May 23, 2025

Analysis

The Tariff Threat

Mexico's fragile supply chains and North American trade policy

In a dramatic shift in US trade policy, the Trump administration has imposed and continues to threaten new rounds of tariffs against Mexico, sounding alarm bells across the Mexican manufacturing industry. If fully implemented, these measures could cause immediate disruption in key industrial zones, place hundreds of thousands of jobs at risk, and halt strategic investments.

Whatever Trump’s motivations around migration, security, or a new model of trade integration, the threat reveals a deeper structural vulnerability in Mexico’s economy: an excessive dependence on a single trading partner, one which is now willing to use tariffs as a political tool. This instrumental use of economic power has direct consequences for the stability of the Mexican economy and the functioning of highly integrated value chains between the two countries.

A clear example of this politicization of trade is the recent dispute over the 1944 Water Treaty. On April 10, less than a week after new tariffs announced during so-called “Liberation Day” came into effect, President Trump accused Mexico of “stealing water from Texas farmers” and threatened to immediately impose an additional 10 percent tariff on all Mexican imports, along with targeted economic sanctions. This episode illustrated how the arbitrary and political use of tariffs can generate profound uncertainty around bilateral trade secured by agreements signed decades ago.

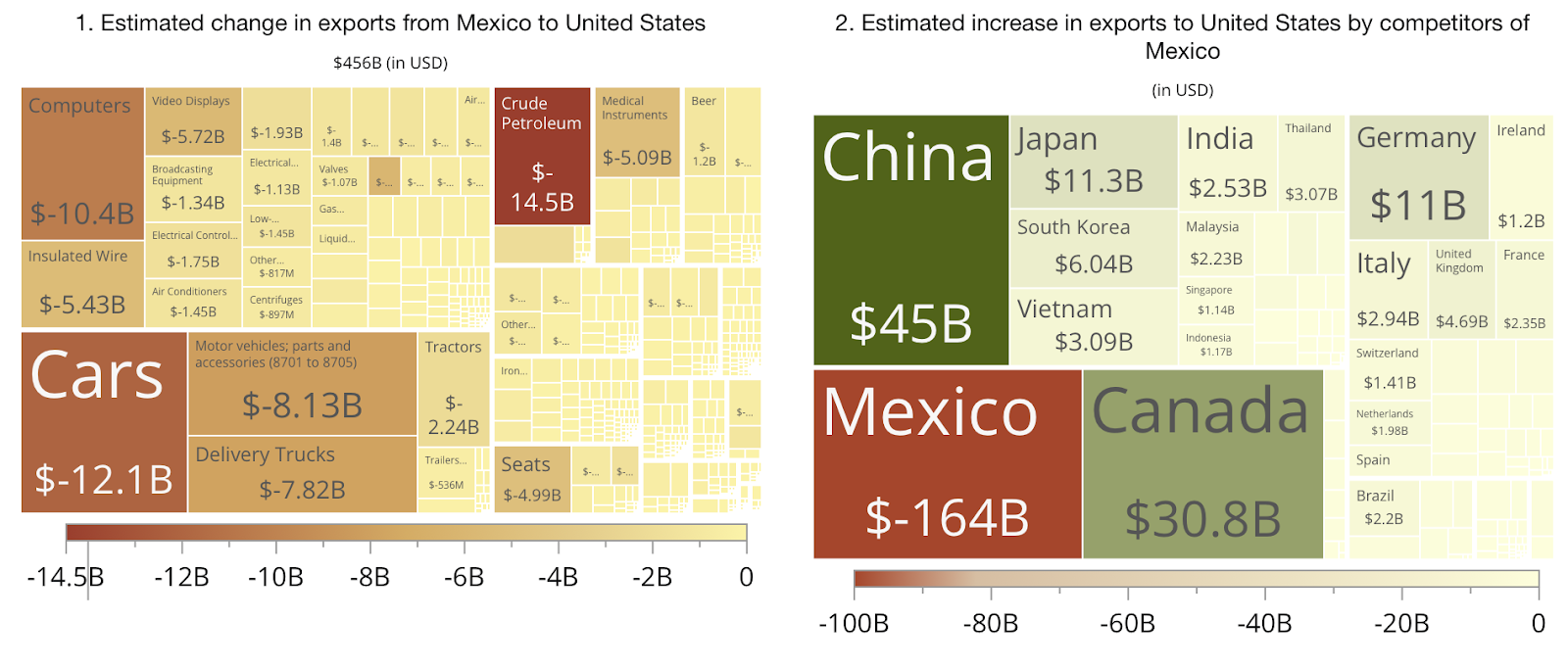

In 2024, Mexico exported a record $495 billion to the United States—equivalent to almost 30 percent of national GDP—mainly concentrated in complex manufactures such as vehicles, auto parts, and electronic products. This industrial success, however, implies a critical exposure: unilateral decisions in Washington are enough to cause, almost immediately, a partial paralysis of the national productive apparatus.

Simulations by the Observatory of Economic Complexity (OEC) estimate that a 25 percent tariff could reduce Mexican exports by up to $164 billion annually over three years—a figure equivalent to Mexico’s total exports to countries outside the United States.1Viktor Stojkoski, Pablo Paladino, Jelmy Hermosilla, and César A. Hidalgo. The OEC Tariff Simulator (2025). https://oec.world/en/tariff-simulator?exporter=mex&tariff=25 The impact would be especially severe in industrial regions with a high concentration of exports, where employment is directly dependent on the stability of binational trade.

Faced with this scenario, Mexico must avoid the false choice between deepening regional integration and seeking new markets. The only viable strategy is twofold: Mexico can intelligently strengthen economic ties with the United States in key sectors, while accelerating technological and geographic diversification to reduce vulnerabilities, scale its own capabilities, and expand the country’s strategic margin in the face of future disruptions. This is the only way to transform a critical exposure into a more autonomous, complex, and sustainable growth architecture—and avoid being trapped in a precarious integration model, vulnerable to unilateral decisions and increasingly incompatible with an unstable geopolitical environment.

