December 19, 2025

Analysis

Transformation without Taxation

Mexico's fiscal orthodoxy

In his famous 1918 essay “The Crisis of the Tax State,” Joseph Schumpeter captured the essence of fiscal sociology, arguing that “The spirit of a people, its cultural level, its social structure, the deeds its policy may prepare—all this and more is written in its fiscal history … He who knows how to listen to its message here discerns the thunder of world history more clearly than anywhere else.” In Mexico, however, this principle seems to have been suspended. There the Schumpeterian thunder is not heard. The project of the Fourth Transformation (4T), launched by Andrés Manuel López Obrador in 2018 and passed down to Claudia Sheinbaum Pardo last year, has sought to reorganize domestic political power, and it has had considerable success—redefining the national narrative and restructuring public spending priorities. Yet it has not significantly altered the tax structure built by previous governments.

This fiscal silence is even more surprising in light of the experiences of other leftist administrations in Latin America. In Bolivia, Evo Morales combined strategic nationalizations with an aggressive expansion of the fiscal apparatus. In Brazil, successive PT governments broadened the tax base while transferring income to the poorest citizens. Despite grappling with high levels of informality and low trust in state institutions, these projects understood that without new resources, it would be impossible to create new social rights. The 4T, by contrast, has tried to square the circle of distribution without serious tax reform.

In what follows we will look closely at this anomaly. Our aim is not to evaluate the overall fiscal performance of the 4T or the ruling Morena party, but to understand its decision not to pursue this crucial measure, despite having the legislative majorities to push it through. The obstacles here are not merely technical or electoral; they are rooted in Mexico’s particular model of political legitimacy: a state that asks for allegiance without demanding a contribution, and a citizenry that asks for rights without viewing taxation as a duty.

This model now appears to be reaching its limits. Sheinbaum has inherited not only the legacy of the 4T but also its most severe structural constraint: the state’s inability to adequately finance its own transformative project, which has become increasingly visible in the country’s latent fiscal deficit, pressure on public finances, and distributive conflicts. While the new president has tried to define her tenure as a bold extension of AMLO’s legacy, what we are beginning to see instead is a kind of exhausted continuity.

History of omission

In Latin America, most projects of national transformation have had an explicit fiscal dimension. The independence processes of the 19th century, the construction of nation-states, the social reforms of the 20th century, and even the most radical neoliberal experiments: all were accompanied by disputes over who should pay the treasury, how much, and for what. Yet Mexico’s tax history stands alone, characterized by silence, evasion, and exceptionalism. It is the story of a country that has tried repeatedly to re-found itself without developing a stable consensus on the sources of public revenue.

Since the colonial era, Mexico has had a highly ambiguous relationship between taxation and legitimacy. The Spanish Crown crafted a stratified tax system based on castes, privileges, and differentiated taxes, yet tax payments were nonetheless continually subject to negotiation, and exemption—rather than contribution—became a symbol of status. The War of Independence failed to change this situation. Though the conflict was catalyzed by fiscal tensions—ownership of tax revenues, indigenous tribute, customs duties, and ecclesiastical tithes—the newly independent state did not translate them into a modern tax system. The war destroyed the colonial apparatus without replacing it with a more effective one.

During the Reform period in the mid-19th century, fiscal questions were once again central to the project of modernization, amid the nationalization of clergy property and the confiscation of land. But this too failed to generate a coherent national culture of taxation or consolidate a sustainable tax base. The liberal state, more concerned with territorial control than fiscal equity, left intact many of the existing means of evasion. Far from creating a new relationship between citizenship and contribution, the regnant liberalism of this period relied on external loans, mining concessions, and structural indebtedness.

The Mexican Revolution of the early twentieth century was perhaps the most clear-cut example of this omission: a social revolution without fiscal reform. The 1917 Constitution enshrined labor rights, distributed land to peasants, and forged an interventionist state, but neglected any equivalent transformation of the tax system. Public monopolies were created and a centralized redistributive apparatus was built with an extremely narrow financial base. The post-revolutionary tax system was defined by its dependence on extraordinary revenues—mainly natural resources—and its low level of direct taxation on the upper classes and accumulated wealth.

