July 25, 2025

Analysis

Rebuilding the Kingdom

Transformations of state, economy, and class in Saudi Vision 2030

Saudi Arabia’s Crown Prince Mohammed bin Salman first announced Saudi Vision 2030 (SV2030), an economic diversification-cum-social reform plan, during an interview with Al Arabiya in April 2016. SV2030 vowed to transform Saudi Arabia, proposing fantastical ventures into the future while aggressively deploying capital abroad and opening the domestic economy up via debt issuance, investment code reform, contracting, and capital market reform. Knock-on effects for the world economy were imminent.

Facing volatility in the commodities market and growing financial vulnerabilities, the oil-dependent nation has since embarked on an effort to remake itself as a global economic powerhouse. Alongside ever expanding flows of crude to the east and deepening investment ties with China, Saudi Arabia’s moves on the home front looked primed to tilt the axis of global capital accumulation. The nine years since SV2030’s announcement have seen gains across a number of domains. The country has already cleared original targets for female labor-force participation and tourism. It is also likely to meet its goals in the capital markets. Courtesy of Aramco’s limited IPO, the Saudi Exchange now ranks as the ninth largest stock market in the world by market capitalization and the third largest among emerging markets.

SV2030 has also prompted an enormous wave of construction in its bid to reshape the country’s built environment. Despite its population of just 30 million, Saudi Arabia is poised to host the largest construction market in the world by 2028.1Valentina Pasquali, “Riyadh dominates Saudi Arabia’s construction market”, (<)em(>)Arab Gulf Business Insight (<)/em(>)(June 25, 2024). Neom—the giga-project being conjured out in the western province of Tabuk along the northern shores of the Red Sea—is alone absorbing 20 percent of the global steel supply.2Andrew Hammond, “Neom ‘uses one fifth of world’s steel”, (<)em(>)Arab Gulf Business Insight (<)/em(>)(October 15, 2024). The plan’s housing program aims to achieve 70 percent Saudi national home ownership in 2030; as of 2024, official statistics estimate ownership in the range of 62–65 percent, up from 47 percent in 2016. Most importantly as pertains to SV2030’s overarching goals, the non-oil economy has expanded at a greater pace than the oil economy in recent years.3 Concerning statistical coding, note that the processing of petroleum is classified as a service activity in government accounts, while petrochemical production is registered as a non-oil output. The construction boom reflects the scale of Saudi Arabia’s rapidly shifting relationship with global financial markets.

SV2030 is betting that the world’s great oil power can transform itself into a real-estate empire. The administrative centralization configured to oversee this restructuring has generated a byzantine network of institutional actors operating outside the traditional boundaries of the Saudi state. Managed by a network of foreign consultants, this new formation has weakened government accountability, eliminated transparency, and diminished the influence of longstanding ruling families in the domestic economy.

There are also immense social consequences to the build: SV2030 is generating polarizing wealth effects within what is already one of the most unequal countries on the planet. An economic model long founded on the distinction between its citizen and migrant labor populations is now generating class divisions within the Saudi national population. Seen in full, these changes point to the political, economic, and social tensions embedded in the ambitious developmental visions being pursued under the reign of King Salman and the Crown Prince Mohammad bin Salman.

Vertical administration

It was exigency that had prompted SV2030. In the lead-up to the Crown Prince’s ascension, commodities markets were rattled by regular bouts of volatility, first in the aftermath of the 2008 financial crisis and then more consequently and lengthily beginning in June 2014. Due to the Saudi treasury’s acute dependence on transfers from Aramco—the company’s contributions represented over 90 percent of government revenues between 2010 and 2014—doldrums in the oil trade posed questions of an existential nature.4Stephan Roll, “A Sovereign Wealth Fund for the Prince”, Research Paper: Stiftung Wissenschaft und Politik (July 2019). As Mohammed bin Salman well knew, dollars and US treasuries would be run down in short order were the deficits of recent years sustained.5For a sense of scale, the net lending/borrowing of the general government averaged out at -10.4 percent GDP between 2014 and 2017. With a 2015 study commissioned by McKinsey Global Institute also sounding the alarm on unemployment, demographic expansion, and a possible energy transition, an intervention was needed.6McKinsey Global Institute, “Saudi Arabia Beyond Oil: The Investment and Productivity Transformation”, Report (December 2015). Growth, social peace, and even regime survival conceivably held in the balance.

A project of SV2030’s scale was to require an equally ambitious rewiring of the state. To facilitate SV2030 and consolidate power in the Crown Prince, the traditional administrative state was made more vertical: once the fiefs of select royals, each government ministry is now directed by a loyalist of the Crown Prince and directly subordinate to the Diwan. Whereas family governance was previously organized around a spoils system that doubled as a mechanism for elite coalition maintenance, King Salman has emphasized the supremacy of the ruler. Upon succeeding his half-brother Abdullah in January 2015, Salman announced a leadership reshuffle that ousted the progeny of his predecessor along with other senior family figures from perches atop governorships and ministries. To snuff out sparks of dissent, the King simultaneously appointed his son, Mohammed bin Salman, Secretary of the Royal Court. With the subsequent merger of the King and Crown Prince’s offices within the Royal Court, Salman and son acquired close to total disciplinary reach. Thereafter, the two progressively disavowed the arrangements which had converted public institutions into the inheritable property of particular family lines.

Accompanying the handling of family business was a transformation in the institutional fabric of the state. Immediately after taking the reins, King Salman abolished eleven supreme councils and dissolved a handful of government ministries. He then established two sub-cabinets, each chaired by his son as of summer 2017, to preside over all economic and security policy: the Council of Economic and Developmental Affairs (CEDA) and the Council of Political and Security Affairs (CPSA), respectively.7Mohammed bin Salman was appointed chairman of the CEDA from the start and took over the CPSA after becoming Crown Prince in summer 2017. The CEDA took on the role of oversight body for SV2030.8Operationally, the Council’s Strategic Management Office was made superintendent, moving across the state without jurisdictional limit, releasing quarterly performance reports, and dispatching its “delivery unit” to whip (or sidestep) the bureaucratic ranks. In its supervisory work, note the Strategic Management Office is aided by the National Center for Performance Management. Chairing both bodies is the Crown Prince’s close confidant and trusted economic advisor Fahad bin Abdullah Toonsi. Through the King’s initial cabinet reshuffle in 2015 and subsequent moves in 2018 (in the wake of Jamal Khashoggi’s murder) and 2020, a crew of technocrats took over all the key posts at the Council of Ministers. The majority came to their posts from previous stops in international finance, their newfound prominence owed entirely to their relationships with the Crown Prince. The era of loyalist banker-technocrats has meant a de facto straightening of the chain of command.