From growth to limits

Productive integration with the United States has been the main driver of Mexico’s manufacturing growth over the past three decades. The automotive, electronics, and industrial machinery sectors have prospered thanks to geographical proximity to the US, trade agreements, and growing regional specialization. But the same process that allowed Mexico to climb up global value chains has also left it vulnerable. As competitive advantages were consolidated, risks were also concentrated. Today, a large part of the national productive apparatus depends on external rules, decisions, and conditions over which Mexico has less and less control. The paradox is clear: the more integrated the Mexican economy, the more exposed it is to disruptions originating outside Mexico’s borders.

In 2024, Mexico exported more than 2.8 million light vehicles to the United States, reaching a 15 percent share of the US market.2Annalisa Villa, “European car makers’ body warns US tariffs threaten domestic production, exports,” (<)em(>)S&P Global(<)/em(>) (March 27, 2025) https://www.spglobal.com/commodity-insights/en/news-research/latest-news/metals/032725-european-car-makers-body-warns-us-tariffs-threaten-domestic-production-exports Behind this figure lies a complex network of assembly plants and suppliers distributed on both sides of the border, relying heavily on critical imported components, especially batteries, advanced sensors, and semiconductors from Asia and the US. This fragmented architecture, while efficient under normal conditions, multiplies logistical costs and exposes the industry to immediate disruption when tariffs or technological restrictions are introduced.

An emblematic case is the Tesla gigafactory announced in Nuevo León in 2023. With an estimated investment of more than $10 billion and the projected creation of 12,000 direct jobs, this plant is emerging as a strategic node in the North American electric vehicle (EV) chain.3Forbes Staff, “Nuevo Leon approves $2.627 billion pesos in incentives for Tesla factory,” (<)em(>)Forbes(<)/em(>) (December 14, 2023). https://forbes.com.mx/nuevo-leon-aprueba-2627-mdp-en-incentivos-para-fabrica-de-tesla Under tariffs, however, its operation could become unviable, making the supply chain more expensive and inhibiting new investments of a similar scale.

The case of Ciudad Juarez illustrates the scope of this vulnerability. The border city is home to more than 300 export-oriented manufacturing plants, many of them integrated into electronics, auto parts, and medical device value chains.4INDEX. Juarez, Consejo Nacional de la Industria Maquiladora y Manufacturera de Exportación, (<)em(>)Economic and Industrial Bulletin of the Maquiladora Industry(<)/em(>) (2023) An abrupt disruption of trade would have immediate effects on formal employment, local consumption, and state tax revenues. Other industrial regions—from Reynosa to Querétaro—face similar conditions of critical exposure, relying almost exclusively on fluid access to the US market.