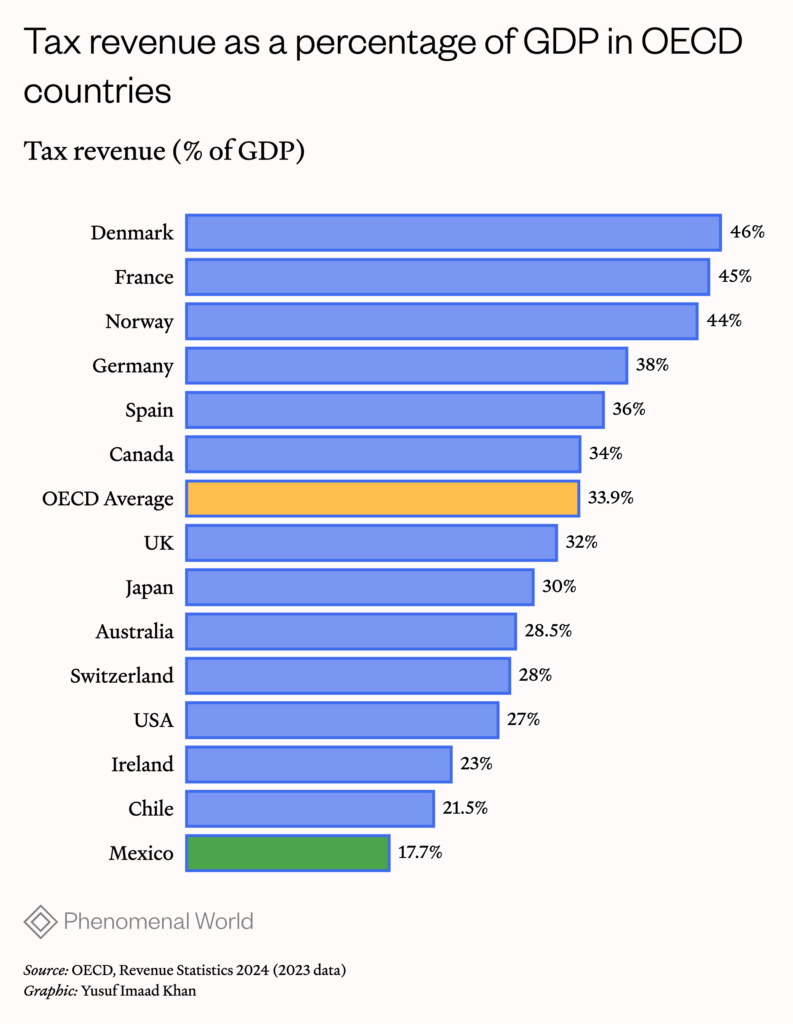

This continuity has had long-term structural consequences. In 2024, tax revenues represented less than 18 percent of GDP, well below the average for Latin America and any OECD country. This is not just a quantitative weakness; there is also a deeper qualitative dimension, as the Mexican state seems to have given up on building a civic bond around taxation. The idea that taxes are the price of living together, a part of the social contract, has not taken hold among the masses or elites. Instead, the logic of exception—in which those with the means to evade tend to do so—has endured, and the state has become ever more resigned to its fiscal weakness, waiting for remittances from emigres or holding out hope that a new oil field will improve its fortunes.

During the 20th century, the governments of the then hegemonic Institutional Revolutionary Party (PRI) were able to maintain their legitimacy for decades through spending—on education, infrastructure, subsidies—without touching the fiscal interests of upper classes, thanks to the availability of natural resources like oil and the international credit lines that they unlocked. But this oil surplus was a mixed blessing, with at least two negative consequences for Mexico’s fiscal sociology. First, it made it unnecessary to build fiscal consent: to create a collective imaginary about how taxes are used and distributed, and how they relate to rights. Second, this lacuna allowed for increasing collusion between the spheres of political and economic power, as businesses’ lax approach to the tax authorities mutated into a relationship of parasitism, in which the public sector was used to stabilize, rescue, or “develop” private interests, from monopolies to banks to tourist traps.

