Analysis

Early this year, in the Brazilian Amazon, a coalition of fourteen indigenous groups rose up against a government decree that planned to privatize the waterway between Itaituba and Santarém—two towns in the state of Pará—as well as a public project to dredge the River Tapajós. The giant commodities trader Cargill controls ports in both towns that act as key nodes of the logistics infrastructure through which soy grown in the rainforest and savanna is sent to global markets, mainly in Europe and Northern Africa. In 2022, around 13 percent of all soy exported by Cargill from Brazil was shipped from Santarém, including almost two-thirds of the beans grown in the rainforest.

The groups launched the protest by camping in front of a Cargill terminal in Santarém and demanding that the government cancel both the privatization of the river and its dredging. The communities claimed that the plans, on which they hadn’t been consulted, posed a direct threat both to their livelihoods and to the rich biodiversity of the region, risking the release of harmful mercury from the riverbed. At its height, the camp had more than a thousand people. After just over a month, the government agreed to meet their demands. The reaction from the mainstream press was one of shock and horror.

The episode brings to the fore the critical role played by multinational corporations in conflicts around the Amazon. By looking at the South American soy boom in the biome and beyond, we can begin to grasp the ways in which corporate concentration in one of the region’s main export activities has contributed to both the rise of a far-right agribusiness bloc and popular mobilizations in defense of the environment. While one of my previous columns discussed how policies oriented towards “land-sparing” helped to create the conditions for bolsonarismo, here I will discuss another crucial factor in South America’s political evolution: the power relations within supply chains.

Capital in the Amazon

Global capital’s interest in the rainforest is nothing new. In the 1920s, for instance, Henry Ford bought a massive piece of land in the biome which he named Fordlândia and hoped to transform into a plantation of rubber trees from which to source the inputs for the tyres of his mass-produced cars. Yet the relative significance of foreign investment has fluctuated over time. Critical scholars studying the region have generally claimed that it would be misleading to make it a central focus, since the Amazon’s main problems have flowed from domestic political and economic factors. “The role of international capital in producing deforestation in the Amazon has been relatively minor,” wrote Susanna Hecht and Alexander Cockburn in The Fate of the Forest in 1990. Hecht later took aim at attempts to connect deforestation to the international demand for beef. ‘‘The so-called hamburger connection,’’ she argued, ‘‘simply does not operate in the current Amazonian context.’’ (The literature on this question, from that period, was summarized by Andrew Hurrell.)

In the last three decades, however, the situation has changed beyond recognition. The rearticulation of the world economy around China made South America a key provider of primary commodities to global production, and transformed the role of transnational corporations in the region—including in the rainforest. There have been a number of sophisticated efforts to map this phenomenon empirically. A recent estimate indicates that 56 percent of Amazon deforestation driven by soy croplands between 2020 and 2022 can be attributed to international, rather than domestic, consumption. In an article from 2018, Victor Galaz and his co-authors argued that the main drivers of land-use change in the rainforest are soy and beef production, and that these two economic activities are dominated by only eight corporations: four giant grain traders (ADM, Bunge, Cargill, and Louis Dreyfus, usually referred to as ABCD), the largest private soybean producer in the world (a Brazilian firm, Amaggi), and three Brazilian meat-processing firms (JBS, Marfrig, and Minerva). Galaz et al. also showed that many of these companies are tightly linked to the sixteen financial firms most involved in activities threatening biomes critical for the Earth’s climate, and especially to the ‘‘big three’’ asset managers (BlackRock, Vanguard, and State Street, all headquartered in the US).

The connection of ADM, Bunge and Minerva to these sixteen financial firms is mainly through stockownership, whereas in the case of JBS and Marfrig, ‘‘investors’ latent influence’’ operates predominantly through debt. (The three remaining firms—Amaggi, Cargill, Louis Dreyfus—are privately owned, which means that the data on their intertwinement with financial capital is limited.) The authors therefore arrive at a blunt conclusion: “the ‘Financial Giants,’ through their common blockholding power, have a previously ignored, yet considerable potential influence in companies shaping biomes critical for the stability of the climate system.’’ Last year, researchers from University College London and University of Exeter went further still, tracing the financial flows— including lending and equity and debt issuance—towards twenty-four corporations, including the eight firms mentioned above, which have been ‘‘linked to significant land use change and degradation’’ in the Brazilian Amazon between 2014 and 2023.