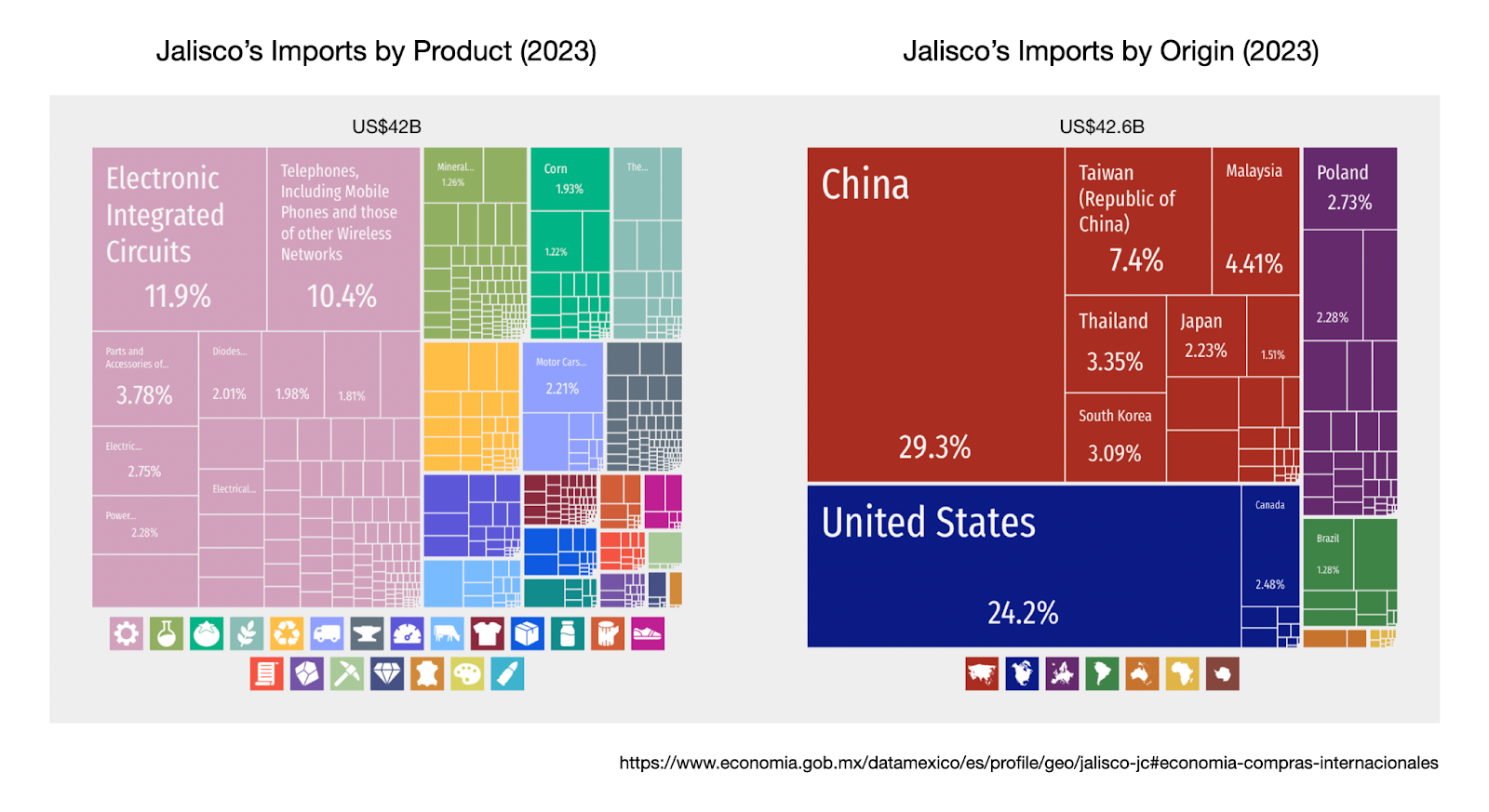

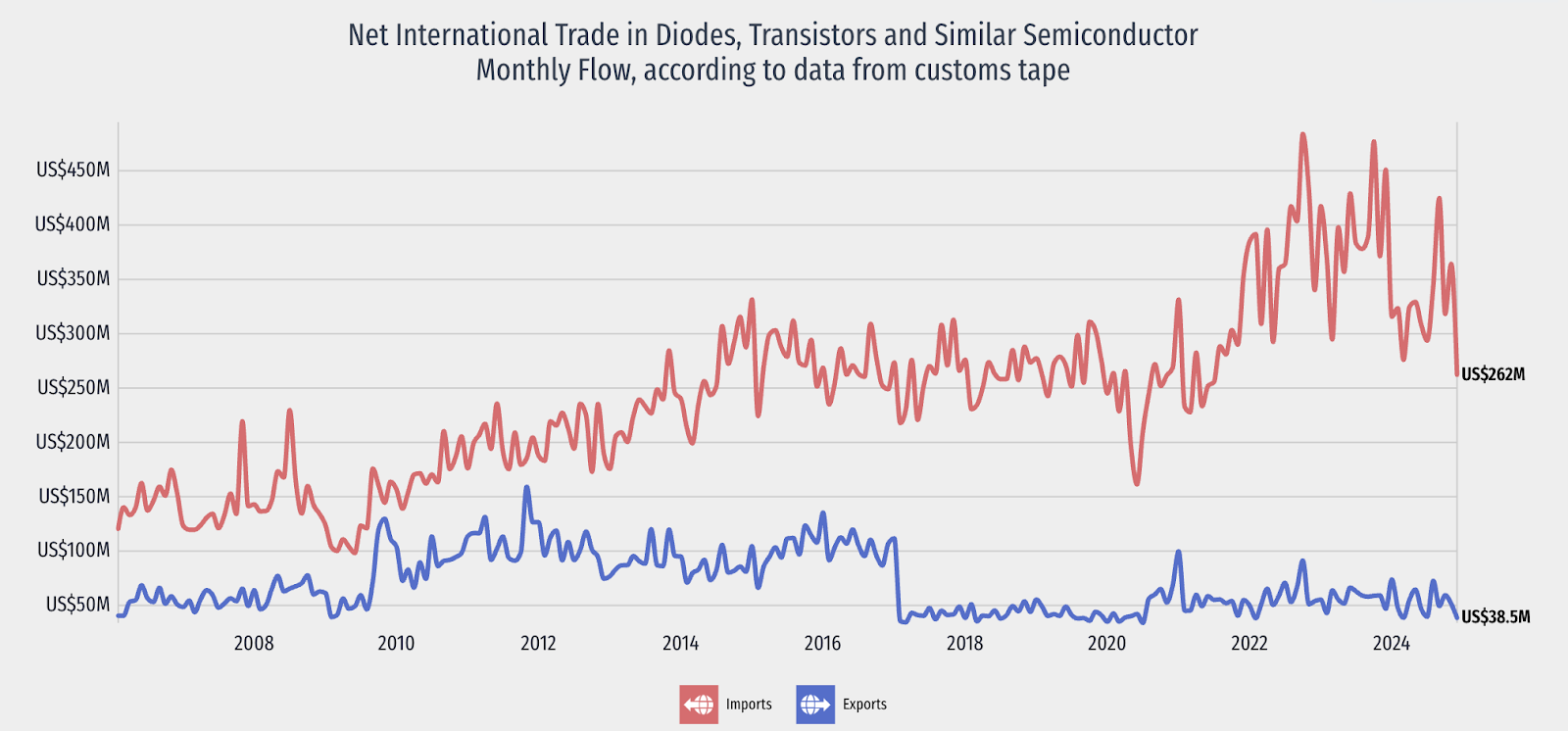

The electronics industry in Jalisco represents another dimension of this dependence. With accumulated investments of over $4.5 billion in the last fifteen years and more than 100,000 specialized jobs, this region has consolidated itself as a key technological pole in Mexico.5Patricia Romo, “Jalisco is confirmed as Silicon Valley and chip capital in Latin America,” (<)em(>)El Economista(<)/em(>) (May 11, 2024) https://www.eleconomista.com.mx/estados/jalisco-confirma-silicon-valley-y-capital-chips-america-latina-20241105-733019.html However, more than 80 percent of the semiconductors it uses are imported from Asia. During the global chip crisis of 2021–2022, this dependence caused losses of more than $400 million in just six months, highlighting the limits of integration without local capabilities in high-tech components.

