazilian Constitution and imposed a zero growth of real federal government expenditures. Nevertheless, in practice, although federal spending growth was considerably reduced, it did not actually fall to zero, as we showed in Haluska et al (2025). The new fiscal rule established in 2023 is statutory.

Moving from institutional arrangements and fiscal rules to practice, the federal government under Lula has resumed the policy of increasing real minimum wage, after remaining frozen during Temer’s and Bolsonaro’s governments.12During Temer administration, the rule for adjusting the minimum wage still allowed for real increases. By then, the minimum wage should be adjusted according to past inflation and the growth of GDP of two years before; and in cases when GDP have fallen, the minimum wage would be adjusted only by past inflation. However, since GDP fell both in 2015 and in 2016, during the two years of Temer administration (2017–2018), the minimum wage was adjusted only for inflation, without real gains. It was only under Bolsonaro’s administration when the rule for adjusting the minimum wage changed, stablishing only adjustments according to inflation, without real increases. This is important to fiscal policy because many pensions and transfers to households are indexed to the minimum wage. In 2023, the real minimum wage increased around 3 percent in real terms each year. Due to demographic changes, the number of elderly people in the country eligible to receive pensions has also been growing. Therefore, the combination of increases in the real minimum wage and in the number of retired people together resulted in a substantial increase in the amount of transfers to households.

By itself, this would not be sufficient to push fiscal policy beyond the 2.5 percent cap on growth of federal expenditures in the new fiscal rules. However, this cap was suspended (by the so-called ‘PEC da Transição’) during 2023, as a law was approved to guarantee extra federal government spending during the year of transition between the old and the new fiscal rule.

Additionally, the federal government paid an important amount of judicial debt to households just a few days before the end of 2023—the so-called precatórios—which increased the transfers to households in that year increasing household consumption mostly in 2024.13Precatórios are court-ordered government debts. Under Bolsonaro, a 2021 law (“precatórios cap”) limited how much could be paid each year, postponing the rest in order to free fiscal space for other programs. This effectively froze part of the payments and created a backlog. In 2022, the Supreme Court struck down the cap as unconstitutional. As a result, in 2023 the Lula government had to resume payments, including both the new debts and part of the postponed ones, which caused a significant increase in fiscal spending.Also in 2024, additional spending for emergencies was made due to adverse climate events (such as floods in the state of Rio Grande do Sul and wildfires in various regions of the country). It should be noticed that both precatórios and emergency-related fiscal spending were excluded from the official fiscal target.

