This week marks the sixty-first anniversary of the military coup in Brazil, coinciding with a time of great instability in the country’s liberal democracy. A few days ago, the Federal Supreme Court ordered Jair Bolsonaro to stand trial for attempting a coup during the 2022 elections, an event that for Brazilian progressive forces evoked memories of the terror under the dictatorship and renewed debates about the threat of authoritarianism today. To explore the meaning of these experiences in light of current events, Phenomenal World editor Hugo Fanton spoke to Frei Betto, an organizer whose social and political work helped facilitate the resistance to the Brazilian military dictatorship, and caused him to be twice imprisoned by that regime.

A Dominican friar and writer, Frei Betto took part in the creation of the ecclesial base communities (Communidades Ecclesial do Base, or base communities), a form of organization encouraged by the parts of the Catholic Church practicing liberation theology in Brazil during the Cold War. These groups met regularly in a specific area—slums, schools, factories, etc.—to combine biblical reading with a debate on the political and social reality they were experiencing. They became one of the main mechanisms of resistance to the dictatorship and the fight for democracy in Brazil.

Frei Betto is the author of a number of books based on the experience of community organizing during the dictatorship, including Letters from Prison and Baptism of Blood, a work exposing the military regime for its crimes against humanity.

At a time when authoritarian forces are advancing in Brazil and around the world, and with the number of arrests and deportations rapidly increasing in the US under Donald Trump, the processes of regime transition toward increasingly authoritarian methods are more relevant than they’ve been in decades—as are the struggles to ensure that the horrors experienced in Brazil are never repeated.

An interview with Frei Betto

Hugo fanton: April 1 marks the sixty-first anniversary of the military coup in Brazil. Could you put it into context?

FREI BETTO: After the Second World War, as the Allies succeeded in defeating Nazi-fascism, a wave of democratization led popular movements worldwide to organize and demand rights. In Brazil, Getúlio Vargas returned to power in 1950. He had ruled the country under a dictatorial regime for 15 years, but had granted great benefits to the working class and was therefore considered the “father of the poor.” Vargas was also the mother of the rich, but in this new government, at the beginning of the 1950s, the conservative sectors of Brazilian society plotted to overthrow him because they did not accept policies that promoted better living conditions for the working classes. This right-wing conspiracy led to Vargas’ suicide in 1954, and Brazil entered a period of great political instability.

At the beginning of the 1960s, Jânio Quadros was elected, which only deepened this instability, as he resigned seven months after being elected, thinking that there would be a large national mobilization to bring him back to the presidency with authoritarian powers. That didn’t happen. The vice-president, João Goulart, better known as Jango, took over.

In this period, the word that most defined Brazil was the adjective “new.” Bossa was nova, cinema was new, literature was new. Celso Furtado’s economy was new, everything was new. Brazil was experiencing its emancipation and a progressive turn, which granted more freedom to social movements such as the peasant leagues and the student movement. In short, it was an effervescent country with a lot of creativity, many achievements, and economic policies that were quite unexpected. All of this was dismantled by the military coup of April 1, 1964.

The Brazilian elite didn’t anticipate that the popular sectors would threaten the privileges and interests of the ruling classes by, for example, demanding land reform. Brazil is a country of continental dimensions and has never known land reform, unlike its neighbors Bolivia and Peru, to name just two examples. This threat to privileges led to several coups with support from the White House, which established civil-military dictatorships throughout Latin America. This happened in many countries on our continent, as part of the US campaign to contain communism. In Brazil, while João Goulart’s government had many progressive aspects, there was nothing communist about him. He was a democrat and even a landowner, but he was sensitive to popular demands. As a reaction to this agenda, the military, subsidized by and in coordination with the United States government, carried out a coup on April 1, 1964. They tore up the Brazilian Constitution and implemented a regime of terror that lasted twenty-one years, of which I was personally a victim.

HF: How did this affect your life at the time?

fb: I was arrested as a student leader for fifteen days in June 1964, a few months after the coup. Then, in 1969, while working as a Dominican friar, I was arrested again for my work in support of the resistance and the struggle to re-democratize the country. I remained in prison for four years, until 1973. That period was marked by a lot of cruelty, torture, and the disappearances of those who were fighting for another social system, in this case socialism, or for the mere re-democratization of their countries. And we saw the spread of military coups to Argentina, Uruguay, and Chile. This tragic period in Latin American history was all financed, bankrolled, and sponsored by the White House.