By the end of the 1970s, this model had begun to falter, and the onset of the debt crisis, trade liberalization, and falling oil prices marked the beginning of a new era. The state now lacked both the resources to deal with these problems and the political will to rebuild the fiscal pact from its foundations. This was in large part because it had made substantial commitments to such private interests, who over the previous years had gone from being mere freeloaders to acting as managers of the public sector under the so-called New Public Management regime. It was in this same period that the PRI turned to the flagship neoliberal taxation policy, VAT, which was introduced in 1980 and increased in 1995: a regressive measure that taxes general consumption without distinguishing between people’s differing abilities to pay, reducing the burden on high incomes while targeting the poorest.

Seven decades of PRI rule finally came to an end in 2000. In its wake, the two subsequent administrations of the right-wing National Action Party (PAN) refused to alter the main pillars of the tax regime, yet pledged to administer it more rationally. They pursued regulation to close loopholes in the system but made no attempt to move it in a more equitable direction. Exemptions continued to be granted on a transactional basis, informal labor was still treated as a cultural anomaly rather than a structural feature, and the political taboo on upsetting large taxpayers remained in force. In lieu of fiscal citizenship, spending was still the foundation of state legitimacy.

In 2012 the PRI returned to the presidency with the election of Enrique Peña Nieto, who pushed through a fiscal reform the following year that partially broke with this inertia. It sought to broaden the tax base, eliminate privileges, and increase non-oil revenue in a context of falling prices. Yet it lacked real political content: rather than seeking to transform the relationship between citizens and the state, its aim was merely to stabilize government revenues. The social order was untouched. Although the tax structure was now somewhat sturdier, this improvement was overshadowed by numerous corruption scandals that plagued Nieto’s six-year term.

This was the backdrop for the Fourth Transformation of 2018 onward: a project that in some ways represented a definitive break with the past, but which also inherited and indeed reproduced this ingrained political culture.

Conflict avoidance

From the outset, López Obrador framed his presidency as a repudiation of neoliberalism, understood not so much as an ideology but as a set of practices associated with corruption, dispossession, and the subordination of the state to private interests. The 4T was not formulated as an economic program in the narrow sense but as a wider narrative of restoration: returning the state to the people, eliminating privileges, redistributing power, and rejecting technocratic mediation. Within this framework, there was always a certain ambivalence about the fiscal issue. While AMLO criticized the clientelistic use of the state budget, he offered no clear argument for increasing tax collection. His message was primarily a moral one: the problem was not how much tax was collected, but where it went: to the elites or to the people, the “corruption pipeline” or national development projects.

This ambivalence later hardened into a doctrine. The AMLO government adopted a strategy that could be summed up as “austerity with efficiency,” seeking to cut superfluous spending, eliminate tax breaks for large taxpayers, and demonstrate that the existing budget, if spent wisely, was enough to finance the country’s transformation. AMLO himself argued that “if there are savings from outlawing corruption and the extravagances of senior public officials, there is no need to raise taxes … Just get rid of tax evasion, get rid of privileges, don’t forgive taxes for the powerful … and the revenue will be sufficient.”

To support this vision, the economist Diego Castañeda invoked the image of the simple farmer: before “sowing” new taxes, the government must first clear the land, improve management, and harvest legitimacy through efficient and honest spending. The promise, then, was twofold: that existing resources would be sufficient if used correctly, and that powerful economic sectors would not be touched as long as they complied with the law.