Academics have also made occasional efforts to get these transnational corporations to change their ways. In 2019, a group of twenty-four prominent researchers proposed ‘‘expanding the focus from ‘corporate social responsibility’ to ‘corporate biosphere stewardship,’’’ advocating ‘‘a new business logic with the purpose of shepherding and safeguarding the resilience of the biosphere for human well-being.’’ Others appealed to central banks and financial regulators, arguing that it is their mandate to deal with ecosystem degradation that ‘‘poses escalating systemic risks to economic and financial systems.’’ To restrict a ‘‘substantial portion’’ of financial flows to companies that threaten the tipping points of the Brazilian Amazon and the Indonesian peatlands ‘‘would only require coordination across relatively few financial centres.’’

The hope implicit in this literature echoes Rudolf Hilferding’s remark that the concentration brought about by finance capital could be seized upon to overcome capitalism itself—‘‘taking possession of six large Berlin banks,’’ he wrote in 1910 in Finance Capital, ‘‘would mean taking possession of the most important spheres of large-scale industry, and would greatly facilitate the initial phases of socialist policy”—except the goal here is no longer to bring about socialism, but simply to salvage a liveable planet by preventing ecosystem tipping points from being reached.

Can’t beat them? Join them

The expectation that central banks might come to the rescue in a deepening climate crisis was evidently grounded in an ephemeral conjuncture, which came to an end with Donald Trump’s return to the White House last year. Yet even if this push had succeeded, it may have had difficult side effects. As Yannis Dafermos argued, ‘‘attempts of private finance to protect itself from climate risks’’—and attempts by monetary authorities to push them to do so—may exacerbate climate finance injustice by increasing borrowing costs faced by Global South countries and deepening their financial vulnerability.

Research on the role of global capital in the climate crisis must therefore consider the impacts of corporate concentration on country-level politics, investigating the alliances built by transnational corporations with domestic elites and the potential resistance they may encounter. Seen through this lens, the case of the South American soy boom offers useful insights. Since the late 2010s South America has been responsible for more than half of global soy production and almost two-thirds of global exports of the commodity. In 2024, Argentina, Brazil and Paraguay accounted for 61 percent of all exports.