At the beginning of the dictatorship, some liberal and democratic leaders, such as Rubens Paiva, who is portrayed in the film Ainda Estou Aqui (I’m Still Here), thought that the coup would just be a period of rearrangement for the ruling classes, under the tutelage of the military. They didn’t think there would be torture, disappearances, shootings, or cruelty at such a scale, as is condensed in the work Brazil: Never Again.

But the dictatorship did take hold, and although different generals took turns as president, its character became increasingly violent, murderous, and genocidal. The situation became more dire after December 1968, when the regime passed Institutional Act No. 5, which many analysts call the coup within the coup, as it institutionalized extrajudicial killings and the suspension of civil rights. Things really escalated at that point, and democratic forces began to resist the military dictatorship, both by peaceful means and by armed means. Groups and parties began to arm themselves in order to confront the military power of the dictatorship. This led to a great deal of wear and tear on the military regime.

HF: What was the work of resistance like throughout the 1970s? What would you highlight in terms of this organizing—whether it was comprised of permanent, daily, or less habitual patterns of opposition—in the extremely unfavorable context of political arrests, torture, murders, and disappearances?

fb: There was a period when this resistance was clandestine, either peacefully or through armed struggle. But during the mid-1970s it took on the dimensions of a mass struggle through union strikes. The union movement, led by Lula, denounced the dictatorship’s economic policy—the so-called “miracle”—as false, a big lie to cover up the real dynamics of the economy. Large unions began to mobilize, bringing thousands of people onto the streets to demand labor rights. This progressively undermined the foundations of the dictatorship.

The positive consensus in Brazilian society that the military had saved the country from communism started to fade as people became increasingly aware of the regime’s atrocities. It was also very important that official trade unionism was opposed and replaced by grassroots mobilization.

Brazil has always had grassroots organizations. From the sixties onward, through the progressive sectors of the Catholic Church, we formed the base communities that gave birth to what is known today as liberation theology. These communities did not attract the attention of the dictatorship, which considered them just a religious phenomenon. Meetings would begin with a reading of the Bible from the perspective of the oppressed, through an embrace of Paulo Freire’s pedagogical method. Ignoring the base communities was a big mistake on the part of the military, as these meetings turned toward training militants for popular activist movements, for trade union mobilizations, and, later, for organizing new political parties.

Between the 1960s and 1970s, there was a great spread of progressive Catholicism in Brazil. Grassroots organizing extended through favelas and factories, generating a more combative opposition within trade unions then tied to the dictatorship. This organizing struggle opened the way for new political parties. Among them was the Workers’ Party led by Lula.

So this is the process that brought together popular forces and undermined the dictatorial regime. Its victories included the return of exiles and the establishment of new national associations for organizing the working classes, such as the Central Única dos Trabalhadores and the Movimento dos Trabalhadores Rurais Sem Terra.

Unfortunately this process, this progressive organizational accumulation, has been lost in recent years. The election of Bolsonaro points to a global phenomena of weakened progressive forces and a strengthening of rightward mobilizations.

Hf: To what do you attribute the new rise of authoritarianism?

fB: After democracy was won due to the social, economic, and political failure of the dictatorial regime, we thought Brazil would never have an autocratic government again. But the world situation is not always linear, and is rather cyclical. Today, in my opinion, we are experiencing a wave of authoritarianism with a strong Nazi accent. This is happening on every continent, and is further exacerbated by the election of Donald Trump in the United States, as he is openly and avowedly an autocrat. An old joke in Latin America is that there has never been a coup in the United States because there is no American embassy in Washington. This is no longer true. The threat is now real there too. Trump tried to stage a coup d’état, and fortunately he was defeated, but now he’s back in office with massive support from the US population.

This authoritarian bias is in vogue around the world, and is due to several factors. During the Cold War, there was bipolarity, with the capitalist countries hegemonized by the United States and the East by socialism in the Soviet Union and China. This created a certain balance of forces. I believe that the greatest achievement of socialism did not take place in any socialist country, but in Western Europe: the working classes won many of their rights, guaranteed by law, because the European bourgeoisie feared that the workers would embrace the path of socialism and communism. The welfare of the working class in Europe was never as solid as it was in this post-war period lasting until 1989.

With the fall of the Berlin Wall, the world elite tore off its mask. And with the change in the pattern of capitalist accumulation from production to speculation, these elites now have much more income and power. Today, we have a world dominated, on the one hand, by speculators and, on the other, by these Big Tech companies that produce nothing, but just process our knowledge and information, turning it into merchandise and also into a force for dominating consciousness.