The Economic Braintrust for SV2030

| NAME | POSITION | PROFESSIONAL BACKGROUND |

|---|---|---|

| Mohammed al Jaadan | – Minister of Finance (2016–) – Minister of Economy and Planning (2020–) – Chairman of Capital Markets Authority | – Commercial Law – Former Special Adviser to Board of Morgan Stanley Saudi Arabia |

| Mohammed bin Abdulmalek al Sheikh | – Minister of State Advisor to Crown Prince – Chairman of Capital Market Authority – Chairman of Saudi Authority for Intellectual Property – Member of CEDA – Head of Saudi Sports Authority | – Saudi Arabia Representative to World Bank |

| Mohammad al Tuwaijri | – Minster of Economy and Planning – Minister-ranked advisor to Royal Courtesy | – Group Managing Director of HSBC Holdings PLC MENA & Turkey – Managing Director of JP Morgan – Head of Treasury Saudi British Bank |

| Fahad bin Abdullah Toonsi | – Advisor to Royal Court – Secretary General of the Strategic Management Office – Board Member for Qiddiya, Neom, AMAALA, and the Red Sea Project – Saudi Representative to G20 – Managing Director of the Crown Prince’s Court | – PhD Financial Economics and Corporate Governance, King’s College London – Senior Manager PriceWaterhouseCoopers |

| Yasir al Rumayyan | – Governor of the PIF – Chairman of Saudi Aramco – Chairman of Maaden – Chairman of Riyadh Air H- ead of Securities Capital Market Authority – Board Member Tadawul | – Head of International Brokerage Saudi Hollandi Bank – CEO of Saudi Fransi Capital |

| Ahmed bin Aqil Al Khatteb | – Minister of Tourism – Former head of General Entertainment Authority – Advisor to Saudi Royal Court – Chairman of Board for Saudi Arabian Military Industries – Chairman of Board for Saudi Fund for Development – Board Member: PIF, CEDA, National Development Fund. Diriyah Gate Development Authority | – Founder Jadwa Investments Riyadh Bank – SABB Bank |

| Majed bin Abdulah al Hogail | – Minister of Municipalities, Rural Affairs, and Housing – Chairman of Saudi Real Estate Refinance Company – Chairman of Real Estate General Authority (REGA) – Head of Housing Program of Saudi Vision 2030 – Member of CEDA – Board member for Neom, Roshn, Qiddiya, Red Sea Global, and AMAALA | – Chairman Aljazira Capital – Vice Chief Financial Officer Saudi Arabian Monetary Agency – Board member Credit Suisse |

| Fahad Al Saif | – Head of Investment Strategy, Economic Insights, and Global Capital Finance Divisions for PIF | – Saudi British Bank – HSBC Saudi Arabia – Board Vice Chairman Bahri Company – Director of Gulf International Bank |

| Ahmed al Rajhi | – Minister of Human Resources and Social Development – Board member for National Development Fund – Director of Modon Member of National Industrial Company | – Al Rajhi Holding |

| Mohammed bin Saleh al Buty | – CEO National Housing Company – Advisor to Minister of Municipal and Rural Affairs |

Salman’s institutional reforms also served to reduce the operational autonomy once granted to select pillars of the state. Historically, two institutions had been charged with managing the country’s patrimony: the central bank (SAMA, previously known as the Saudi Arabian Monetary Authority) and Saudi Aramco. Each had been freed from undue political meddling as past rulers identified their own prospects being tied to SAMA and Aramco’s competence. Salman and his son, however, hitched both institutions to their political project. In 2020, SAMA was obliged to transfer $80 billion in foreign reserves to the Public Investment Fund (PIF), chaired by the Crown Prince, and fall in line with the PIF’s asset management and oil rent investment strategies.9See: Alexis Montambault Trudelle, “Diversification meets personalization: the strategic role of the Public Investment Fund in Saudi Arabia”, Analysis: Noria Research (January 2025). Similarly, Aramco was forced into a number of transactions in support of the PIF, including transferring 16 percent of company equity to the Fund, acquiring a 70 percent stake in the PIF-owned Saudi Basic Industries Corporation, and issuing debt to provide the PIF with liquidity (by way of dividend payments).

Aramco’s leadership has also been brought under the direct thumb of the royal court. Khalid al-Falih was removed as Chairman in 2019 and Minister of Energy in 2020. Prior to al-Falih’s dismissal, the Aramco portfolio had always come attached with the top job at the Ministry of Energy, and appointments to the two-file job had been reserved for petroleum doyens of high regard.10The likes of Abdullah Tariki and statesman-like Ahmed Zaki Yamani. Today, nomination to the now-split gigs of Minister and Chairman is governed by a clear political logic. Running the Ministry is the Crown Prince’s half-brother Abdulaziz bin Salman while handling Aramco is the Crown Prince’s trusted advisor Yasir al-Rumayyan. As a result of this reorganization, pockets of institutional independence which formerly stabilized the monarchy no longer exist.

The parallel state

Salman’s reforms, jointly aimed at concentrating power and streamlining the roll out of SV2030, additionally served to equip the King and his son with what amounts to a state outside the state: a configuration of new planning, administrative, and financial bodies as well as regime-owned commercial entities, all directly accountable to the Crown Prince.

This parallel government relies on an intellectual engine of management consultants and financial professionals, including nationals and foreigners. Manifest in BCG’s enormous new office in the King Abdullah Financial District and in consulting industry revenues coming in well north of $3 billion per annum since 2023, the consultants’ rise infuses planning with both rationalism and risk. Alongside the Crown Prince’s inner circle, the apparatchiks of SV2030—strategists, planners, project managers, and bankers—are a transnational assemblage. Public policy mercenaries chasing short-term contracts are bound to their work neither by ideology nor patriotism and face no disciplinary structures apart from being fired or frozen out (see: PriceWaterhouseCoopers, most recently). If these actors have assisted in turning the focus to efficiency and investment returns, they have also helped marginalize the standing of developmentalism—and all its social contents—within the policy debate.

The Strategic Management Office (SMO) of the CEDA is in charge of most of the policy planning for SV2030. As coordinator and monitor for the eleven grand “Vision Realization Programs,” the SMO is empowered to bypass or impose itself upon government ministries. Like the Council to which it reports, this office relies heavily on consultants seconded to the government by Boston Consulting Group and Kearney.11Personal correspondence, March 2025. External experts are entrusted with developing the SMO’s strategy, specifying delivery plans and objectives, and managing Vision projects downstream.

The PIF plays a significant planning role, too. Once an asset manager of the Ministry of Finance established to foster national industrial champions, the PIF was brought under the direct command of the CEDA in 2015, and its C-suite is dominated by Saudi and expat career finance professionals. That same year, the Fund was also legally restructured as an investment company with full ownership rights over the assets on its balance sheet.12By way of the second move, PIF holdings and activities are registered as part of the private sector in national accounts. In controlling so much of SV2030’s off-budget fiscal spend, it is the PIF’s decisions that materially animate much of the Crown Prince’s diversification strategy. Given that the board, chaired by the Crown Prince, retains full discretion in making investment decisions, the PIF’s insertion into the policy space amounts to a deeper concentration of royal power.13A consultative role provided by the Investment Strategy and Economic Insights Division.

A handful of other extra-bureaucratic institutions have come into the planning fold of SV2030. The PIF Program Office, also chaired by the Crown Prince, directs the five Giga Projects—Neom, Roshn, Red Sea Global, Qiddiya, and Diriyah—that together generate much of the demand for new structure and infrastructure. The PIF owns Ardara, a non-Giga real estate development vehicle, and has been the majority-owner of the largest mining company in Saudi Arabia (Ma’aden) since its foundation. The PIF also holds majority positions in many of the leading firms in the cement sector. More recently, the Fund has cobbled together a national steel champion and taken a 30 percent stake in Masdar, the latter specializing in the trading and distribution of building materials.