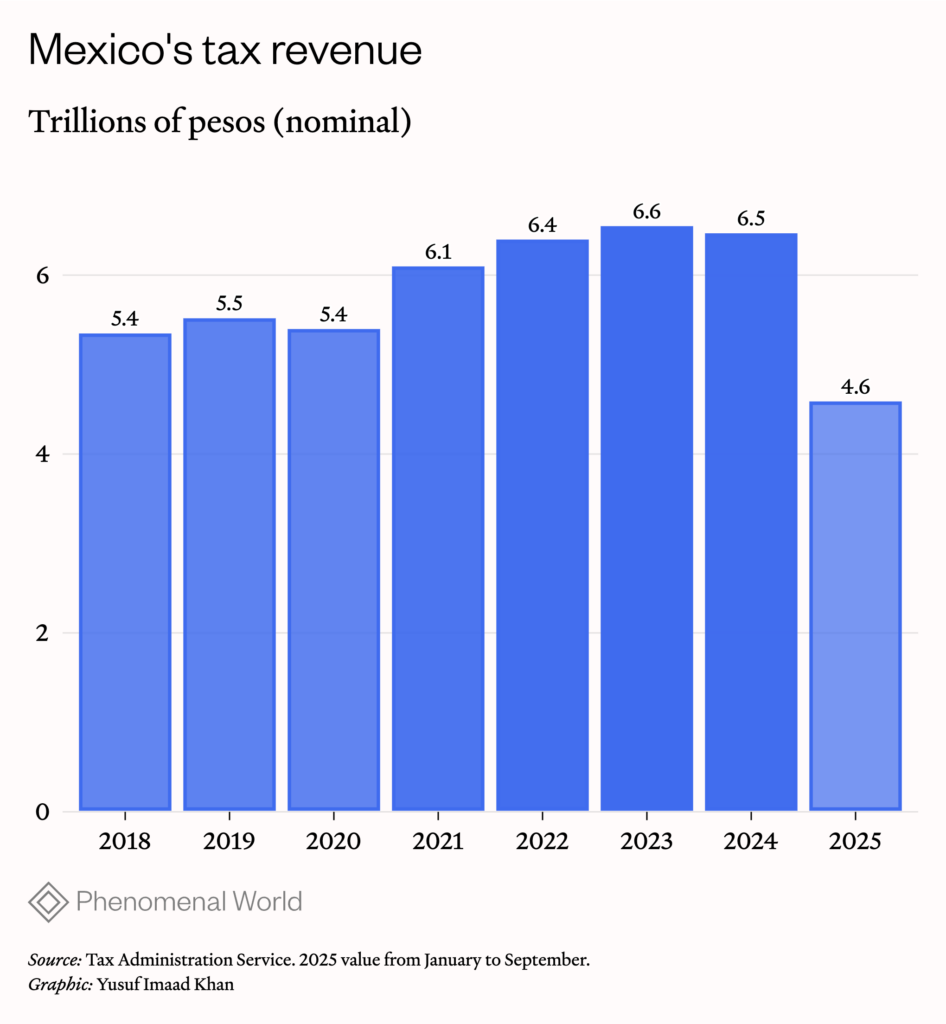

This strategy brought tangible benefits. Between 2019 and 2021, the Tax Administration Service (SAT) increased effective tax collection without the need for major legal reforms. Administrative capacities were strengthened and tax evaders were openly confronted. The state clamped down on the culture of tax forgiveness and evasion and audited large taxpayers, presenting this almost as an act of moral hygiene. The SAT reported that during AMLO’s administration tax collection increased by around 60 percent in nominal terms, from 2 trillion 299 billion pesos in 2018 to 3 trillion 697 billion pesos in 2024 (a figure only includes taxation of large taxpayers without oil revenues).

But there were difficulties beneath the surface. This agenda depended on the implicit consent of business, which accepted the new settlement as long as the main pillars of the tax regime were not challenged. At the same stroke, it also put the financing of the 4T in doubt, as programs such as “Jóvenes Construyendo el Futuro” (Youth Building the Future), “Sembrando Vida” (Sowing Life), and the universal pension for the elderly, were all funded without increasing the tax base—putting increasing pressure on the state budget, which could only stretch so far.

The Covid-19 pandemic brought these problems to the fore. While other countries resorted to debt and fiscal stimulus to deal with the crisis, the Mexican government insisted on maintaining strict budgetary balance. There were no massive bailouts, no universal direct aid, and no increase in public investment to mitigate the economic blow. The IMF rewarded the government for its pandemic response with Special Drawing Rights. As a result, austerity remained the guiding principle even in these exceptional circumstances: protecting the macroeconomic balance while sacrificing the income of millions of families.