So I think we are in a world in which consciences are experiencing a spiritual domestication. We’ve always talked about globalization and I’ve always criticized this expression: what really exists is globo-colonization, the colonization of the planet by a system of society that is capitalist; a hedonistic, consumerist system that turns human beings into merchandise because we’re not worth our intrinsic dignity, but rather the goods we own or don’t own. The more we possess material goods, the more we are welcomed into society. There is an accelerated process of domination, causing social ties to become increasingly frayed. Union, or party relations are increasingly atrophied. There’s a strong tendency for networks to lead to individualism, because associative ties are being eroded and, at the same time, narcissism is being accentuated. The logic of social media produces both narcissistic feedback and a great dependence on these Big Tech companies that don’t exist to facilitate our communication but to sell products.

Hf: Is there a parallel between Bolsonaro and the military coup in 1964, between today and what we experienced under the dictatorship?

fB: Yes, because Brazil, unlike Argentina, Chile, and Uruguay, has never punished its torturers and murderers. On the contrary, it has created an odd mechanism from a legal point of view, which is the reciprocal amnesty. Instead of being denounced, tried, and sentenced, the torturers and murderers were granted amnesty at the same time as those who fought against the dictatorship. This meant that the culture of the dictatorship remained warm in the barracks of the Army, Air Force, and Navy. And they consider the 1964 coup to be a breakthrough, a revolution, and not the establishment of a dictatorship. Bolsonaro is the son of this strongly Nazi-like military background, just like all those who, with him, attempted the failed coup of January 8, 2023.

But today, they can’t find support in the military institutions. I don’t see any possibility of a new coup as we had before. But while Bolsonaro is ineligible to run for office, I do see the possibility of his people winning the next election in 2026, including the office of the President of the Republic. The authoritarian threat is in place. I think we progressives have to step up our work, because the risk is there. There is a tendency in Brazilian society to support this Nazi-fascism that characterizes Bolsonarism. I think this is a very big risk. So we need to get back to grassroots work and master the digital networks. We’re very reactive, we’re not proactive on digital networks.

Hf: What impact does the Trump administration have on this situation?

Fb: Trump is going to rule autocratically, ignoring the laws, the judges, as seen in the deportation of Venezuelans to El Salvador. The question is how the US judicial system reacts, to what extent it has the strength to stop him. If the mechanisms of checks and balances aren’t activated, I think that, looking at today’s scenario, he won’t be in office in four years’ time. He can’t be a candidate, but he can invent a casuistry, a new amendment to the US Constitution that allows him to be a candidate again. It’s too early to make an assessment, but I predict an extremely autocratic government, on the edge of what would be a declared dictatorship.

But all this will depend a lot on the performance of his government. Already, in his two months in office, he is creating a great deal of disappointment. Sixty days in office, and his prestige is already going down the drain. The wear and tear is already too great. The most sensitive part of the human body—the pocket—is a source of tension in Brazil, the US, or anywhere else. What will be the government’s role in people’s well-being? Food, health, education, etc., or war, arrests, and deportations?

Across the world, parties governing amid the post-pandemic rise in prices have found themselves punished at the ballot box. The seeming ubiquity of this voter reflex, which has transcended the left-right divide, translates to a political cry for help: just do something. The question, though, is what to do. The answer to this question today is unusually constrained in historical terms: interest rate increases and public-sector austerity. The example of Javier Milei is a case in point: the Argentine president took office in December of 2023 amid triple digit inflation and slashed public spending. While inflation in the country has dropped in response, the country’s poverty rate has climbed to 50 percent.

But persistent and accelerating rising prices were not unusual during the decades after World War II, and how governments should understand their cause was a central problem of politics and economic theory. The newly created United Nations understood the stakes of inflation, and in 1948 established a commission to study the roots of rising prices in Latin America and the Caribbean. Amid the birth of a Latin American school of critical economics in the years after World War II, “structuralist” economists associated with the UN’s Economic Commission for Latin America and the Caribbean (Comisión Económica para América Latina or CEPAL), argued that inflation accompanied development occurring within an imbalanced system of global trade. “Monetarist” economists, associated with the International Monetary Fund (IMF), instead blamed inflation in developing South American countries on excessive monetary expansion and fiscal mismanagement. The diverging political implications of these two interpretations were stark, lending themselves to distinct policy programs which would shape the trajectory of the region.