Chaired by Minister of Municipalities, Rural Affairs and Housing Majed bin Abdullah al Hogail, the Housing Program Office of SV2030’s mandate encompasses real estate development and strategizing the wider housing transition. Regulation and consumer protection has been turned over to the freshly founded Real Estate Governing Authority (REGA). Established in 2017 and chaired by the same al Hogail, REGA’s regulatory remit is anchored to attracting investment into the built environment. Institutions of SV2030’s parallel state likewise preside over the design and administration of industrial policies related to boosting local content use in construction.14The Ministry of Industry and Mining is not left entirely in the cold, it should be said, as the Future Factories Program runs through its offices. Nevertheless, the main players are the PIF and the National Housing Company (NHC). Through the mother institution, majority-owned subsidiaries, and Giga stock companies, the PIF leads the charge in developing domestic manufacturing capacity while the NHC plays second fiddle. Also part of the SV2030 push, the NHC was established in 2016 as a real estate investment fund. While backed and partially capitalized by the state treasury—and while legally housed within the Ministry of Municipalities, Rural Affairs and Housing—NHC operations are insulated from the traditional state bureaucracy. It supports domestic production of building materials through a number of initiatives, including the Rakaez Program, Logistics City Project, and Industrial Links Program.

Three sectors of the parallel state are critical to the funding of the build.15Having only just held its inaugural board meeting, note that the National Infrastructure Fund—which is under the orbit of the NDF, like the REDF—will likely be added to this mix going forward. Essential to the demand and supply sides of SV2030’s real estate agenda are the country’s commercial banks—namely Saudi National Bank (SNB), Alinma Bank, and Riyad Bank. Though none are pure instruments of SV2030, each is primarily owned by the PIF—and all have been enlisted to serve the SV2030 agenda.16The latter fact is attested by the patterns of their credit allocation, which have quite clearly shifted in accordance with the goals of the Housing Program. In the case of SNB, moreover, service to 2030 is made quite explicit. Not only are commitments to SV2030 apparent in the bank’s mission statement, which lists “catalyzing the delivery of Saudi Vision 2030” as an objective and obligation: The PIF’s fingerprints, and by extension SV2030’s, are also all over the 2021 merger which expanded the SNB’s balance sheet and in so doing, facilitated greater lending to targeted sectors. Second, also making a critical financial contribution to SV2030’s build is the Real Estate Development Fund (REDF). Though itself a legacy institution, REDF was repurposed for Vision-service upon its being absorbed by the National Development Fund (NDF).17The NDF was established by royal decree in 2017 to provide capital investment for SV2030. It is chaired by the Crown Prince and its board is comprised largely of the technocrats listed in the table above. Its financing predominantly runs through two channels: Guarantees provided to mortgage lenders and, via the Sakani Program, interest subsidies and down payment supports provided to home buyers.18Through the Sharakat program, the REDF, in conjunction with the Ministry of Municipalities, Rural Affairs and Housing, does also provide financing to builders and developers. Finally, the Saudi Real Estate Refinance Company (SRC), fully-owned by the PIF, is tasked with injecting liquidity into the banking sector and developing the secondary real estate market, providing banks with capital relief, purchasing mortgages to free up the balance sheets of lenders, and pioneering the securitization effort, on the advice of Blackrock.19Adelaide Changole, “Saudi Arabia Taps BlackRock to Build Mortgage-Backed Securities Market”, (<)em(>)Bloomberg (<)/em(>)(October 23, 2024). In conjunction with Hassana Investment Company, this past January the SRC began bundling and cutting up mortgages for trading on secondary markets.20Nadin Hassan, “SRC and Hassana launch mortgage-backed securities to boost Saudi real estate investment”, (<)em(>)Arab News (<)/em(>)(January 2, 2025); At a more junior level, note that the Roshn Group offers a hand with finances as well. Also fully-owned by the PIF, this institution indirectly facilitates credit lines to developers working on its massive housing builds. Most recently, it has done so via a syndicated loan arrangement (USD 2.4 billion) with four national banks that will see the Roshn Group backstop credit lines for contracted business partners.

In one sense, the changes wrought by Salman have served to cohere the bureaucracy of the new ministerial class to the Crown Prince and their collective population of the CEDA. But with everyone forced to manage up, inter-ministry relations, never strong to begin with, have been entirely severed.21Author Personal Correspondence: February 2025. Extreme verticality means that all but those at the top are excluded from the policy process. No one lifted to leadership positions by the Crown Prince are of the ministries they now direct, creating confusion at lower bureaucratic levels as well as uncertainty in execution. The administrative organization of the state is becoming denser and more labyrinthine. Jurisdictional overlap follows, as do government entities working at cross-purposes with one another.22Hadi Fathallah, “Challenges of Public Policymaking in Saudi Arabia”, Commentary: Carnegie Sada Center (May 2019). David B. Jones, “King-makers or knaves? The role of consultants in domestic policymaking and governance in Saudi Arabia” in Mark C. Thmopson and Neil Quilliam (eds.)(<)em(>) Governance and Domestic Policymaking in Saudi Arabia: Transforming Society, Economics, Politics and Culture(<)/em(>) (I.B. Tauris: 2022).

While the PIF is not run as a blacksite—a recent auditor’s report from KPMG establishes some basic data—there are still many unknowns about the Fund’s dealings. How to explain, for instance, the 40 percent increase in employee costs in 2023 (a jaw-dropping bill of $15.9 billion)?23Andrew Hammond, “The huge ambitions of PIF come at vast expense”, (<)em(>)Arab Gulf Business Insight (<)/em(>)(September 20, 2024). Gaps of USD hundreds of billions when it comes to book assets and assets under ownership? The about-face in the marketing of Giga Project real estate, now targeting Saudis rather than foreigners? The turnover at the top of Giga projects like Neom and reports of gross executive misconduct?24Rory Jones, “The world’s biggest construction project is a magnet for executives behaving badly”, (<)em(>)Wall Street Journal (<)/em(>)(September 11, 2024).

The murkiness of procurement instead suggests a shift in primary beneficiaries. Available evidence shows a handful of families—the Al Rajhi, al Muhaidib, Al Issa, al Zamil, al Subeaei, and al Sudairi, many of whom had younger members intersect with the Crown Prince during his time at Jadwa Investments—riding SV2030 to new heights. Furthermore, hearsay abounds that the Crown Prince and his brothers are taking personal cuts on many of the major developments underway.25Author personal correspondence, February 2025.

The amalgamation of new agencies comprising the parallel government creates ambiguities over who is responsible for policy—and by extension, deserving of blame. In moving expenditures and liabilities off the books, this configuration also obscures the realities of the state’s financial commitments, while subtly vesting the Crown Prince with Leviathan-like authorities and allowing him to micromanage SV2030 and take personal direction of investment operations.

Debt-financed housing

In the immediate aftermath of the first Gulf War and during the commodities boom of the early 2000s, Saudi policymakers tried squeezing growth and political legitimacy from the laying of concrete, glass, and rebar.26Rosie Bsheer, “The Property Regime: Mecca and the Politics of Redevelopment in Saudi Arabia”, (<)em(>)Jadaliyya (<)/em(>)(September 8, 2015); Michelle Buckley and Adam Hanieh, “Diversification by Urbanization: Tracing the Property-Finance Nexus in Dubai and the Gulf”, (<)em(>)International Journal of Urban and Regional Research (<)/em(>)38:1 (2014). Like these earlier leaders, the Crown Prince today has entrusted the state with responsibilities for leading new industries and folding select private capitals—both domestic and foreign—into ventures downstream.27For previous iterations, see: Adam Hanieh,(<)em(>) Money, Markets, and Monarchies: The Gulf Cooperation Council and the Political Economy of the Contemporary Middle East(<)/em(>) (Cambridge University Press: 2018). As before, profitability has again been hitched to the super exploitation of a vulnerable workforce.28 See: Staff writer, “Saudi Arabia: ILO Forced Labor Complaint a Wake-up Call”, News Release: Human Rights Watch (June 5, 2024). Last fall, an ITV documentary estimated 21,000 migrant workers had died on construction sites since SV2030’s launch.29Staff Writer, “Saudi Arabia: ITV finds migrants constructing ‘The Line’ at megacity project, Neom, experience egregious labour rights abuse”, Business & Human Rights Resource Centre (October 28, 2024).

