September 19, 2025

Interviews

The Belt and Road 2.0

An interview with Mathias Larsen on China’s overseas clean-tech manufacturing investments

Chinese firms are going out.

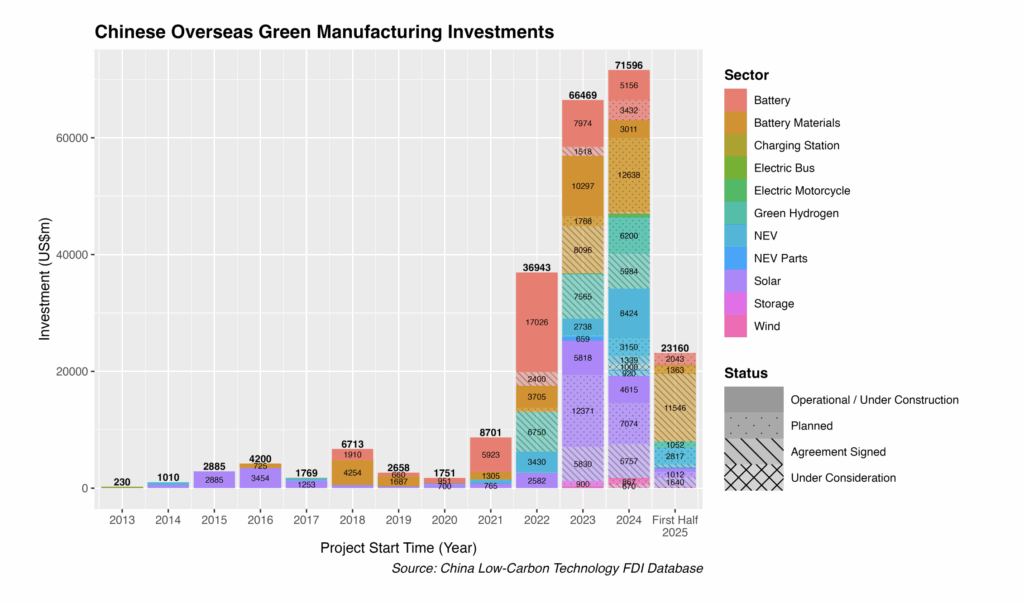

As the US withdraws from green tech industries and pressures its allies to follow suit, Chinese firms are stepping in to power the developing world’s green transition. A new report from the Net Zero Industrial Policy Lab at Johns Hopkins University, co-authored by NZIPL Fellow Xiaokang (Harold) Xue and Senior Policy Fellow at LSE’s Grantham Research Institute on Climate Change & the Environment Mathias Larsen, previews the insights from a comprehensive database on Chinese overseas investments in clean tech manufacturing. The scale is staggering. Chinese firms have committed over $227 billion across 461 green manufacturing projects in 54 countries since 2011—with 88 percent of investment occurring just since 2022. In inflation-adjusted dollars, this sum is larger than the $200 billion Marshall Plan.