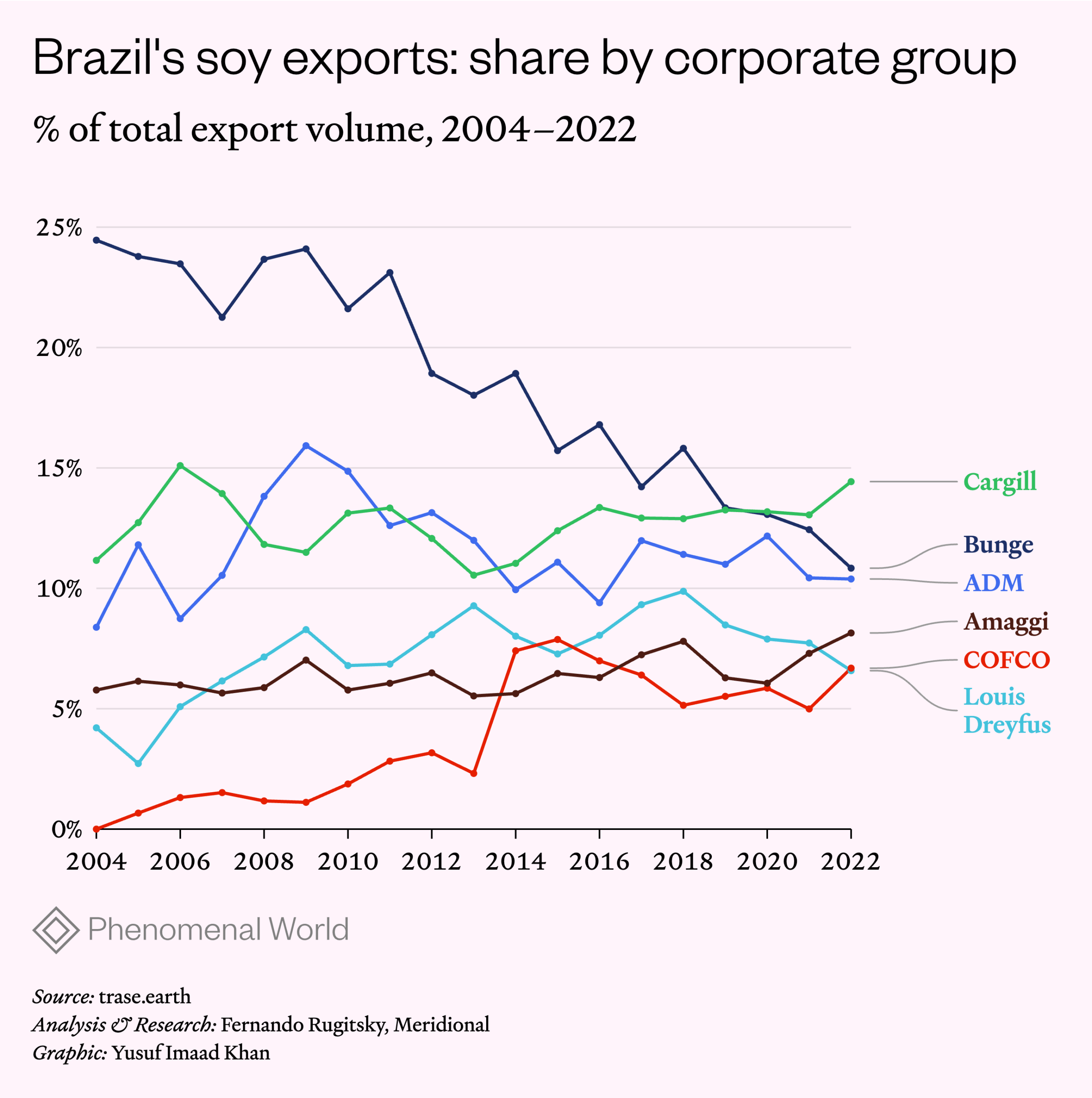

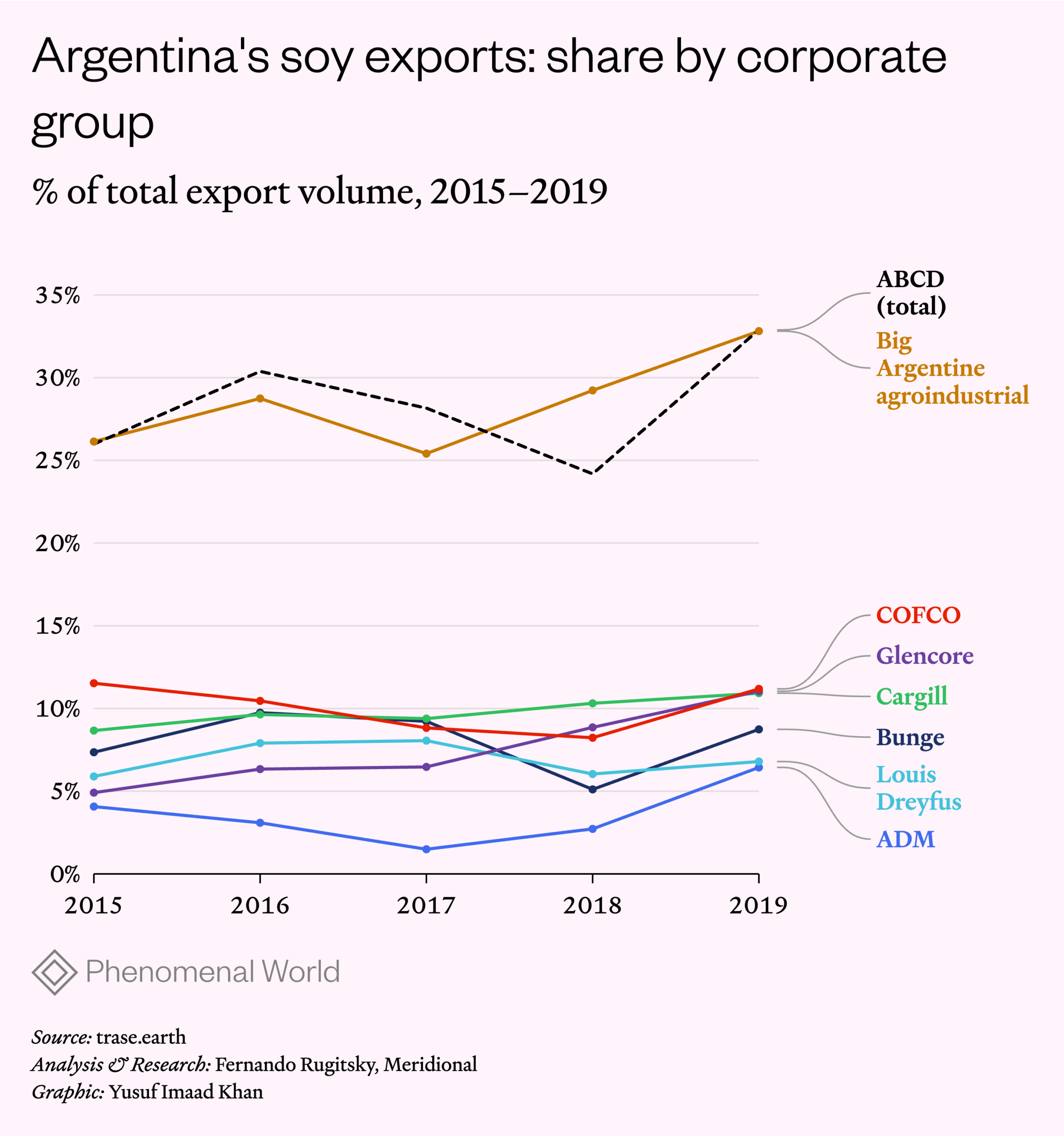

The data made available by Trase.earth is clear about the dominance of the giant grain traders in Brazilian and Argentine soy exports, as shown in the figures below. (Data includes soybeans and “the raw equivalent of the traded sub-products,” that is, ‘‘soy cake and soy oil are converted to soybean equivalent tonnes.”) Statistics for Brazil start in 2004, when the ABCD firms responded for 48.2 percent of total soy exports, in tonnes. By 2009, their share had peaked at 59.8 percent, before gradually falling over the following years, to 42.2 percent in 2022—the most recent information available. Despite the decline, the four companies remained in control of a sizable share of a booming business: in 2022, exports totalled 93.7 tonnes of soy, up from 36.2 in 2004. The data for Argentina is limited to the period between 2015 and 2019 and shows that the share of the ABCD firms oscillated between a quarter and a third of the total. Adding a fifth giant commodity trader, Glencore, brings this figure above 40 percent.

Founded either in the nineteenth or in the early twentieth century, the ABCD firms saw their global influence increase at the turn of the millennium in parallel with the expansion of future trading in commodities. Jennifer Clapp argued that this financialization of the commodity trade allowed them to “wield enormous power in shaping food systems.” Profiting from volatility that caused hunger and popular rebellions throughout the world, these corporations were known, according to Gustavo de Oliveira and Mindi Schneider, for “rerouting cargo ships mid-ocean to gain marginal profits on large volumes, and speculating on futures markets with the privileged information that results from controlling significant shares of non-transparent markets.”