Margarita Fajardo, professor of history at Sarah Lawrence College, examines CEPAL and its contributions to the knowledge and theory of inflation in her 2022 book The World That Latin America Created. Her current follow-up book project considers the history of inflation (alongside commodity regulations) and its importance to the transition to a neoliberal order in Latin America. For Phenomenal World, geographer Sammy Feldblum spoke with Fajardo to understand the hemispheric history of how inflation might be mobilized for a different sort of political-economic project. The following conversation has been edited for length and clarity.

An interview with Margarita Fajardo

sammy feldblum: One of the major themes of your book is institutional personalities: how institutions of knowledge production like CEPAL came to shape Latin American economics, including the interpretation of inflation.

What is CEPAL? How did the economists employed by CEPAL come to collect and analyze data in a different way from those working on macroeconomic theory in the US in the 1950s? And what historical circumstances gave rise to CEPAL’s critiques of the global economy and the economic science developed to explain it?

margarita fajardo: Although CEPAL became eventually known as a Latin Americanized institution, we must remember that it is a UN-affiliated body. That global aspect is often forgotten, but it’s important because it gives a sense of CEPAL’s potential resources, leverage, and ideological diffusion.

Intellectually, CEPAL is best known for a few key notions that are often packed together under the umbrella term of “dependency theory.” The main contribution of the cepalino understanding of development was to place development in the context of a global political economy of countries divided between center and periphery: the industrialized centers producing manufactured goods and the periphery producing raw materials for the world markets. That international division of labor gives rise to specific political economies, specific labor struggles, and specific monetary policies. These specificities are what cepalinos identify as the source of a long-term decline in the terms of trade, impeding Latin America’s development in the long run. Given that diagnosis, cepalinosproposed two different strategies: first, industrialization that substitutes those goods previously imported from the world’s economic centers, and second, international cooperation between those centers and peripheries to make trade fairer and more conducive to the economic development of the periphery.

The book tries to unpack the notion of “dependency” and give each of the ideas within that framework its time, place, and trajectory. It’s important to really understand the differences between these concepts—and the politics behind each of them—because they emerged during distinct periods. CEPAL is known for the center-periphery framework, the structuralist approach to inflation, and then dependency theory. The center-periphery framework was rooted in the post-World War II context. The structuralist approach to inflation, which I will explain in a moment, rose in the 1950s in relation to the politics of inflation in Chile and Brazil. Full-fledged dependency theory emerged in the mid 1960s and 1970s in response to the early theory of the center-periphery structure of world production and trade, and also in response to the changing political economy in Latin America, which was considering the role of international capital and of the political forces of development at the local, national, and global levels.

Institutions, individuals, and ideas—that is the tripod in which I conceptualize CEPAL and its role. In the book, I focus on individuals that shaped the trajectory of the institution, and also how the institution and the individuals clashed and altered each other’s trajectories. Those particular individuals include Argentinian Raúl Prebisch, long-time head of CEPAL and prime mover of the center-periphery framework. Then the “structuralist approach to inflation” connected many different cepalinos, including Mexican Juan Noyola, Brazilian Celso Furtado, and Chileans Anibal Pinto and Oswaldo Sunkel. Dependency theory brought in German-American Andre Gunder Frank and Brazilian Fernando Henrique Cardoso, just to name a few.

There are also those who participate in the dependency framework and are not linked to CEPAL. The confluence of these institutions, ideas, and individuals is what led to the rise and transformation of what I call the cepalino project.

sF: You note that the structuralist approach to inflation arose in the 1950s, but earlier, in the case of Chile for example, there was a policy of tolerance to inflation. Why and when does inflation come to be seen as a threat to economic development and social peace, and how does that figure into the initial period of cepalino thinking?

MF: The structuralist approach to inflation rescued and redeployed that foundational framework of CEPAL. Chile, the headquarters of CEPAL, greatly influenced the institution. The country had experienced long-term double-digit inflation, though not hyperinflation, for decades. In that context, inflation came to be assumed as the cost of development, or the accompaniment to growth. But there was a point in the 1950s when that consensus started to break. Why? Perhaps it has to do in part with the stagnation of development. When development and inflation coexisted, the latter was tolerated. But once development started faltering while inflation persisted, the search for new explanations for inflation began.