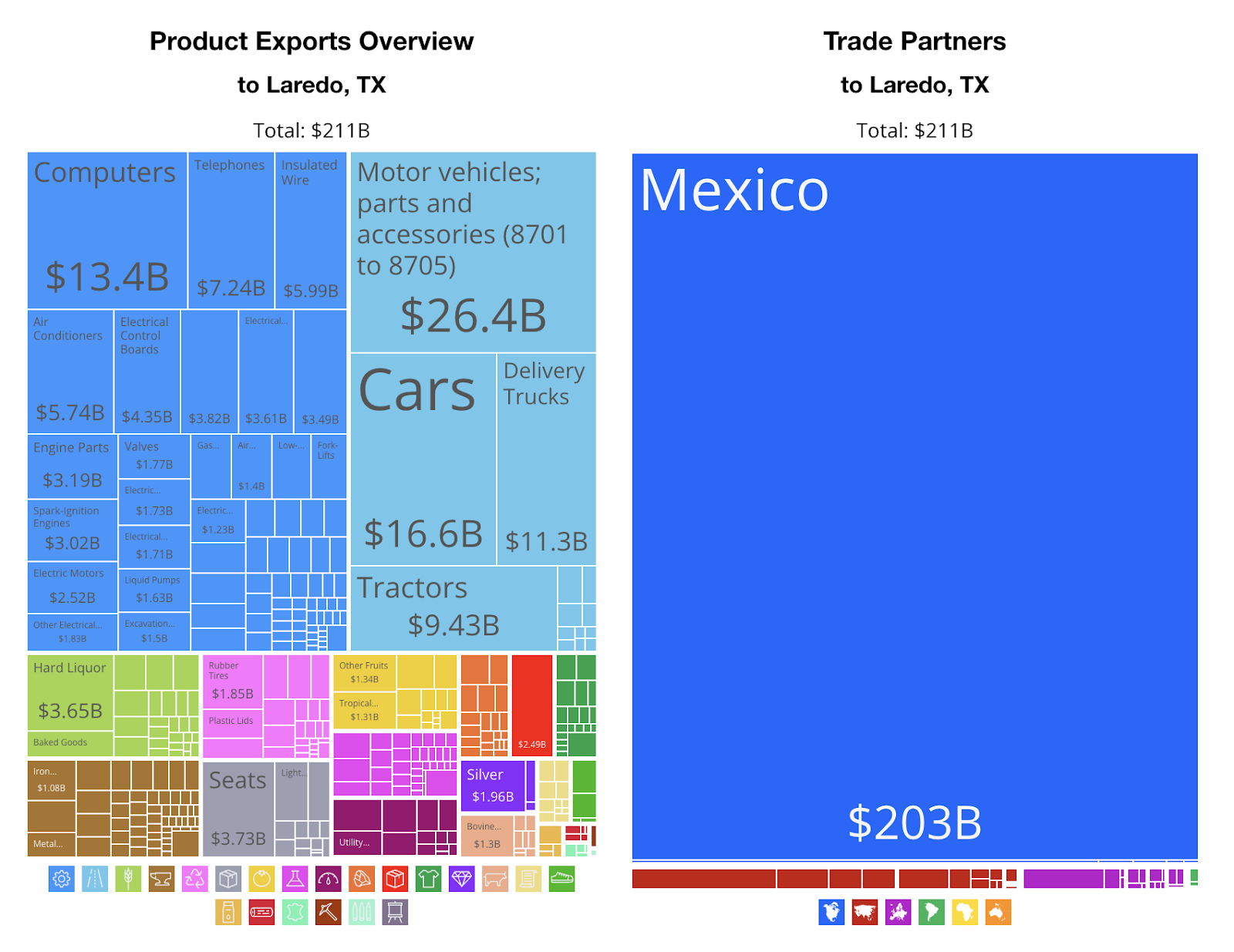

This structural vulnerability is compounded by a logistical bottleneck that amplifies risks. The Laredo-Nuevo Laredo border crossing concentrates close to 40 percent of land trade between Mexico and the United States—more than $211 billion annually—but operates with overloaded infrastructure and slow customs processes. This saturation generates cost overruns estimated at more than $3.5 billion per year, affecting the operational efficiency of key sectors such as automotive, electronics, and medical devices.6Nuevo Laredo Institute for Competitiveness and Foreign Trade (ICCE). (2022). Binational Socioeconomic Forecast 2022. Nuevo Laredo, Tamaulipas, Mexico. Retrieved from https://anyflip.com/ivqr/ygor/

The current model of integration, based on efficiency and scale, has been successful in terms of export growth, but its limits are becoming increasingly evident. Without greater technological autonomy, a more robust supplier base and modern infrastructure, this scheme is vulnerable to external shocks. In a geopolitical environment marked by uncertainty and unilateral decisions, persisting in this dependence without strategic adjustments compromises the Mexican state’s ability to protect its industrial base and guide its economic development with sovereignty.

One strategy, two fronts

Mexico’s growing exposure to unilateral trade decisions has made it clear that sustaining current integration is not enough: a strategic reconfiguration is needed that recognizes its limits and capitalizes on its strengths. The country’s most dynamic sectors—automotive, electronics, and the medical industry—show both the potential of deep integration and its latent risks. The question is no longer whether Mexico should integrate or diversify, but how it can do both in an intelligent and complementary way. Exploring this dual path requires understanding which sectors represent consolidated advantages, which face critical bottlenecks, and where real platforms exist to reduce vulnerabilities without weakening what works.

This approach does not imply a break with the United States, but a qualitative transformation of the relationship. Mexico is not simply a low-cost supplier: it is a centerpiece of North American industrial competitiveness. What is at stake is not only maintaining access to the US market, but redefining the terms of integration through greater national technological content, internal innovation capabilities, and more resilient supply chains that can withstand external shocks without jeopardizing productive stability.