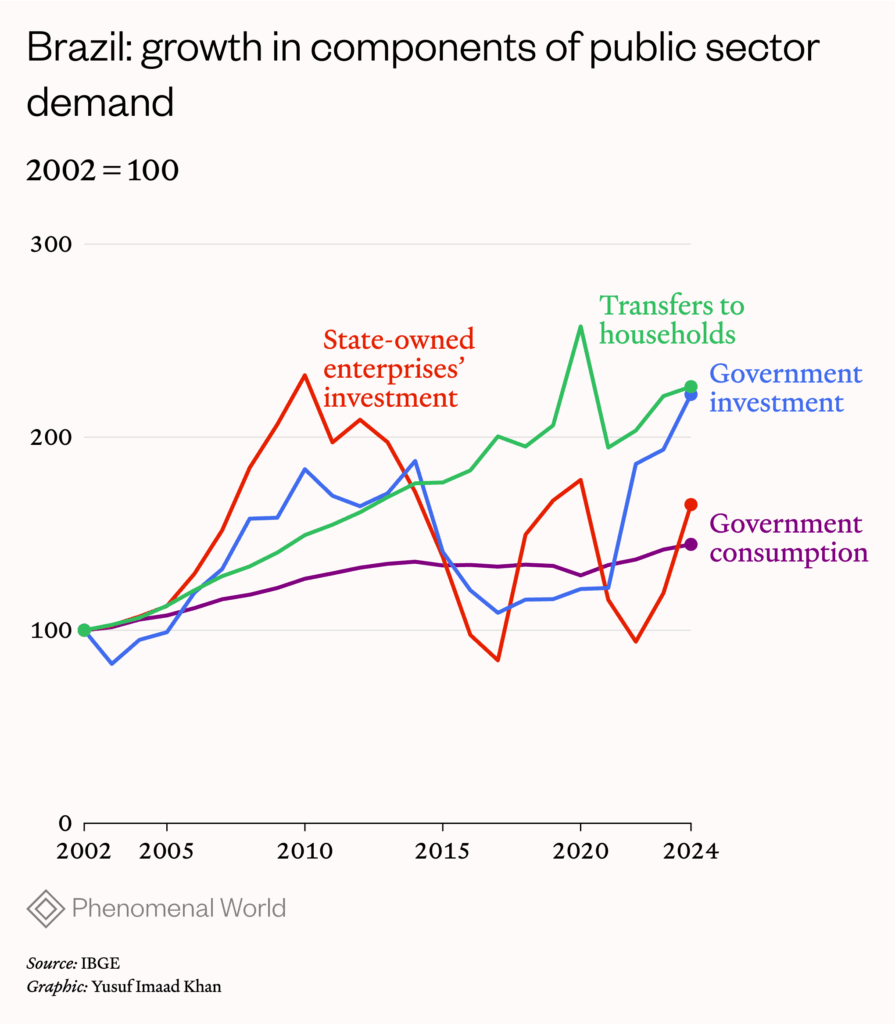

Finally, the increase in public expenditures was driven not only by the federal government, but also by the states and municipal governments, whose expenditures were boosted by increasing receipts and due to the 2024 municipal elections.14IPEA (2025) Carta de Conjuntura : n. 66, jan./mar. 2025 ‘BOX 3: O comportamento recente dos gastos dos entes subnacionais’ carta de conjuntura do IPEA – Instituto de Pesquisa Econômica Aplicada (Ipea). Additionally, there was an expansion of investments made by state-owned enterprises of 28.6 percent a year, which are not included in the fiscal targets. As a result, total government consumption grew on average 2.8 percent a year during 2023 and 2024; total public investment increased 9.0 percent a year, and transfers to households grew 5.4 percent a year. In sum, while the base real interest rate was higher in the period 2023–24 than in 2015–22, fiscal policy was much more expansionary.

Autonomous demand, induced consumption and business investment

Apart from public spending, there are three other important components of aggregate demand: household autonomous expenditures, induced consumption and induced business investment. Induced consumption represents spending out of contractual income (wages and salaries) generated by firms’ decisions to undertake production. Business investment is seen as induced because firms will typically only invest to produce output to meet their expected levels of demand. Autonomous spending represents spending independent of business production decisions, mainly by creation of consumer purchasing power out of credit or government spending.15For a theoretical discussion on the concept of autonomous demand and its relation with macroeconomic policies, see: Serrano, F., Summa, R., & Freitas, F. (2023). Autonomous demand-led growth and the supermultiplier: the theory, the model and some clarification. (<)em(>)Instituto de Economia UFRJ Working Paper(<)/em(>), (<)em(>)3(<)/em(>). By household autonomous expenditures, we mean the sum of autonomous consumption and residential investment which are sensitive to interest rates and credit conditions, and consumption out of public transfers.

As we saw in Figure 2, the real interest rate was high regarding historical averages, but it was reduced marginally from the end of 2023 and the beginning of 2024. Also, the number of formal jobs increased considerably (3.4 percent a year, on average, during 2023–2024), and the informality rate decreased from 49.8 percent to 48.5 percent.16According to data from “(<)em(>)PNAD Contínua.”(<)/em(>)Workers in the formal labor market have much better access to cheaper credit; cheaper borrowing and formalization have together increased autonomous household spending. The federal government also launched a program for credit renegotiation to reduce household indebtedness, called Desenrola Brasil. As a consequence of all these factors, the consumption of durable goods grew on average 12.7 percent in 2023–2024.