SV2030’s housing program has launched a contracting bonanza. State and state-adjacent entities awarded just short of $147 billion in contracts in 2024, with the power and construction sectors leading the way.30Mohamed Ali Omar and Junaid Ansari, “GCC Projects Market Update”, Report: Kamco Invest (January 2025). Middle East Economic Digest estimates the value of projects currently in the pre-execution stage at $770.5 billion. Narrowing the focus to real estate, the value of projects commissioned between 2016 and 2024 topped $164 billion, with another $250 billion in the hopper.31Roughly one-fifth of this spend has been deployed for Riyadh-based developments, and one-third out west in support of Neom. The full realization of the Crown Prince’s objectives for real estate and infrastructure development will come with a bill of $1.3 trillion. But if there is much that is familiar in Saudi’s latest build, novelties abound as well. The capitals, institutions, and financial engineering involved all break new ground. Appreciated in full, these changes speak to a partial rupture within the Saudi accumulation regime.

Named the GCC’s top developer for 2024, the National Housing Company (NHC) is the master real estate developer for SV2030. It projects to bring 600,000 housing units to market by 2030, claims to have added 600,000 jobs to the economy last year, and aims for revenues of approximately $14 billion in 2025.32Edmund Bower, “National Housing Company announces record revenue”, (<)em(>)Arab Gulf Business Insight (<)/em(>)(January 23, 2025). The PIF has wide-spanning commercial holdings in the construction and real estate development space as well. On the contractor side of things, the PIF took equity positions in four major construction companies in early 2023.33The four are AlBawani Holding Company, Almabani General Contractors Company, El Seif Engineering Contracting Company, and Nesma & Partners Contracting Company. At the time of writing, the Fund is also preparing to take over the 36 percent stake that the Ministry of Finance currently holds in the Saudi BinLadin Group.34The MoF acquired this position after the BinLadin Group’s owners were coerced into paying a penance for past deeds during the shakedown at the Ritz Carlton.

SV2030’s roll-out of new structure and infrastructure is leaning heavily on government debt. The Ministry of Finance has issued tens of billions in bonds and sukuk per annum in recent years. Aramco has taken on debt in order to indirectly support the build as well: In 2021 and 2024, the company issued a total of $12 billion in medium-term traditional and Islamic bonds, proceeds of which were used to pay dividends to the PIF, amongst other things. The Saudi Real Estate Refinance Company has issued bonds and sukuk as well, and it is expected that the holding companies in charge of the Giga Projects, such as the one overseeing Neom, will join the bond issuance party.

Nor has SV2030 debt financing been limited to the selling of fixed-income securities. State and sub-state entities have borrowed billions through the arrangement of private revolving credit facilities. For instance, in 2023, the Ministry of Finance reached an agreement on a ten-year, $10 billion syndicated loan earmarked for construction, with the Industrial and Commercial Bank of China as the main lender.35Saudi Debt Agency Annual Report. This January, the Ministry tapped Abu Dhabi Islamic Bank, Credit Agricole, and Dubai Islamic Bank for a $2.5 billion revolving credit line to fund construction.36Abeer Abu Omar, “Saudi Arabia starts 2025 with a $12 billion bond and PIF loan”, (<)em(>)BNN Bloomberg (<)/em(>)(January 6, 2025). Downstream, the holding company for the Roshn Giga Project—a fully-owned subsidiary of the PIF—also secured a syndicated loan worth SAR 9 billion (~$2.4 billion) from a consortium of domestic banks at the start of 2024.

By far the most active in the private credit space, however, is the PIF itself. In 2021 and 2024, the Fund secured three-year credit facilities (extendable up to five years) of $15 billion from an international consortium. In 2018 and 2022, it also borrowed $11 billion and $17 billion, respectively, in the form of unsecured general corporate purpose loans.37Staff writer, “Saudi PIF secures record-breaking $17bn seveny-year senior unsecured term loan”, (<)em(>)Arab News (<)/em(>)(November 30, 2022). To further diversify private credit lines, the PIF moved into the Islamic lending market at the start of 2025 as well. Structured as a Shariah-compliant murabaha facility, the Fund secured a revolving credit line of $7 billion from a consortium of twenty international banks.38Staff writer, “A&O Shearman advises on PIF’s first syndicated murabaha facility”, Client News: A&O Shearman LLP (January 14, 2025)