Politically, however, none of this seemed to matter. The government maintained high approval ratings, preserved its image of fiscal honesty, and managed to avoid direct confrontation with business elites—except for a few emblematic figures such as Ricardo Salinas Pliego. The 4T managed to consolidate fiscal orthodoxy while giving it a popular form, creating the image of a disciplined administration, meticulous in controlling spending, and unwilling to spark needless conflict.

The avoidance of progressive tax reform was not only a matter of expediency, but also of genuine conviction. The government was invested in the notion that ordinary people already pay a lot—despite Mexico’s relatively low tax burden—and that the state must prove its worth before demanding more. Consequently the political capital Morena accumulated between 2018 and 2021 was not used to initiate a serious discussion about taxing wealth, inheritance, digital platforms, or idle assets. But while this may have paid off for AMLO, his successor is now encountering its contradictions.

Turning point

Claudia Sheinbaum came to power on the double promise of continuing the 4T project and addressing the areas it had neglected. Her academic background as a scientist, plus her track record as Head of the Mexico City Government from 2018 to 2023, generated different expectations among different groups—the popular sectors viewed her as the legitimate heir to AMLO’s project while the middle classes saw her as an enlightened technocrat capable of guaranteeing stability. After her election she reiterated that the transformation would continue without additional taxes and that fiscal discipline was a condition of sovereignty. Only a few months into her term, however, the cracks began to show.