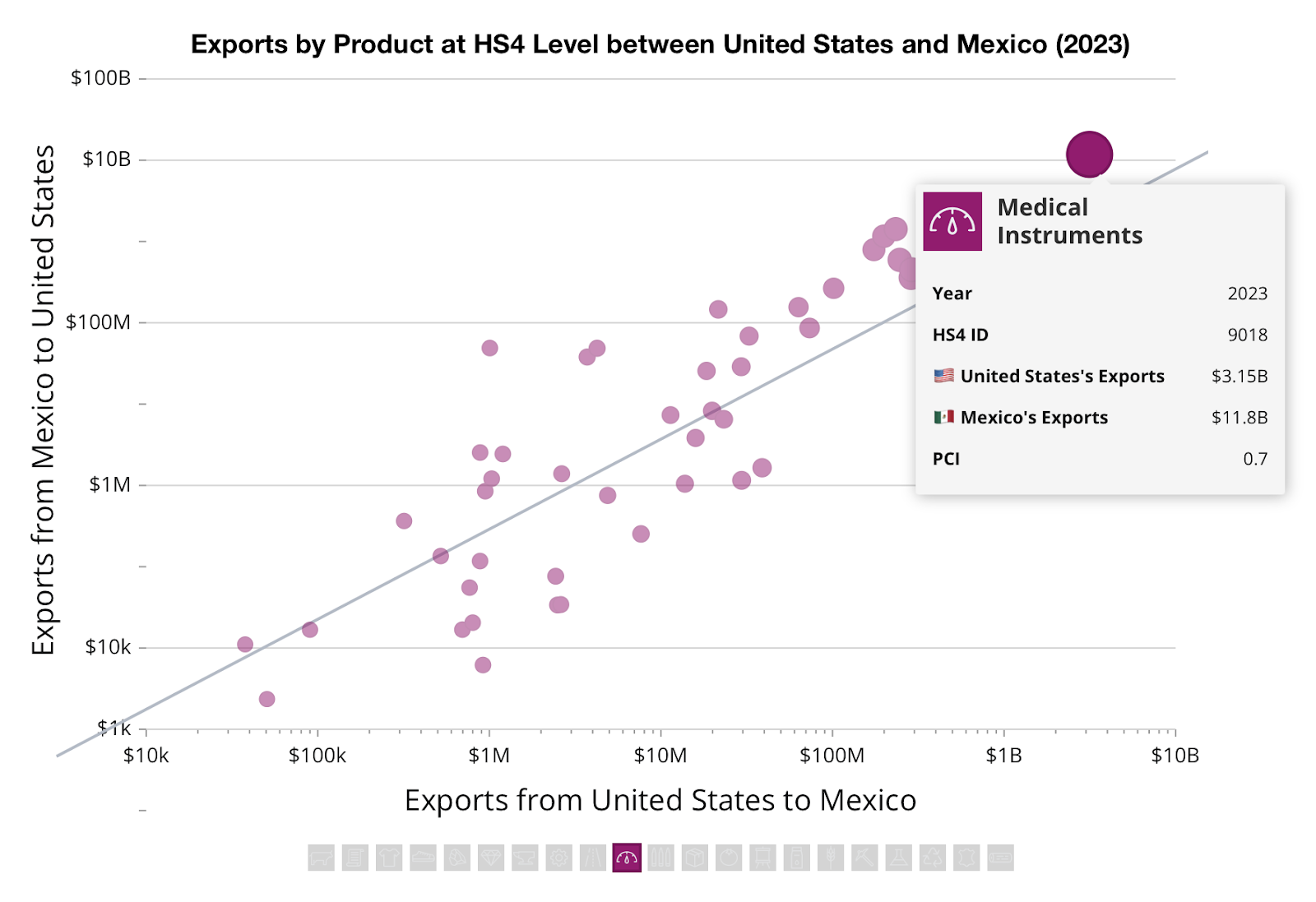

The medical device industry offers a concrete example of new-generation productive integration. In 2024, Mexico consolidated its position as the main supplier of these products to the US market, with exports over $12 billion and growth rates exceeding 25 percent annually. Companies such as Medtronic, Johnson & Johnson, and Abbott have built binational operations that combine manufacturing efficiency in Mexico with US-based regulations, design, and research and development capabilities. According to recent data, Mexico contributes 2.8 percent of domestic value added to US exports, compared to 1.8 percent for China and just 0.4 percent for Vietnam.7Pedro Casas and Arturo Martínez, “‘America First’ does not mean ‘America alone’,” (<)em(>)21st Century Diplomacy(<)/em(>), Wilson Center (February 3, 2025). https://diplomacy21-adelphi.wilsoncenter.org/article/america-first-does-not-mean-america-alone

This model reduces operating costs by up to 20 percent compared to Asian suppliers, while improving the speed of logistical response in a highly regulated sector.8National Academies of Sciences, Engineering, and Medicine, Health and Medicine Division, Board on Health Sciences Policy, Committee on Security of America’s Medical Product Supply Chain, “Globalization of U.S. medical product supply chains,” Chapter 3 in (<)em(>)Building resilience into the nation’s medical product supply chains(<)/em(>). Carolyn Shore, Lisa Brown, and Wallace J. Hopp (Eds.) National Academies Press (March 3, 2022). https://www.ncbi.nlm.nih.gov/books/NBK583730/ In addition, Mexican plants comply with demanding international standards (FDA, CE, ISO 13485), which allows them not only to supply the US, but also to compete in global markets. What is relevant is not only integration, but also their technological quality and their projection beyond North America.