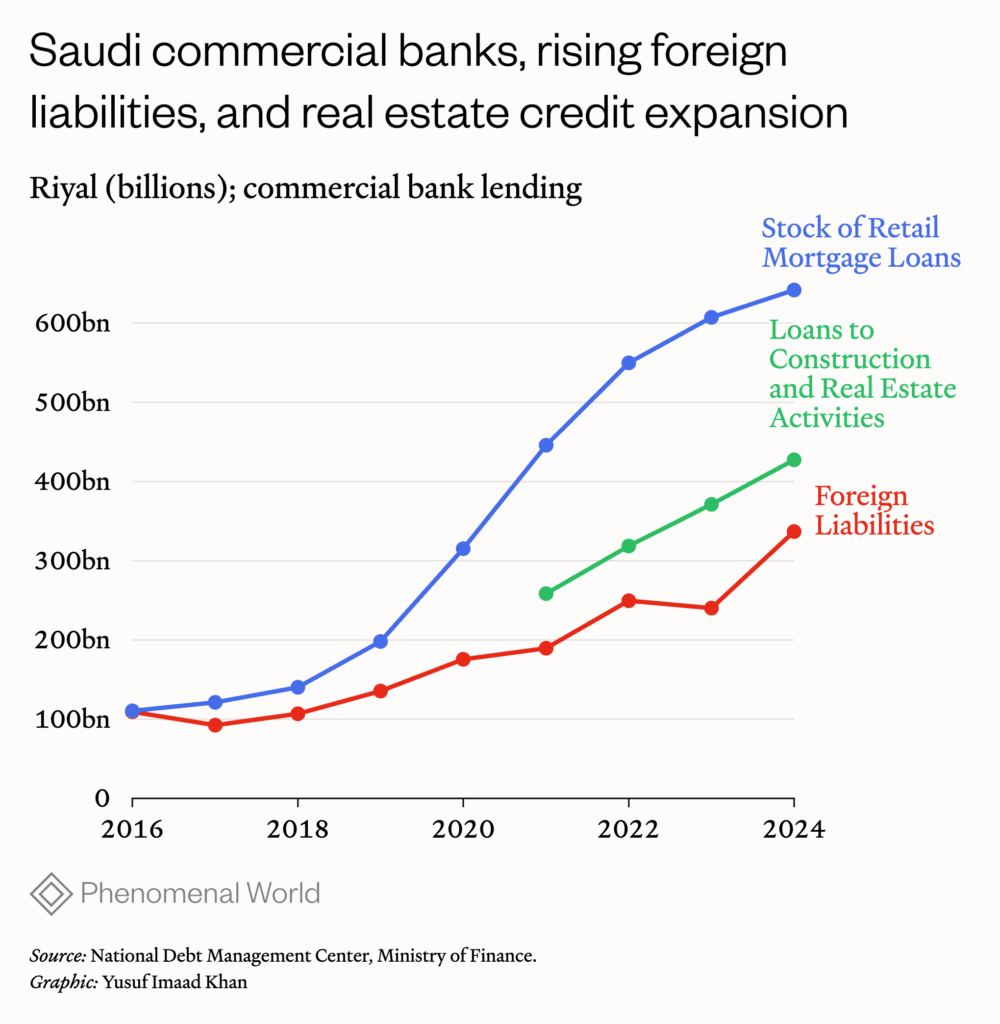

Saudi’s commercial banks have also leveraged up to support the build. This was necessary due to the widening gap between deposit growth—relatively weak, especially if one excludes public entities—and borrowing demand. Since the pandemic especially, the latter jumped as a result of the (state-backed) construction boom and (state-backed) spike in mortgage demand. To fund lending, Saudi banks first sold billions in t-bills on domestic markets. Insufficient for capitalizing their needs, they next issued billions in foreign currency bonds and sukuk.39Staff writer, “Saudi Banks’ credit equality may weaken due to external funding reliance”, (<)em(>)Fitch Wire (<)/em(>)(October 21, 2024). Most recently, these institutions have been selling risky, short-term debt (Additional Tier 1 bonds) to free up liquidity for lending.40Tasos Vossos, Abhinav Ramnarayan, and Olga Voitova, “Saudi banks are on risky debt spree to keep funding gigaprojects,” (<)em(>)Bloomberg (<)/em(>)(June 4, 2025). Graphing external liabilities against credit to home buyers and builders shows the extent to which foreign debt is lubricating the property market.

Sinews of debt

SV2030 has changed the country’s incorporation within financial markets. During the first half of 2024, USD-denominated bond and sukuk issuance were such that Saudi Arabia displaced China as the top issuer of dollar debt in emerging markets, the first country to do so in twelve years.41Selcuk Gokoluk, “Saudi Arabia Dethrones China as Top Emerging-Market Borrower”, Bloomberg (June 19, 2024). The Kingdom settled into second position by the close of 2024, recording 51 percent year-on-year growth; in 2025, the country’s USD-denominated fixed income market is expected to jump by approximately another 15 percent to more than $500 billion.42Lest a recent decision by the Accounting and Auditing Organization for Islamic Financial Institutions throws a spanner in the works. Fixed Income Team, “GCC Bonds and Sukuk Market Analysis”, Report: Markaz Research (January 2025); Staff Writer, “Saudi debt capital market to exceed USD 500 bn this year – Fitch ratings”, Enterprise Saudi Arabia (February 5, 2025). With S&P raising the long-term foreign and local currency sovereign rating to A+, debt sales should fly for a number of years still. Saudi Arabia’s capital markets are now also demonstrating that they possess the liquidity and accessibility needed to play a role internationally. In these regards, China’s issuance of a $2 billion bond on the Saudi Exchange last November offers the clearest testament to the ongoing success.43Both the subscription amounts ($39.73 billion) and the yields (but a few basis points higher than US treasuries of equivalent maturities) left impressions. Matt Smith, “Investor demand lowers yields on China’s dollar bonds”, Arabian Gulf Business Insight (January 6, 2025).

Saudi’s presence in the global financial circuitry is not new, of course. By virtue of petrodollar recycling, Riyadh long served as a constitutive fiber for Wall Street and for Eurodollar lenders. By way of the mega-project boom of the early to mid-2000s, internally-facing funding relations with the HSBCs and Deutsche Banks of the world had been established, too.44See: Buckley and Hanieh (2013). Nevertheless, SV2030 prompted three major shifts.

Firstly, SV2030 reversed the primary direction of movement for the capital flows: Rather than petrodollars flowing out, it is debt (and to a lesser extent, equity) financing rushing in which is binding Saudi to external financial networks. The reversal itself is not entirely unprecedented. During the early 1990s, slumping oil revenues led to extensive foreign borrowing and the establishment of a hot treasuries market that was much enjoyed by foreign traders.45Author Correspondence, December 2024: Paris. See as well: Muhammad al Jasser and Ahmed Banafe,”The development of debt markets in emerging economies: the Saudi Arabian experience”, Paper no.11: Bank for International Settlements (2002). Nevertheless, the prevailing direction of capital flows today contrasts with the rest of Saudi’s modern history.

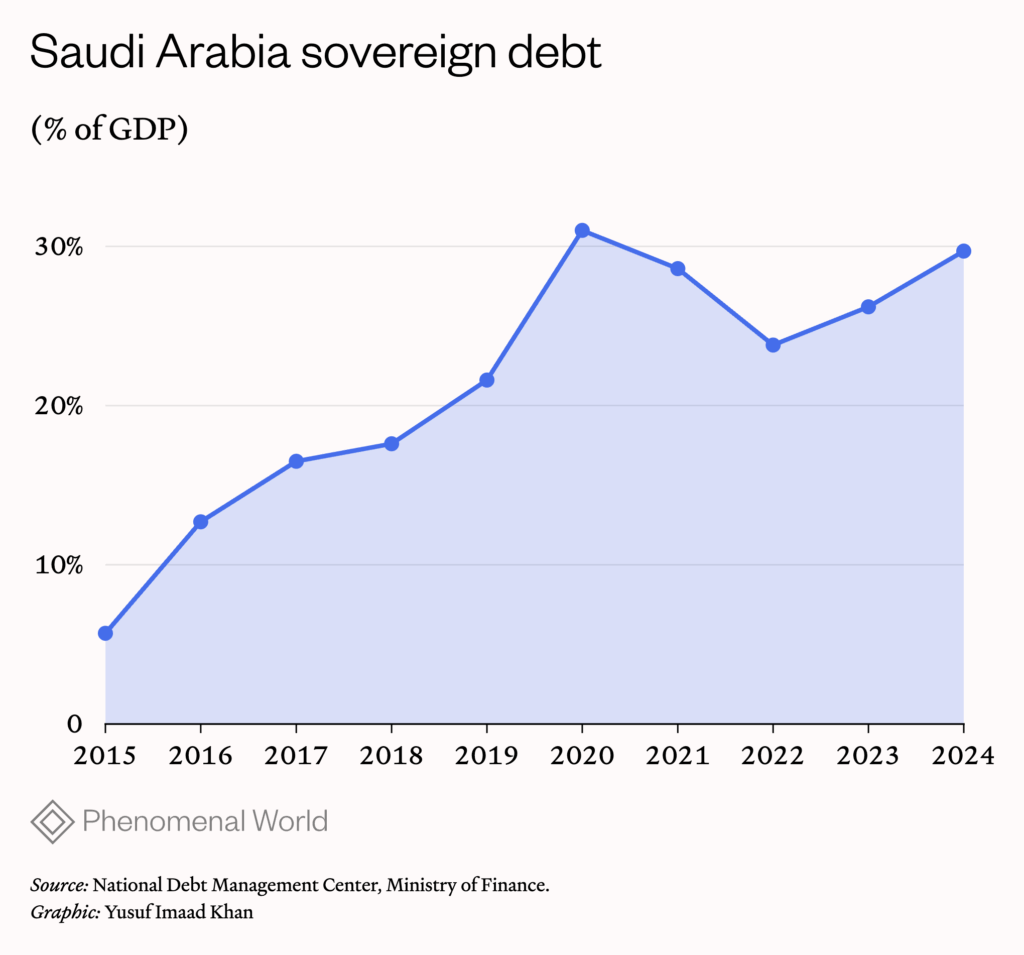

Secondly, SV2030 is scaling the use of leverage to unprecedented levels. Even though state and country are far from pressing against debt sustainability-related concerns—the S&P rating attests as much, as does interest expenses absorbing only 3.6 percent of budgetary resources—in relative and nominal terms, the magnitude of external debts has created obligations of meaningful consequence.46Stephane Alby, “EcoPerspectives 1(<)sup(>)st(<)/sup(>) Quarter 2025: Saudi Arabia”, BNP Paribas (January 2025)