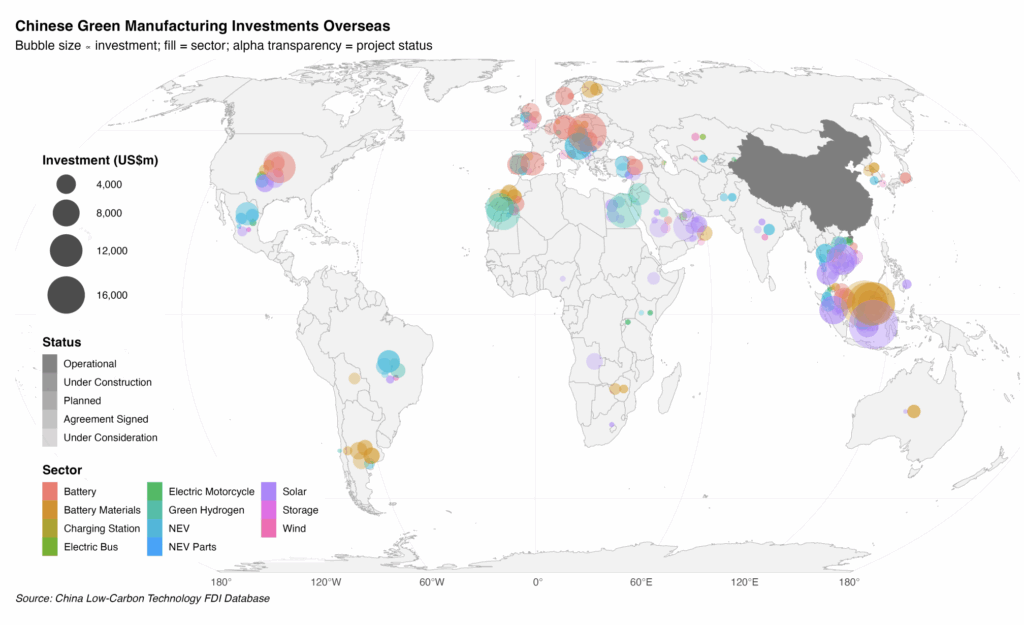

At the moment when climate action is most urgent, and clean energy is becoming the cheapest source of power globally, the US is walking away from the ambition to lead or even participate in that transition. Meanwhile, China has surged green investment domestically and built end-to-end control of green supply chains: solar, batteries, EVs, wind turbines, green hydrogen. And its firms are bringing this capacity to the developing world, with over 75 percent of these projects located in global South countries eager for industrial capacity.

In a report based on Xue and Larsen’s research, Bloomberg’s David Fickling contrasted the two trends: “Right now, Beijing is offering cheap, clean power, employment, trade and a route to prosperity. Washington is offering tariffs, policy chaos, White nationalist memes and South Korean workers in shackles after a raid on an EV battery factory. This is no way to win the grand strategic contest of the 21st century.”

Tim Sahay, the Co-director of NZIPL and co-author of the Polycrisis newsletter spoke with Mathias Larsen about the new research and what it tells us about the developing shape of the global green transition and this pivotal moment in global economic history.

An interview with Mathias Larsen

TIM SAHAY: China’s total dominance in green technologies has provoked anxiety in many countries among policymakers, analysts, and captains of industry—overcapacity and dumping are the watchwords of the moment. One prescription in response has been that China should set up green factories abroad, rather than send out ships laden with green goods. So is that happening?

ML: What our research demonstrates is, in summary, a massive increase of Chinese outward investments in the manufacturing of clean technologies. This both supports the host countries’ development and supports a global green transition.

There are five key takeaways. The first is the scale of investments: more than $200 billion, toward $250 billion, with a rapid increase since 2022. It’s nearing $100 billion a year, which is around the same amount that China gave in infrastructure loans when that peaked in 2018. In comparison, the Marshall Plan by the US after the Second World War was around $200 billion in total. The Marshall Plan locked Europe into US technologies and standards, so when we see sums of this size, we can ask whether it will potentially have a similar effect in the future.

To put this in perspective, China’s domestic investments in green manufacturing were $340 billion in 2024. Compared to $70 billion in outwards green FDI, that’s a fifth. It’s the same ratio in terms of stock, where there’s about a trillion of investments in green manufacturing domestically. Now this stock here is getting past $200 billion, also a fifth.

The second crucial point is the speed of the increase. The Belt And Road Initiative was primarily infrastructure loans, which peaked in 2018 at around $100 billion per year. That figure fell off a cliff, and there was a valley from 2020 to 2022, with basically no outbound Chinese investments or loans at all. And from 2022, we see a rapid increase in the FDI that we are tracking. While numbers for 2025 suggest a stagnation, the pattern may end up near this prior level, around $100 billion a year. So we can clearly call this BRI 2.0.

The third point is the status of the projects. Most of the projects we’ve identified here are not actually operational yet, meaning actual production capacity will come online within a year or two. That is the point at which we should see the actual impacts of the projects, both on the host country’s development and in terms of the global dissemination of these technologies.

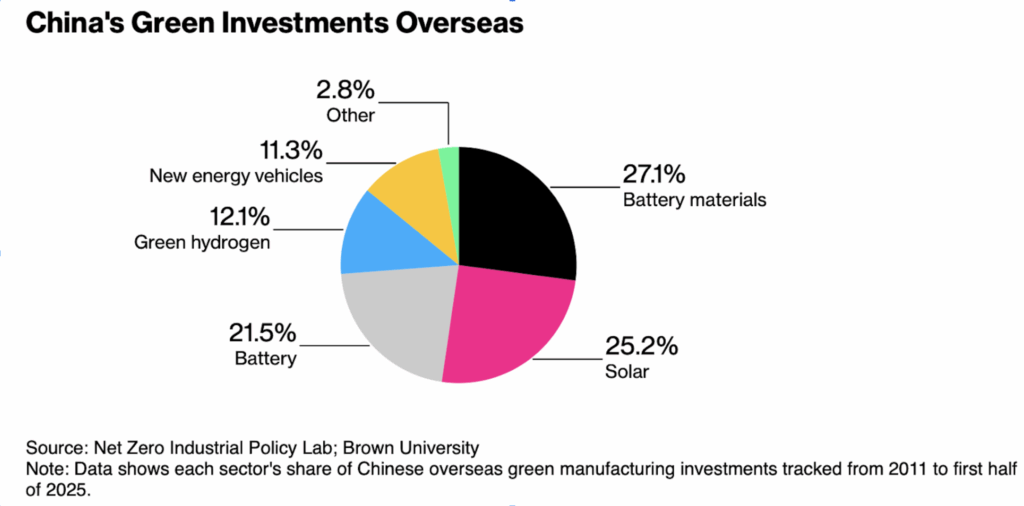

The fourth point is around the technologies themselves. These investments cover most green technologies, with over half being solar and battery technologies. That means that China’s total dominance of green tech, which we are all increasingly familiar with, is globalizing. (There’s a little bit less wind in the mix, but it’s still part of the picture.)