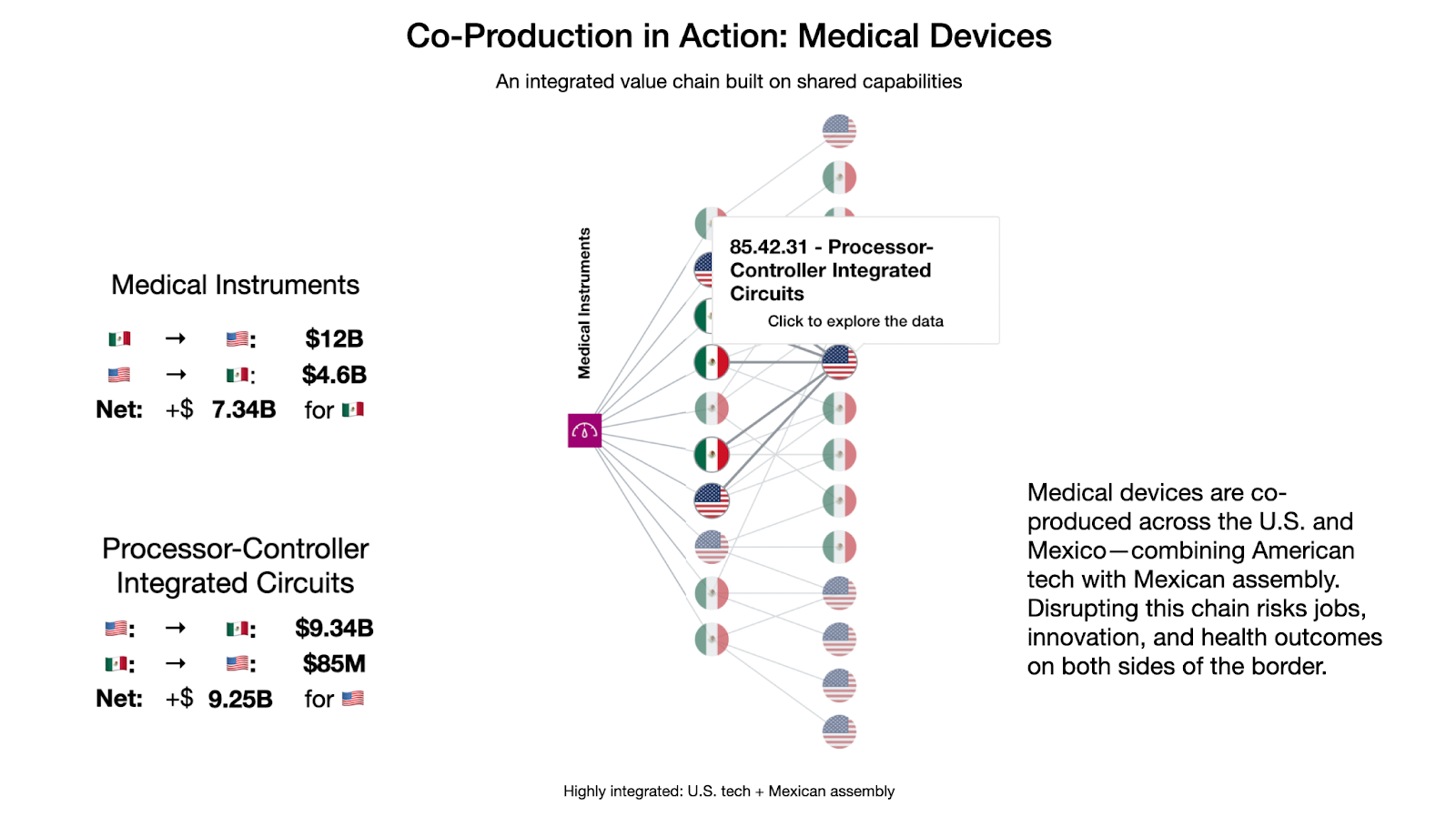

A detailed visualization of bilateral trade clearly shows how this interdependence operates. Mexico leads exports of finished medical devices to the United States, while relying on key inputs such as controller-type integrated circuits (HS 8542.31) from the same US market. In 2024, Mexico exported more than $12 billion worth of medical devices to the United States, which in turn shipped more than $9.3 billion worth of these components to Mexico. The result is neither a deficit nor a loss: it is a shared value chain, where one country designs and supplies the “brains,” and the other assembles, certifies, and delivers quality products ready for clinical use.

This model is not sustained by tariffs or nationalist speeches. It is sustained with clear rules, cross-border investment, and mutual trust. Fracturing this would not only jeopardize jobs and competitiveness, but would also weaken the health capacity of the entire region by disrupting a productive ecosystem that transcends borders and depends on deep coordination.

In 2024, Mexico exported more than $30 billion in auto parts to the United States, which represented more than 40 percent of the total imported by that country. However, this apparent leadership hides a structural weakness: the average national technological content barely exceeds 55 percent.9Ministry of Economy (2023). Diagnosis and Prospects of the Automotive Industry. Government of Mexico. Available at: https://www.gob.mx/se/documentos/diagnostico-y-prospectiva-de-la-industria-automotriz Many of the most sophisticated components—sensors, semiconductors, electronic modules—continue to be imported.

Sustaining this position in the supply chain requires more than volume: it requires a transition from assembly to value generation. This implies concrete instruments, such as tax incentives linked to a progressive increase in domestic content, technological co-investment schemes with anchor firms and technical training programs in key sectors. South Korea, in the 1980s and 1990s, adopted a similar strategy to move from intermediate supplier to industrial power. Mexico can adapt that experience to its own conditions.

The other pillar of the dual strategy is productive and commercial diversification with strategic direction. Mexico has already begun to receive relevant investments in emerging sectors such as EVs. A prominent example is BMW’s plant in San Luis Potosí, which will produce 140,000 battery packs per year starting in 2027.10BMW Group, “BMW Group increases production of electric vehicles in the global production network: the ‘NEUE KLASSE’ platform will also be built at the San Luis Potosi Plant” (2023) However, the country does not yet have an integrated production chain: it does not have the scale capacity to refine lithium, manufacture cells, or assemble complete systems.

Poland’s experience offers a useful roadmap. In less than a decade, the country created a competitive electric battery ecosystem, supported by three pillars: targeted tax incentives, specialized industrial parks in logistically advantageous locations, and accelerated technical training in partnership with global leaders such as LG and Northvolt.

Vietnam’s experience in advanced electronics is also instructive. Although companies such as Intel have opened design centers in Guadalajara, and Foxconn has expanded its assembly capacity, Mexico still imports more than 75 percent of the semiconductors it consumes. Vietnam, on the other hand, took advantage of agreements with Samsung to develop capabilities in packaging, intermediate design, and specialized technical training, gradually moving up the value chain. Rather than spectacular leaps, Vietnam’s progress was based on structural agreements, progressive accumulation of capabilities, and clearly defined objectives.