Thirdly, the SV2030 build is diversifying the financial channels and institutions connecting Saudi Arabia and the rest of the world. Via sovereign bond issuance, all the major global book runners have been brought into the fold—the likes of HSBC, JP Morgan, Standard Chartered, Citi, Bank of China, Mizuho Financial Group, Goldman Sachs and BNP Paribas.47Matt Smith, “Saudi Arabia leads international bond issuance”, (<)em(>)Arab Gulf Business Insight (<)/em(>)(September 5, 2024) Via the buyers targeted by the bond’s primary dealers, all the usual asset and index fund managers have been staked in Saudi as well. The borrowing of domestic commercial banks, meanwhile, alongside private lending arrangements organized by the PIF, are tying banks from across the world’s largest financial centers to the construction bonanza. In certain instances, local banking affiliates, like HSBC’s Saudi British Bank and Credit Agricole’s Banque Saudi Fransi, position foreign financial institutions more directly in the fray.

Equity acquisitions on public exchanges—both in Saudi and on foreign stock markets—grants access to others: Foreign holdings in major developers like Dar al Arkan (and its mother company) connect many international investment houses to SV2030.48Nirmal Narayanan, “Foreign investments surge in Saudi stocks, reaching $1.02 bn in September”, (<)em(>)Arab News (<)/em(>)(October 9, 2024); For a general sense of scale, foreign investors held Saudi equities worth roughly USD 110 billion as of last fall; non-GCC foreign owners are estimated to control 12% of the Saudi Exchange. Regulations that had previously obstructed foreign investment into real estate in Mecca and Medina have been recently lifted, suggesting that the equity channel will soon bring in more foreign capitals.49Staff Writer, “Saudi Arabia allows foreigners to invest in firms with property in Mecca, Medina”, (<)em(>)Reuters (<)/em(>)(January 27, 2025). Smaller deals have integrated lesser creditors into the financial wiring of SV2030, public institutions included. Consider Italy’s state export credit agency SACE issuing loan guarantees worth $3 billion for the Neom Giga Project this past January.50Staff Writer, “Saudi Arabia’s PIF signs $3 billion agreement with Italian export credit agency”,(<)em(>) Reuters (<)/em(>)(March 5, 2025).

Viewed in its totality, the financial circuitry behind SV2030 has substantially changed the Saudi state and economy’s relation with the world around it. To extents never seen before, a host of foreign capitals have taken direct positions in the profits being scrounged from the country’s built environment. Through the sinews of debt, the integration of Saudi within global financial markets has also deepened.

Contracting arrangements have likewise shifted the Saudi state’s relation to foreign capitals. Multinationals from near and far are on the ground today working on hundreds of ongoing projects. The laying of the Riyadh Metro alone brought in everyone from the United States’ Bechtel to Germany’s Siemens to France’s Alstom and Avant Premiere, Italy’s Webuild, Spain’s FCC, and Korea’s Samsung. A brief survey of the wider web of infrastructure and real estate builds reveals the scale of this global constellation.

Select List of Foreign Partners Involved in SV2030

| FIRM | COUNTRY | PROJECT |

|---|---|---|

| WeBuild | Italy | Neom: Joint venture with Sajco for high-speed train line |

| WeBuild | Italy | Trojena Dam Project |

| PowerChina | China | Neom |

| Baosteel | China | Joint venture with Aramco and PIF |

| China State Construction Engineering Corporation | China | Join venture with Diriyah Company and El Seif Engineering Contracting Co. |

| China Energy Engineering Corp | China | Photovoltaic (PV) project |

| Jinka Solar | China | Joint venture: PV module project |

| Bauer Group | Germany | Neom: Foundation |

| Kent | United Kingdom | Joint venture with Nesma & Partners (engineering and procurement) |

| Aecom | United States | Neom: Infrastructure and Geotechnical Support |

| Jacobs Engineering | United States | Neom: Construction Advisory |

| Air Products | United States | Neom: Joint venture with ACWA power for green hydrogen ammonia production |

| Kolin Construction | Turkey | Trojena infrastructure |

| Samsung | South Korea | Join venture with al Rushaid Petroleum Investment Company (construction technologies) |

| FCC | Spain | Riyadh Metro |

| Hill International, Italferr, Sener, Chinese Engineering Construction Company | United States, Italy, Spain China | Land Bridge Riyadh-Jeddah |

| Orascom Construction, Hassan Allam Construction, Talaat Moustafa Group | Egypt | Partnerships with National Housing Company |

Some foreign companies have independently won contracts. Others have been integrated into the build via joint ventures with either private or state-owned firms. At a juncture marked by stagnation in Europe and crisis-adjacency in much of west Asia, this means that the structure of balance sheets and prospects for profitability for many firms are hinging on opportunities in the (re)construction of Saudi Arabia.

At the same time, various measures like surety bonds, upskilling projects, and supports for supply chain integration are in place to boost smaller, local businesses in Saudi Arabia.51Reina Takla, Nirmal Narayanan, “Saudi Arabia launches new financing products to boost construction sector”, (<)em(>)Arab News (<)/em(>)(February 14, 2025). Whether with policymaker intent or not, SV2030 is also allowing low-level brokers in the market for construction labor to cash in. Exploiting loopholes pertaining to Saudiization quotas (and taking advantage of citizenship-coded distinctions in legal rights), tassatur entrepreneurs are today collecting sizable rents on the deployment of non-nationals to construction sites.52Anita Hammer and Ayman Adham, “Mobility power, state and the ‘sponsored labour regime’ in Saudi capitalism”, (<)em(>)Work, Employment and Society (<)/em(>)37:6 (2023). For Saudi Arabia’s relatively few though exceedingly well-endowed savers, the country’s equity markets furnish an indirect way to make a de facto state-backed buck on SV2030 as well. Those with holdings in the country’s commercial banks, the primary lenders to the build, are reaping the rewards of record earnings—up 14 percent in 2024, the sector’s net profits topped SAR 80 billion, or $21.33 billion.53Anton Lopatin and Redmond Ramsdale, “Saudi bank earnings aided by lower interest rates, despite liquidity tightening”, Non-rating Action Commentary: FitchRatings (March 10, 2025). With dividend-payout ratios of 50 percent and attendant rises in valuations, it is a good moment for holders of banking stocks.54Zeina Nasreddine and Mohamed Damak, “Saudi Arabia Banking Sector Outlook 2025: Vision 2030 Momentum Continues”, Report: S&P Global Ratings (January 2025). Anyone carving out positions in the country’s many publicly traded real estate investment trusts (REITs), or in her major construction material producers, is also collecting sizable dividend payments.55Dividend schedules are available at: <(<)a href='https://www.saudiexchange.sa/wps/portal/saudiexchange/newsandreports/issuer-financial-calendars/dividends/!ut/p/z0/04_Sj9CPykssy0xPLMnMz0vMAfIjo8ziTR3NDIw8LAz8LTw8zA0C3bw9LTyDvAwMAoz1g1Pz9AuyHRUBMfE6EQ!!/'(>)https://www.saudiexchange.sa/wps/portal/saudiexchange/newsandreports/issuer-financial-calendars/dividends/!ut/p/z0/04_Sj9CPykssy0xPLMnMz0vMAfIjo8ziTR3NDIw8LAz8LTw8zA0C3bw9LTyDvAwMAoz1g1Pz9AuyHRUBMfE6EQ!!/(<)/a(>)