The fifth point is the breadth of that globalization: These investments are taking place across all continents.

And just a couple of words on the scope of this new database. It covers Chinese companies investing in foreign countries, meaning it does not include other countries’ firms nor Chinese domestic investments. And it counts investments and not loans, which were the previous type of foreign engagements we know as the Belt and Road Initiative. We also focus on manufacturing, not power generation, and specifically we focus on clean technology manufacturing. Prior work tracking these kinds of investments has been less comprehensive—it gave us a hunch that China was doing this kind of foreign direct investment, but didn’t give any clear indication of the action scale and ramifications of that investment.

TS: What are the motivations of private Chinese firms “going out” and internationalizing their supply chains? To what extent is it a private capitalist firm-driven strategy versus a host-country developmentalist strategy?

ML: There are certain countries that get a lot out of these investments, which are clearly part of their own development strategy. But what we see most clearly from this data is that there are basically three motives for the Chinese companies at play.

The first is access to the host country market. Many countries realize that green tech is becoming a large share of their economies, and that simply importing clean tech will have negative consequences on industries and employment and so on, and therefore they put in tariffs and local content requirements to ensure that some parts of the value chains are inside the countries. That’s the case in Brazil, for example.

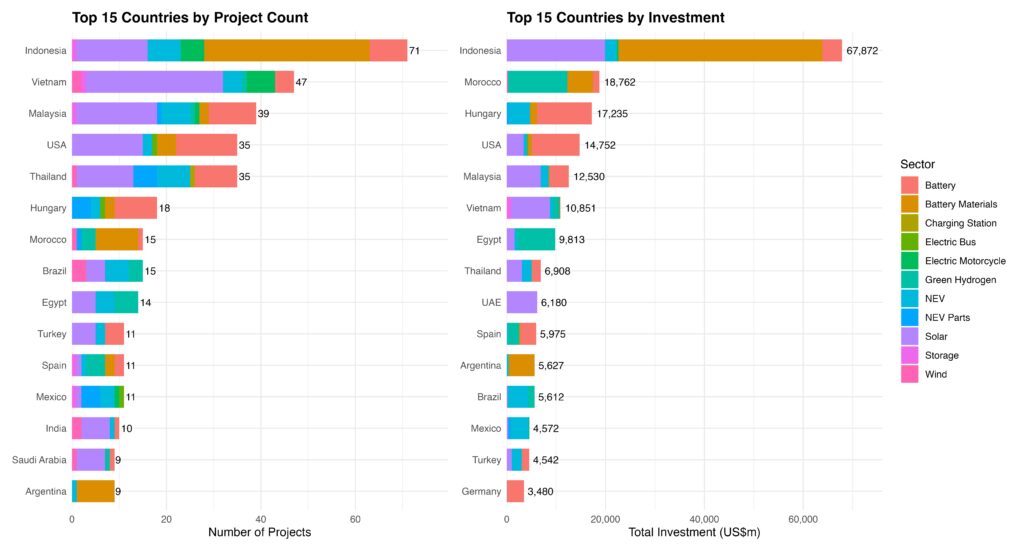

The second reason is access to third-party markets. As big markets like the US and the EU put up high tariffs on direct imports from China, Chinese cleantech firms invest in manufacturing in places that have access to these markets. Morocco is an important example here, because it has free trade agreements with the US and the EU.

The third is access to raw material inputs. As this manufacturing scale grows, so does the need for the raw materials for it—nickel, cobalt, lithium, and so on. Mining is one part of that, but processing also increasingly takes place in host countries. Indonesia is the major example, where a country bargains with China to capture a larger share of the value of the manufacturing supply chain.

TS: How should we interpret what this overseas green manufacturing push means for China’s role in the global green transition?

ML: These overseas Chinese investments are straightforwardly good for climate. They can play a key role in advancing the global dissemination of clean technologies driving down prices, and increasing the pace at which these clean technologies are deployed. Whether these manufacturing investments create overcapacity is essentially a question of whether there are profits to be made from the investments—not a concern about whether these technologies are needed, because obviously we need to scale up the pace of deployment to meet the goals of the Paris Agreement.