Mexico is home to more than 120,000 engineering graduates each year,11WorldAtlas, “Countries That Produce the Most Engineers,” (July 18, 2018) Retrieved April 23, 2025, from https://www.worldatlas.com/articles/countries-with-the-most-engineering-graduates.html industrial zones connected to high-volume ports and border crossings, and a manufacturing base that represents more than 18 percent of national GDP.12Ministry of Economy and Labor, Manufacturing industry in Mexico (2023), based on data from INEGI. What is lacking is not advantages, but a determined and coordinated strategy to transform these latent advantages into solid platforms for advanced production. The key is not to distribute efforts, but to concentrate them in sectors where the country can rapidly scale, generate critical capabilities, and open new routes for international insertion.

Investing and scaling

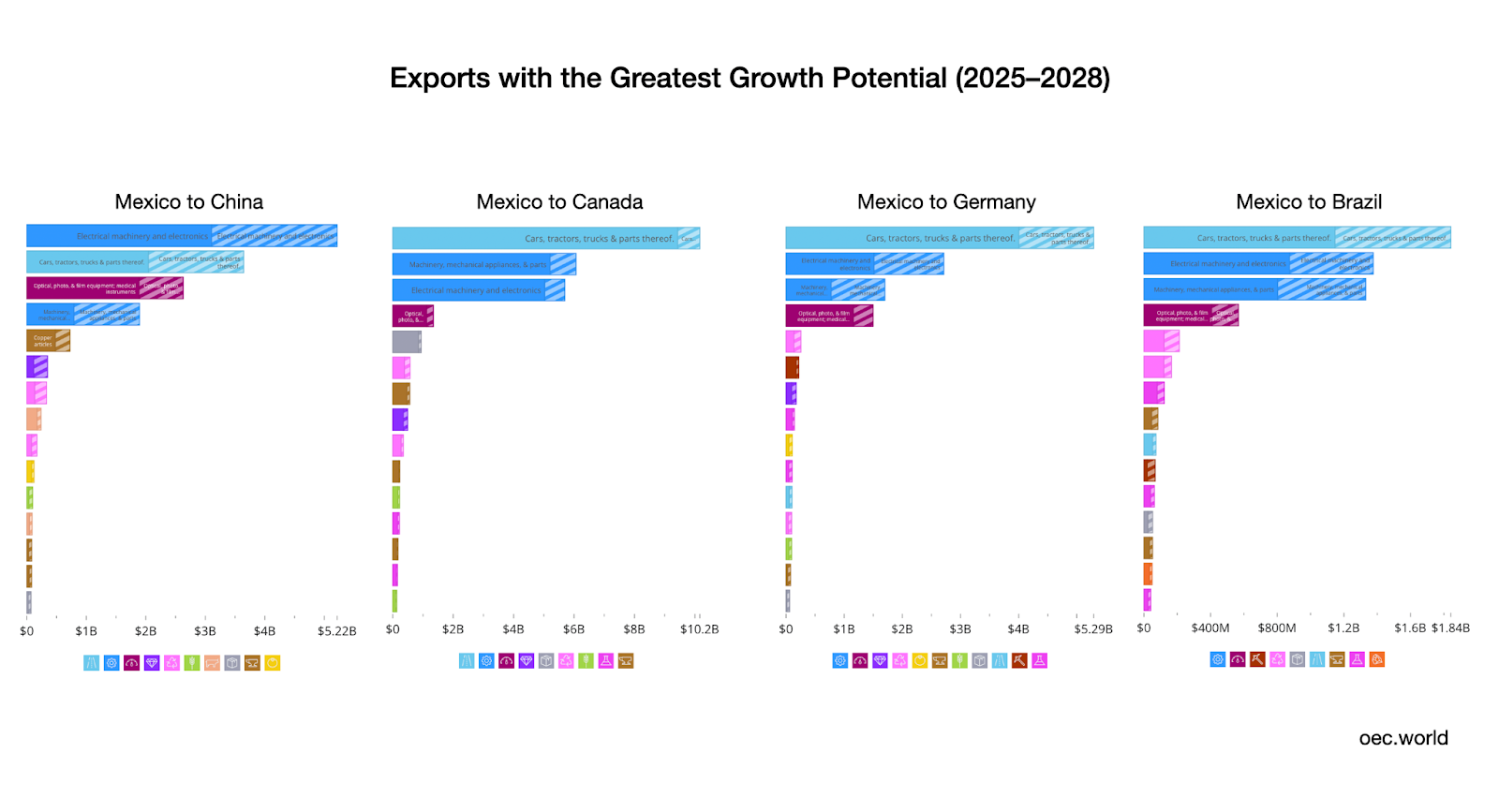

The question is no longer just to which countries to export more, but in which sectors and markets Mexico can scale quickly, reduce critical vulnerabilities, and build a more robust technological base. The export potential model of the Observatory of Economic Complexity (OEC) offers a concrete guide: it identifies high-impact niches where the conditions to compete already exist and where focused investment can transform current gaps into platforms for expansion.13Gilberto García-Vazquez, “Uncovering Hidden Trade Gems: Rethinking Export Potential with the OEC,” (<)em(>)OEC(<)/em(>). https://oec.world/en/blog/export-potential

Unlike traditional approaches, which project future trade based on past growth or geographic proximity, the OEC model incorporates productive capacities, technological linkages, and compatibility with destination country demand. By cross-referencing these factors, the model identifies products with high potential for expansion. The results are not generic: they point to concrete ways to diversify with strategic logic.

- China: Auto parts, integrated circuits, and advanced medical devices.

Estimated potential: more than US$3.2 billion in additional exports.

- Germany: Automotive manufacturing, industrial electronics, and computers.

Estimated potential: more than US$2 billion.

- Canada: Auto parts, digital technologies, and medical devices.

Estimated potential: more than $2.5 billion.

- Brazil: Commercial vehicles, advanced auto parts, and industrial electronics.

Estimated potential: more than $900 million.