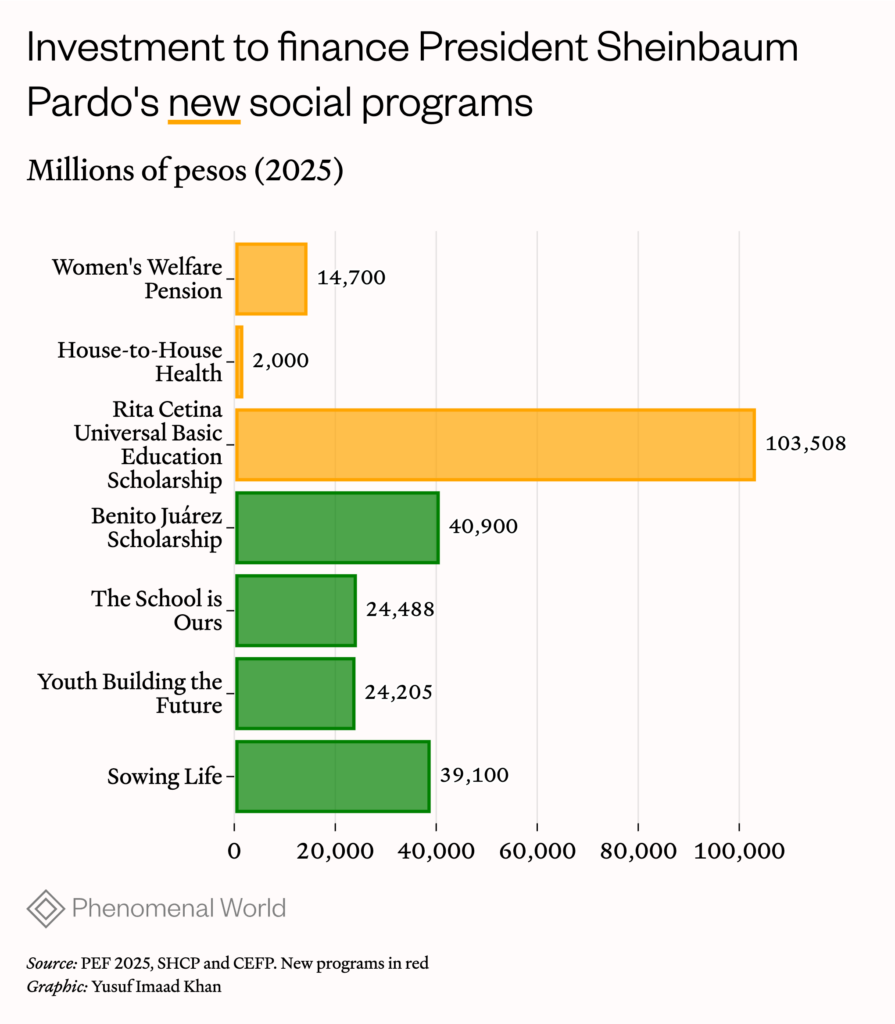

When the National Coordination of Education Workers (CNTE)—a dissident teachers’ union with a long history of labor militancy—demanded pension changes along with salary increases, it highlighted an uncomfortable fact. The state no longer had any fiscal margin, thanks in large part to the financial burden of state-owned organizations such as the oil company Pemex, whose debt servicing is due to cost MX$180 billion in 2025 alone. Sheinbaum had also maintained existing social programs such as support for the elderly and launched three new ones—a special pension for women between the ages of 60 and 64, a universal scholarship scheme for secondary school students, and a program in which medical and nursing staff provide home health care to vulnerable populations—in addition to various public works projects. Looking at the balance sheet, the new president was forced to concede that the current reserves were “not enough” to satisfy the teachers: a candid admission of budgetary constraints of the kind that AMLO had never made.

Other incidents helped to foreground the tax issue. One was the president’s promise, made in a morning press conference, to reimburse Mexicans living in the United States: a proposal so costly it was soon withdrawn. Another was the government’s conflict with Salinas over his debts to the SAT. Yet despite the issue having moved up the agenda, Sheinbaum’s administration continues to focus on other battles, such as judicial reforms to allow the popular election of judges. The pattern of evasion continues. When the government presented its annual revenue and expenditure proposals to the legislature in September, the Ministry of Finance had already reiterated that it had no plans to promote tax reform, aside from some piecemeal measures such as “health taxes” on products like sugary drinks.

In this context, the notion of a “second stage” of transformation has been put in doubt. Is this a programmatic expansion or merely an institutional consolidation? If the new phase of the 4T does not include tax reform, what distinguishes it from the old one? The risk is that, in trying to create this narrative of continuity without committing to fiscal conflict, Sheinbaum’s administration will become little more than a managerial one, whose main role is to allocate increasingly sparse resources. The Morena leadership appears to be aware that any attempt at progressive taxation will inevitably be met with resistance, not only from elites, but also from the informal sectors and even the middle classes who benefit from the status quo. What it is less willing to acknowledge is that, if it refuses to face up to this confrontation, it could jeopardize the social programs that it has pledged to maintain or extend, along with its ability to guarantee the rights to education, health, and even housing as enshrined in the Constitution.

The 4T has been extraordinarily successful in changing the political framework of the Mexican state without remodeling its financial base. Looking ahead to the next elections in 2027, and to Morena’s longer-term prospects, the question is not whether Sheinbaum’s ambitious policies can be achieved within these constraints—the overwhelming evidence is that they cannot. It is, rather, how long the ruling coalition can avoid an inescapable truth: there can be no transformation without taxation.

Further Reading

How Mexico Doubled the Minimum Wage

Monopsony, corporate power, and the labor market

The Fourth Transformation

The political economy of Claudia Sheinbaum’s popularity

Mexico’s Big Green State

Claudia Sheinbaum plans to repurpose the country's state-owned enterprises towards decarbonization

Further Reading

How Mexico Doubled the Minimum Wage

Monopsony, corporate power, and the labor market

The minimum wage in Mexico has more than doubled in real terms over the last six years. This is no small feat, especially if we...

The Fourth Transformation

The political economy of Claudia Sheinbaum’s popularity

As anti-incumbent sentiment toppled governments around the world in 2024, Mexico’s Morena won in a landslide, and the presidency was passed from Andrés Manuel López...

Mexico’s Big Green State

Claudia Sheinbaum plans to repurpose the country's state-owned enterprises towards decarbonization

AMLO's government emphasized the importance of state-owned enterprises for reviving Mexico's energy sector. With her announced regulatory reforms, President Claudia Sheinbaum is reorienting these enterprises...