The impact on host country development and decarbonization will be heavily dependent on those countries’ domestic political economy and policymaking space. These investments create a window of opportunity for host countries to conduct industrial policy to advance domestic developmental goals—some have done a good job at that, some have done a less good job.

Another dynamic to consider is what this means regarding China’s role in finance for the global South. As mentioned, BRI lending decreased dramatically, and was replaced by the “Small and Beautiful” strategy—shifting away from financing for large infrastructure projects, and toward smaller scale and more lucrative projects and sectors. (It was basically more Small than Beautiful.) So the scale we are witnessing is meaningful, and arguably a good thing for the pace of development and the green transition—as many global South countries are in near debt distress or fearful of getting there. Over-indebtedness is, of course, not a problem with foreign direct investment, as any loans related to these projects sit on the balance sheets of the Chinese firms and not the host country.

Then there is global trade. China currently has a $1 trillion current account surplus. If manufacturing moves abroad, this might, to some degree, reduce this surplus. Right now, cleantech only represents 5 percent of Chinese exports, but it’s a growing figure. The trend of “going out” might limit direct exports from China, and reduce some of these imbalances in the Chinese economy.

TS: What has been the role of the Chinese state in supporting this private sector BRI 2.0 ? Is there a lot of planning, funding, coordination, and implementation?

ML: BRI 1.0 was entirely state-driven. Projects were organized by the Chinese government and the given host country. They were then operationalized by financing from Chinese policy banks, Chinese state-owned commercial banks, Chinese state-owned insurance companies like Sinosure, and then largely constructed by Chinese state-owned construction companies. It was all hands of the state on both sides. The loans would be sovereign-backed or tied to revenue sources from commodity sales, and so on.

By contrast, this BRI 2.0 phenomenon is all private. It’s the private companies that raise the capital themselves to do investments. Projects are certainly encouraged by host countries because they want this type of FDI, but typically they aren’t being subsidized in any way by the host countries or the Chinese state.

Given the vast and widely studied state support for the BRI, this is kind of surprising! In all the talks I’ve had with Chinese banks doing this type of lending and principal, they do not appear to have, at any meaningful scale, given loans to Chinese private companies to make these kinds of overseas green manufacturing investments. We can take the example of Build Your Dreams (BYD), which did a partial listing in Hong Kong to finance their overseas investments; they didn’t get the money from the China Development Bank. This is a very clear contrast in the role of the state across the first BRI and what we are showing with this data.

What may be most surprising to outside observers is what I found in my interviews: Chinese government officials themselves may not be aware of the full range and aggregated total of these private sector green investments overseas. Individual ministries, like the Ministry of Commerce, of course give approvals to firms going out, but those approvals are done at the project-level. If the Chinese government itself is not tracking or coordinating such a massive surge of outward green manufacturing investment, it’s unlikely that this private sector-led BRI 2.0 is being coordinated at the government-to-government level.

TS: How do recipient countries view Chinese green manufacturing investments, compared to Western alternatives. What recommendations would you give for the EU, for example, in their response to China’s financing overseas? Should it be competition, should it be collaboration?

ML: I think it’s important to understand at the outset that in large part Chinese companies are not doing these kinds of investments as a matter of preference—they would prefer to maximize their profits by manufacturing their product inside China and then exporting it.

It is only because host countries put conditions against Chinese imports that firms are forced to make these investments. As mentioned, host countries recognize that imports of new technologies from China represent a potential danger for their own industrial base, plans for further industrialization and development, employment, and so on. Manufacturing FDI from China, by contrast, can be seen as a potential opportunity to use these investments for industrialization, employment, and development goals. The crucial question is if and how the host country is able to make use of that opportunity.

How are host countries responding to maximize their own benefit from these investments? What principles and conditions should be demanded of Chinese investors? And how should new countries potentially receive these investments position themselves in global supply chains? What kind of requirements should they make for Chinese investors? Future analysis of this massive scale of planned investments should be oriented towards these questions.

Further Reading

Global BYD

The international expansion of Chinese electric vehicles

Amid the intensifying retreat of American hegemony, an alternative geo-economic and geopolitical arrangement is coming into view: a battery-powered globalization with Chinese characteristics. Chinese EV...

Who Will the Green Transition Save?

An interview with Alfredo Santos of CUT-Bahia on Brazil’s Camaçari Industrial Complex

The Camaçari Industrial Complex in Bahia attracted worldwide attention following BYD’s announcement in 2023 that it would be home to the electric vehicle company’s largest...

BRICS in 2025

Two energy systems and development models compete for primacy within the group

Within the BRICS group, two competing global models of energy, growth, and influence. The future of the world’s majority will be decided by the pace...