These opportunities are not simply new trade destinations: they represent concrete routes to reduce dependence on the United States, increase the technological content of Mexican exports, and expand the country’s geo-economic radius of action. It is not a matter of competing with low prices, but of scaling up in terms of quality, sophistication, and strategic relevance. Taking advantage of these niches not only diversifies trade, but also redefines Mexico’s role in global value chains. Identifying opportunities is just the first step; capitalizing on them depends on building the capabilities needed to compete in those markets. Scaling up exports of medical devices to Germany or Canada, for example, requires reinforcing international certifications (CE, ISO), adapting regulatory frameworks and having advanced testing laboratories. Accessing markets such as integrated circuits in China or Germany requires electronic design, encapsulation, and functional testing: capacities that are still limited in the national productive ecosystem.

The same goes for infrastructure. Exporting complex manufactures to Asia or Europe will not be viable without reliable logistics routes, modern ports, and friction-reducing customs agreements. Opportunities may be well mapped, but without these enabling conditions, they will remain out of reach. Lack of seamless connectivity—by road, rail, port or regulation—not only makes operations more expensive, it also restricts the country’s ability to integrate into global chains with higher technological margins.

Integration and diversification can be brought together as parts of the same productive architecture. The scale achieved in sectors integrated with the United States offers a concrete starting point for identifying the links of greatest external dependence and turning them into platforms for technological expansion and trade openness. Turning these weak points into platforms of sophistication requires an integrated approach, where technological capabilities, industrial scale, and commercial access are developed in a coordinated manner.

From capabilities to policy

The productive transformation that Mexico needs will not be achieved with scattered programs or disconnected incentives. It requires prioritizing critical capabilities, mobilizing public instruments, and coordinating the public and private sectors around new trajectories of specialization. The goal is not only to increase exports, but to build a more autonomous, sophisticated, and resilient economy. But this process cannot succeed through inertia: it requires political vision, implementation capacity, and an institutional architecture capable of sustaining the effort beyond six-year cycles.

Mexico’s industrial base has grown in scale, but not in technological density or local integration. Today, less than 1 percent of Mexican companies participate directly in exports, reflecting a structural disconnect between foreign investment and the ecosystem of domestic suppliers.14OECD, SME and Entrepreneurship Policy Review: Mexico 2023, (<)em(>)OECD Publishing(<)/em(>) (2023) https://doi.org/10.1787/1cc9eaec-en Closing this gap does not require improvisation, but coordination. This implies linking tax incentives to increased domestic content in strategic sectors, promoting technological co-investment schemes between global firms and local suppliers, and launching accelerated training programs in mechatronics, encapsulation, advanced chemistry, and industrial automation. It is not a matter of replacing imports indiscriminately, but of developing technological autonomy in critical nodes—where the country is more vulnerable today, but also where the strategic return is greater.

Moreover, infrastructure not only facilitates trade: it determines who can participate in it. Today, logistical and energy bottlenecks limit the expansion capacity of entire regions. While in the north, some key US-Mexico border points operate under chronic saturation, generating high cost overruns, in the southern part of the country, a lag in energy infrastructure impedes the arrival of advanced manufacturing to areas with great industrial potential. In these regions, the electricity grid remains insufficient, its load capacity irregular, and costs uncompetitive in comparison to the north. A useful contrast is the SIEPAC project, which electrically connects six Central American countries. Mexico has yet to take full advantage of the project to pursue regional integration. A strategic expansion of the national grid—combined with investment in renewable energy and distributed storage–would link the south and southeast with the main industrial corridors of the country and open new routes for territorial diversification. Overcoming these barriers requires more than isolated investments: it requires an integrated vision that combines logistics, modern energy, and digital connectivity, transforming infrastructure into economic cohesion and regional competitiveness.

This scale of transformation requires an institutional center. Today, industrial policy is fragmented among ministries, trusts, programs, and levels of government, without a unified direction. The most successful experiences—from South Korea to Poland—were all characterized by political coordination. Without high-level coordination, it is impossible to align incentives, mobilize resources, and sustain priorities beyond a six-year term. Mexico needs a governing body that combines strategic vision with operational capacity: a National Industrial Policy Council that reports directly to the presidency, articulates measurable objectives in technological autonomy and export diversification, coordinates budgets and regulations between agencies, and ensures the participation of the private sector, state governments, and productive clusters. It is not a matter of creating yet another bureaucracy, but of providing the country with an institutional architecture capable of transforming capabilities into results.

The tariff threat is not simply a compounded risk. It is the visible symptom of a deeper structural vulnerability: a model of economic integration that, although successful in terms of export volume, was built on fragile foundations—technological dependence, geographic concentration, and scarce local articulation. Mexico’s industrial future will not be defined only by what it exports, but by how it produces goods, with whom it integrates production, and under what rules it sustains manufacturing. The dual strategy of integration and diversification is not ideological, it is a structural necessity in a world where trade is no longer governed by efficiency, but by power. The water dispute, which became a trade ultimatum, made it clear: no agreement guarantees stability when the rules can be changed at a press conference.

Still, Mexico has strategic sectors, emerging capabilities, and an industrial base that can scale. What is missing is not diagnosis, but sustained action, and a political will capable of transcending the enthusiasm of the first few months of a new presidency. The decisions Mexico makes in the coming years will define whether the country moves toward a more resilient, complex, and sovereign economy, or whether it perpetuates its own vulnerability.

Further Reading

Driving Capital

The USMCA, the IRA, and Mexico’s electric vehicle boom

Since President Biden signed the Inflation Reduction Act (IRA) into law in August 2022, the Mexican auto assembly and parts industries have been booming. Tesla...

The Runaway Shop

An interview with Jeffrey Hermanson on labor unionism and manufacturing under NAFTA and USMCA

In the early years of NAFTA, the maquiladora system undermined national manufacturing and unions in Mexico across industrial sectors, drawing workers around the country into...

The Fourth Transformation

The political economy of Claudia Sheinbaum’s popularity

As anti-incumbent sentiment toppled governments around the world in 2024, Mexico’s Morena won in a landslide, and the presidency was passed from Andrés Manuel López...