In South America, their dominance was established in the 1990s through the surge in acquisitions that formed part of the process of neoliberalization. By extending the subordination of soy farmers, they set in motion a cumulative process that further tightened the companies’ grip. They squeezed prices paid to producers and so pushed them to combine intensive use of herbicides with genetically-modified seeds, “in order not to incur price deductions at the point of delivery, deepening the technological treadmill and the farmers’ need for finance.” By the early 2000s, they had come to control “the entire transportation logistics…as well as the port terminals, cargo ships and processing facilities that ultimately crushed the soybeans into meal and vegetable oil.”

South American big capital did not put up much resistance to this trend. In Brazil, Amaggi maintained its powerful position, controlling more than 8 percent of soy exports from Brazil in 2022 and around 1.6 percent of the soy croplands in the mid-2010s, partly by coordinating with the global traders. It established joint ventures with Bunge and Dreyfus and obtained funding from Mitsui (a large Japanese trader). It also had significant political influence. Its owner, Blairo Maggi, was governor of the main soy growing state in Brazil (Mato Grosso) between 2003 and 2010, senator between 2011 and 2016, and Minister of Agriculture between 2016 and 2019.

In Argentina, taxes on exports of unprocessed soybeans, strengthened large domestic agro-industrial capitalists who produced soy oil, allowing them to keep a share of total exports similar to the one of the ABCD firms (see figure above). The three largest Argentine corporations (Vicentin, AGD, and Perez Companc) controlled from a quarter to a third of total exports, between 2015 and 2019. (Embroiled in a series of scandals after 2019, Vicentin would eventually be rescued by an Argentine businessman with the support of Cargill.)