The big money is accruing to the players with major positions in the financing of the SV2030 construction boom—and to those who control firms benefiting from procurement, project contracting, and (partial or full) PIF incorporation. The leading scions of the banking sector—representatives of the al Rajhi, Olayan, al Sharbatly, al Muhaidib, al Jarallah, al Subeaei, al Mojel, al Zamil, and al Issa families, among others—are flying high. Through holding companies and multisector conglomerates, many of these same persons double dip via construction. There, SV2030 contracting combined with VAT exemptions for real estate activities and the state’s provision of an exceedingly vulnerable workforce allows these companies to mint enormous fortunes. The Royal Institution of Chartered Surveyors’ estimates Saudi construction firms as a population are currently enjoying profit margins in excess of 60 percent.56Staff Writer, “Saudi Arabia’s Construction Sector: A Gateway to Unprecedented Opportunities”, R Consultancy Group: Linkedin post (April 3, 2024). For those operating further afield, incorporation within the PIF has helped turn already strong privately-owned firms into national champions. Such has been the experience for developers Almabani General Contractors and AlBawani Holding Co. as well as energy giant Acwa Power and Hadeed and Rajhi Steel, among others.

A new sociology of housing

The Housing Program of SV2030, which defined 70 percent home ownership by 2030 as its primary objective, emerged from this series of political, financial, and commercial undertakings. As construction continues on a massive scale, winners are already being sorted from losers. Those fortunate enough to already hold property in Riyadh, for instance, have enjoyed substantial appreciations in rent streams and asset values, while the gentry in secondary cities like Jeddah and Dammam are having less luck.57Taking 2024 as an example, property values appreciated in Riyadh by nearly 10% in Riyadh versus just 1 percent in Jeddah and Dammam. See: Oliver Morgan, Mohamed Mousa, Manika Dhama, “Middle East Real Estate Predictions 2025: KSA Market Review”, Report: Deloitte (January 2025); CBRE Research, “Saudi Arabia Real Estate Market Review Q2 2024”, Report: CBRE (August 2024). On the developers’ side, only banks able to leverage mergers and debt flows into larger balance sheets are riding a profit wave powered by mortgage lending and lending to the construction and real estate sectors.58International Monetary Fund, “Financial Sector Assessment Program: Saudi Arabia”, Country Report no.2024/281 (2024). Residents of areas designated for certain luxury redevelopments—like the 500,000–1,000,000 persons evicted from neighborhoods surrounding the old town of Jeddah—have lost their homes. Those acquiring land and property through the state’s eminent domain declarations, alternatively, have very much gotten something for nothing.59See: Staff writer, “Saudi Arabia: ‘Unfathomable’ Jeddah demolitions uproot hundreds of thousands”, (<)em(>)Middle East Eye (<)/em(>)(January 28, 2022); Staff writers, “The Dark Side of Neom: Expropriation, expulsion and prosecution of the region’s inhabitants”, Report: ALQST for Human Rights (February 2023).

Working toward SV2030’s home ownership objectives on the demand side, the Central Bank increased the maximum loan-to-value ratio for first time buyers from 85 to 90 percent in 2018. More significantly, perhaps, the Ministry of Finance capitalized the Real Estate Development Fund (REDF) to directly support home buyers, by covering VAT payments for first time home buyers and subsidizing a share of their down payments and mortgage loans. Via its fully-owned Saudi Mortgage Guarantees Services Company, the REDF also extends mortgage guarantees and other insurance-type policies to reduce lender risk. Through these mechanisms, the institution has subsidized seven out of ten outstanding mortgages. Its efforts were critical in juicing the commercial banking sector’s staggering increase in retail mortgage lending. From 2016 through the pandemic years, the data shows the extension of credit to home buyers leaping at a remarkable clip. After witnessing a slight lull in 2022 and 2023, the volume of lending bumped back up again near historic highs in 2024. All in all, the stock of retail mortgage loans on the balance sheets of Saudi commercial banks grew more than 600 percent during the years in question.

On the supply side, loan guarantees for developers, taxes introduced on vacant land, and a handful of targeted measures attempted to address matters of affordability. The Development Housing Initiative conveys state subsidies to contractors working on low income housing builds. The NHC is now pledging to price its units 20 percent below market rates as well.60Nadin Hassan, “Saudi Arabia’s NHC to offer affordable homes 20% below market rates, CEO says”, (<)em(>)Arab News (<)/em(>)(January 28, 2025). Arguably most central to SV2030’s supply strategy are an assortment of initiatives—many led by the SRC—aimed at turning homes into liquid financial assets. The SRC and Hassana Investment Company—an investment arm of Saudi Arabia’s social security and pension fund—are currently developing a market for mortgage-backed securities, with the technical support of Blackrock and King Street Capital.

The SRC’s recent acquisitions of commercial banks’ mortgage portfolios—purchases that also have the effect of freeing up those banks’ balance sheets—have contributed to this securitization process.61Staff Writer, “SNB offloads SAR 3.4 bn mortgage portfolio to Saudi Real Estate Refinance”, (<)em(>)Enterprise Saudi Arabia (<)/em(>)(March 1, 2025). It is expected these portfolios will shortly be cut and bundled into tradable securities.62Adelaide Changole, “Saudi Arabia Taps BlackRock to Build Mortgage-Backed Securities Market”, (<)em(>)Bloomberg (<)/em(>)(October 23, 2024). The assetization of housing has further been advanced through the Capital Market Authority’s October 2016 approval of regulations for REITs. In the years since, sixteen REITs have been established and listed on the Saudi stock exchange, offering domestic and international investors indirect exposure to the housing market. Notably, the largest REITs are run by the investment house of the al Rajhi family and by Jadwa Investments, respectively. The latter is the firm where the Crown Prince cut his teeth in the early 2010s.

This collection of policies has lifted the home ownership rate for Saudi nationals into an estimated range of 62–65 percent.63International Monetary Fund, “Financial Sector Assessment Program” (2024): 12. Valentina Pasquali, “Saudi Arabia wows US investors to bolster housing sector”, (<)em(>)Arab Gulf Business Insight (<)/em(>)(September 9, 2024). But the state is incurring both a fiscal burden and contingent liabilities. Even more significant are effects rendered through growing household indebtedness. For those who have managed to join the ranks of property owners post-SV2030, the combination of rising home valuations and high interest rates (even after state subsidies) pushed debt levels into relatively dangerous territory. Presently, debt-service-to-income ratios are averaging out at around 40 percent.64International Monetary Fund (2024). Such repayment obligations leave little budgetary margin, and scarcely little capacity for shock absorption.