Regarding residential investment, the federal government resumed housing finance subsidies for low- and medium-income families launched in 2009 under Lula but extinguished in 2019 by Bolsonaro, the so-called “Minha Casa Minha Vida” program. This measure has not overcome higher interest rates: residential investment decreased 1.8 percent on average in 2023–2024.

Induced consumption among households increased as well. Real wages increased as a consequence of higher growth rates of GDP, lower unemployment rate, the policy of real minimum wage increase and the appreciation of the real exchange rate (which, as discussed,was a collateral effect of higher interest rate differentials). Average real wages from formal jobs grew around 1.7 percent per year, as can be seen in Figure 3. The real income of employees, which includes not only formal but also informal workers, grew even more, 4.8 percent a year, probably because not only compensation increased but also the better growth performance contributed to increasing the income of self-employed workers. Households’ induced consumption thus grew because of both the increase in real wages and the increase in employment.

Finally, we get into the discussion of the behavior of business (non-residential private) investment. After falling in 2023, in 2024 induced business investment increased much more than the GDP in 2024 (7.1 percent).

This illustrates how business investment is made by firms: to build capacity in expectation of future demand. In 2023, expectations of growth were very low, but were slowly revised with the actual growth recovery.17Other part of the fall in investment in 2023 can be due to a temporary boost in investment in 2021-2022, when several companies anticipated their purchases of new trucks, because they must be produced with stricter rules about the emissions of pollutants, with higher production costs and prices, after 2023 (IPEA, 2024, Haluska et al, 2025). Since it was becoming clearer that growth was more permanent, business investment increased more than GDP in 2024.18As expected by the flexible accelerator mechanism. For empirical evidente for Brazil, see: Braga, J. (2020). Investment rate, growth, and the accelerator effect in the supermultiplier model: the case of Brazil. (<)em(>)Review of Keynesian Economics(<)/em(>), (<)em(>)8(<)/em(>)(3), 454-466. Despite high real interest rates in the period, private business investment increased rapidly in 2024 because of the recovery of aggregate demand.

Policy-constrained demand-led growth

The hesitation of the federal government to defend the expansionary fiscal policy and higher growth rates of GDP manifested even more recently. Because of its use in indexing transfer payments, the increase in the minimum wage was capped in 2025 to the same 2.5 percent ceiling on public expenditure growth. Benefits paid by Bolsa-Familia, the social insurance program covering over 20 million households in Brazil, have also been frozen in nominal terms (a real decline) since 2022—with proposals to increase them denied failing to pass.19The last important nominal increase in the main benefit paid by Bolsa Familia was made by the right-wing government of Bolsonaro, although in 2023 an additional benefit was included in Bolsa-familia to pay an extra amount for each 0 to 6 years old children in the family.

The idea that government spending must be controlled to make space for faster growth led by the private sector, while being extremely popular among Brazilian economists of all persuasions, is not only based on flawed theoretical arguments, but has led to the slowdown of the Brazilian economy since 2011 and actual stagnation since 2015.20On slow down, see Serrano, F., & Summa, R. (2015). Aggregate demand and the slowdown of Brazilian economic growth in 2011-2014. Nova Economia, 25, 803-833. On stagnation: Haluska, G., Summa, R., & Serrano, F. (2025). The bridge to stagnation: government expenditure cap, reforms and the fall in the business investment share in Brazil (2015-2022) (No. 247/2025). Working Paper. If the current efforts to slow down the increase in Brazilian government expenditures are successful, the nation’s economic growth will unquestionably be reduced.

Further Reading

The Political Economy of Brazilian Inflation

The implicit income policy of central bank inflation targeting

Over the past two decades, Brazil has seen two great swings in its distribution of real national income. In the years between 2004 and 2014,...

Why So High?

The institutional challenges of Brazil's interest rate policy

The clashes between Lula and Campos Neto illustrate something of the complex and controversial issue of interest-rate setting in Brazil.

Lula’s Fiscal Cage

The winners and losers in Brazil’s new tax regime

Among the factors securing Luiz Inácio Lula da Silva’s victorious return to power in the 2022 Brazilian presidential elections, the most important was the promise...