Chinese state capital posed a more significant challenge. Following the so-called “2004 soybean crisis” in China, when a sudden change in the global price of the commodity pushed a number of Chinese processing firms into bankruptcy, the ABCD firms saw their control of the Chinese market surge. In response, the government prioritized the growth of Chinese traders, especially COFCO, in a dispute dubbed the “battle of the beans.” (See Tomaz Fares’ detailed account.) The ripples were eventually felt in South America: in Brazil, COFCO started exporting soy in 2005 and, since 2014, became responsible for a share between 5 and 8 percent of total exports; in Argentina, its share was even higher, around 10 percent, between 2015 and 2019. A substantial part of the post-2009 decline in the share controlled by ABCD in Brazil is explained by the rise of COFCO. Yet the shift in market shares may exaggerate the actual challenge. Being treated initially with “particular hostility” from the ABCD, who aimed “to maintain their oligopolistic control over soybean exports,” COFCO was forced to build alliances with the incumbents, reaching a preferential agreement with ADM. If you can’t beat them, join them.

Corporate concentration and South American politics

The rise of COFCO is unlikely to bring effective competition to the industry, simply expanding from four to five the firms at the helm of the oligopsony of South American soy. Given their focus on processing, marketing, and logistics, the real material process of growing soy is still done by a multitude of farmers, large and small. A tiny minority, usually backed by foreign and domestic financial capital, owns vast tracts of cropland and manages to retain some autonomy relative to the traders. Estimates with data from the mid-2010s indicated that seven giant farm management companies—pools de siembra, as they are called in Argentina—controlled almost 7 percent of all hectares planted with soy across Argentina, Brazil, and Paraguay. In Brazil alone, five of them (including Amaggi) accounted for about 5 per cent of the soy cropland area.

Yet these are the exceptions, giant as they are. The vast majority of the soy farmers are significantly smaller, including large numbers of medium- and smallholders, who due to their size are deeply subordinated to the trading oligopsony. They are not only price takers but have lost most of the control of their own operations. “The nature and ‘autonomy of farming’ are increasingly disciplined and structured by external forms of management based on the application of technological packages and farm-service logistics,” Oliveira and Hecht wrote. In Argentina, this transformation of farming is referred to as sojización, characterized “by higher levels of capitalization, mechanization, foreign investment and economies of scale.”

The political constituency represented by this multitude of farmers, connected to the most dynamic sector of the region’s economies, could in principle have been mobilized against the oligopsony, demanding a different organization of the supply chain. But instead, subordinated rural groups, suspicious of the center-left governments that presided over the consolidation of the trading oligopsony, turned sharply to the right. In Brazil, these radicalized soy farmers rose through the ranks of state-level soy producer associations to hegemonize rural politics for the country as a whole, providing Bolsonaro with a key electoral base. This marked the birth of what Caio Pompeia calls agri-bolsonarismo.

A similar development can be identified in Argentina. In 2008, when the government of Cristina Kirchner moved to increase taxes on the exports of soy, it was resoundingly defeated by a large coalition in a struggle that is now referred to as the crisis del campo, which Diana Córdoba and her co-authors described as a “rural protest of unprecedented scale in which disparate and historically fractured rural interests united in a common protest that lasted for months.” They went on to explain how

Landowners, contractors, workers, hauliers and other rural actors—representing the rural elite, smallholders and the rural working class—participated together, using trucks and farm equipment to install blockades on rural routes and cutting off the movement of agricultural (and other) products throughout the core agricultural region.

Some have argued that the origins of Argentina’s rightward movement—first with the election of Mauricio Macri in 2015, then with the victory of Javier Milei in 2023—can best be found in this crisis of 2008. In both Argentina and Brazil, then, the economic transformation led by the giant grain traders increased the countries’ foreign vulnerability at the same time as it sowed the seeds of anti-democratic politics. These examples from recent South American history reveal that corporate concentration in the global food industrial system not only threatens food security and fuels climate change, but also weakens democratic institutions. When the indigenous groups faced down Cargill earlier this year, it was not only their livelihoods that were at stake.

Filed Under

Further Reading

Hockey Sticks and Crosses

Images that define the globalization debate

Images that define the globalization debate

The Chainsaw and the Miracle

Milei's structural adjustment program.

Argentina's midterm elections have given Milei a renewed mandate to slash the state, working in concert with the IMF and US Treasury.

April is the Cruelest Month

Diversification and dedollarization in the world economy

Investing in the US has been a good bet for well over a decade. America’s tech industry, its indefatigable consumers, highly profitable firms, and pro-growth...