The pressure is heightened by the fact that most Saudi households have little savings. Figures from 2018, the latest available, document an average savings ratio of 1.6 percent annual disposal income, with 45 percent of Saudis reporting no savings at all. With real wage growth flat in the intervening years and the cost of living increasing substantially—the latter reality reflected in households’ growing reliance on debt when it comes to financing not only major expenditures like automobiles and education, but day-to-day consumption—it is probable that the 1.6 percent ratio is even lower today. 65On disposable income growth since 2018, see: Staff Writers, “The Saudi Report: Part One”, Report: Knight Frank (2024). Also see: Alotaibi Mohamed Meteb, “The conspicuous consumption phenomenon in Saudi Arabia”,(<)em(>) Prague Economic Papers(<)/em(>) 33:6 (2024).Ibrahim Tawfeeq Alsedrah, “Determinants of the personal savings rate in the Kingdom of Saudi Arabia using time saving deposits”, (<)em(>)Heliyon (<)/em(>)10:3 (February 2024); Dayan Abou Tine, “Saudi Arabia records 16% surge in credit card loans in Q1 2024”, (<)em(>)Arab News (<)/em(>)(May 9, 2024); Staff Writer, “Consumer lending made easy through open banking”, Blog: Tarabut.com (June 7, 2023). This all amounts to new property-owning families assuming unprecedented degrees of risk via the housing transition. For many, securing the present requires that their job be retained no matter what. Securing the future, meanwhile, hinges at least partially on their home appreciating in value.

New housing construction has also created a disjuncture between the kinds of properties coming to market and the kinds that are needed to actually grow ownership ranks.66The average four bedroom villa in Riyadh is currently priced at SAR 2.8 million (or approximately $700,000). A majority of the one million new units estimated to come to market between now and 2030, meanwhile, are expected to be priced north of $1 million. Knight Frank (2024): 40 Housing budgets for 70 percent of Saudi nationals are below the price of the average villa in Riyadh.67Ibid. According to the IMF, 80 percent of retail borrowers are government employees. The state’s fiscal consolidation efforts have focused on reducing the headcount of the civil service—an agenda pursued through in part through golden handshake arrangements with employees but primarily through hiring freezes.68Nadim Kawach, “Saudi Arabia plans cash pay-offs to cut public sector jobs”, (<)em(>)Arab Gulf Business Insight (<)/em(>)(January 13, 2025); International Monetary Fund, “Staff Report: Saudi Arabia Article IV Consultation”, (September 2024). This lending pattern thus reveals the exclusion of younger generations from the property market.69 There are certainly exceptions to the trend. Family wealth affords a workaround for some.(<)sup(>) (<)/sup(>)Education-mediated wage differentials are also allowing a relatively slim fraction of the younger workers in the private sector to become viable borrowers.(<)sup(>) (<)/sup(>)See Knight Frank (2024) and IMF, “Article IV Consultation): 48.

Private sector employment opportunities from SV2030 are concentrated in low productivity industries like construction, wholesale and retail commercial services, and hospitality. For most young people navigating this labor market, and especially women, the implication is a confluence of weak earning potential and low levels of income mobility. With rents rising in most urban centers, non-extant savings—an average of 2 percent for those between twenty-six and twenty-nine years of age, 4 percent for those thirty to thirty-four, and -4 percent for those thirty-six to thirty-nine—are thereby baked in. The odds of becoming a homeowner are slim. With house prices up 81 percent and apartment prices up 56 percent since 2020 in Riyadh, exclusion from asset ownership is tantamount to falling hopelessly behind.

The Saudi model

Since large imports of non-citizen labor into Saudi Arabia began in the 1960s, the local expression of class was mediated by nationality and, per Adam Hanieh, spatialization.70For a full consideration of spatialization, see: Adam Hanieh, “Temporary migrant labour and the spatial structuring of class in the Gulf Cooperation Council”, (<)em(>)Spectrum: Journal of Global Studies (<)/em(>)2:1 (2010). Foreign workers, subject to intensive exploitation and discretionary deportation, at once underpinned capital accumulation and served as a social release valve in times of crisis. While spatialization continues to serve as an organizing principle for Saudi society and Saudi capitalism, SV2030 has changed how class acts on the citizen-national population. In the past, social divisions amongst citizen nationals had been flattened to a non-insignificant degree through public policy. While politics, religion, gender and geography bequeathed profound inequalities, public sector employment and the extension of subsidies and other forms of transfers nevertheless consolidated a broad middle class.

In our present juncture, these flattening measures are being gradually withdrawn and indeed reversed. Asset ownership, rather than a state job and the income it confers, increasingly arbitrates class positioning. In some ways, this is a continuation of a trend initially powered by a mid-2000s collapse in labor income: Between 2007 and 2018, average household income increased by just 5.3 percent, or less than 0.5 percent per annum, despite average household expenditures growing by 38 percent during the same period.71KPMG (2020): 3 The current moment is novel, though, in that stagnation in labor earnings endures amidst an SV2030-driven spike in asset prices. The divergence closely resembles ones observed in the United States, United Kingdom, and Australia.72See: Lisa Adkins, Melinda Cooper, and Martijn Konings, “Class in the 21(<)sup(>)st(<)/sup(>) century: Asset inflation and the new logic of inequality”, (<)em(>)Economy and Space (<)/em(>)53:3 (2021). In these societies, capital gains, capital income, and intergenerational wealth transfers have crystallized as the syntax of class. The juxtaposition in Saudi Arabia between a post–2021 decline in real wages for Saudi nationals and a post–2021 boom in housing valuations suggests the country is on the same track.73IMF, “Article IV Consultation” (2024): 73

Mohammed bin Salman’s Saudi Arabia harnesses growth to fixed capital formation and embraces the state as planner and market actor. But it does so through the financialization of housing and debt-financed consumption. The result is a super-powered state without the requisite competence: land filled with structures and infrastructure that provide economic utility only during their construction; a cronyism different in form but not kind from the iteration which preceded it; an increasingly debt-addled consumer society; a labor market generating demand primarily in low end services; and a housing market charged by risk, speculation, and exclusion. Though SV2030 may craft a more viable path to long-term growth, the proposition that it will carve one to social peace is dubious. A mix of carnival and repression may suffice to keep the country’s politics stable. But a great deal of pain, resentment, and deprivation will fester beneath the surface.

Further Reading

Egyptian Leverage

The IMF invests in the Egyptian dictatorship’s structural payments imbalance

Normalization and the Future of the Middle East

An interview with Elham Fakhro on the Abraham Accords

Built Trades

Employer claims of unavailable labor are rooted in an unwillingness to raise wages and the long-term decline of the nation’s system of training and allocating labor

Further Reading

Egyptian Leverage

The IMF invests in the Egyptian dictatorship’s structural payments imbalance

Cairo’s role in a US-backed regional security architecture makes the military dictatorship a regional giant too big to fail. The Sisi regime, like its predecessors,...

Normalization and the Future of the Middle East

An interview with Elham Fakhro on the Abraham Accords

Before October 7, 2023, the pursuit of diplomatic and economic normalization between Israel and Arab states appeared to be the central trajectory for regional politics...

Built Trades

Employer claims of unavailable labor are rooted in an unwillingness to raise wages and the long-term decline of the nation’s system of training and allocating labor

As the American economy reopened in the first half of 2021, reports of a “labor shortage” spread throughout US industries. But there was one sector...