Cepalinos, like everyone else, initially thought of inflation as driven by costs: wages that increase above price levels that then are translated into prices. This creates a wage-price spiral that is transmitted to the rest of the economy. As development faltered and labor struggles over real wages intensified, some cepalinos worried that the wage-price spiral was not only unable to explain the rise in prices, but that it also fueled the fire of conservatives, who did not want to concede on those labor struggles by lowering profits or engaging in some form of redistribution. As cepalinos debated the sources of inflation in Chile among themselves, they were also thinking in relation to another big institutional actor in Latin America, the IMF. There, we can see the growing split between the structuralist and monetarist approach to inflation.

Cepalinos considered not only the amount of money in circulation, but also the structural factors affecting inflation, including the international economic structure, land tenure regimes, and balance between the different sectors of the domestic economy, among others. They argued that the international division of labor between raw-material producing peripheries and the industrial center—and the falling terms of trade for the former—made imported goods costlier, both hindering development and promoting rising prices. Similarly, the land tenure system, with its large, idle landholdings, made foodstuffs and agricultural products expensive or unavailable, turning countries towards imports amid a shortage of foreign exchange. As cepalinos debated the causes of inflation, they gave rise to the structuralist approach to inflation in the 1950s, which was eventually recast as the antithesis of the monetarist approach to inflation ascribed to the IMF.

sF: Can you elaborate more on these distinct approaches to inflation? What kind of policy program does each approach put forward?

MF: The structuralist approach tries to understand inflation as a product of development, meaning that the economic development in this postwar context was driven by demand for imported capital goods required for industrialization. This meant that development, the industrialization process, required imported capital goods which—given the shortage of foreign exchange and falling prices of exportable commodities—created inflationary pressures. This approach differentiates between the structural causes of inflation and inflationary pressures like wages.

The response required sustainable and accelerated development to break the bottlenecks that lead to inflation. If there’s not enough food, and food needs to be imported, then prices can rise. If we need to import capital goods, then we can either develop the capacities to manufacture goods ourselves, or we can create stable foreign exchange flows by stabilizing the prices of commodities to lower those inflationary pressures. The toolkit of the cepalinos, or the structuralists, sought to foment development through international cooperation in order to manage inflationary cycles. This would prevent the rapid adjustments in income required to control inflation, instead using international cooperation to soften those effects and have a less detrimental impact on the population.

The monetarist explanation of inflation has to do with the quantity of money available in the market, the source of which is private banks, the central bank, and the government treasury. The solution has to do with controlling that money supply: central bank regulations and cutting fiscal expenditure.

The structuralists think of inflation as a cost of development. The monetarists think inflation impedes development. Monetarists think that if the problem of inflation can be solved, then development will follow.

sF: How important is this split in driving the dependency theorists’ criticism of CEPAL more generally? I’m thinking specifically of the structuralist criticism of Raúl Prebisch’s stabilization plan in Argentina in the 1950s.

MF: Initially, the structuralist and monetarist approaches were not exclusionary paradigms. They could concede points to the other side. But over the course of stabilization plans in both Chile and Brazil, the political debates became heated. The paradigms of CEPAL and the IMF became more polarized. CEPAL was the “International Monetary Fund of the left,” a toolkit and institutional fulcrum to challenge the policies of the IMF. Certain cepalinos like Prebisch would say that such an oppositional approach would actually undermine an understanding of the true social costs of inflation.

The confrontation between structuralists and monetarists positioned cepalinos on the left of the polarized political contests in Latin America, especially as a result of the Cuban revolution. But also, while some cepalinos sided with the Cuban revolution, others trusted the Alliance for Progress, the US counterrevolutionary response to Cuba, as a solution for accelerating development. The alignment of CEPAL vis-a-vis the Cuban Revolution and the Alliance for Progress led to criticism from dependency theorists, who, in response, sought a different model. For some dependentistas, CEPAL’s institutional rupture with Cuba signaled that the organization was complicit with imperialist forces and thus an agent of underdevelopment.

sF: In 1970, Salvador Allende gave dependency theory-adjacent Pedro Vuskovic wide leeway to implement a program of economic planning in Chile. How does Vuskovic approach inflation while in power? How does the resulting high inflation under Allende spark backlash to the regime?

MF: I don’t know if Vuskovic would call himself a dependentista, but I do think he was very much influenced by dependista ideas, and he was a member of the Socialist Party. He implemented a plan to accelerate development through granting subsidies, raising wages, and promoting industrial growth. That push towards development initially worked.

There were many different factors at play, so it’s hard to tell in the Chilean case why exactly that approach failed. Did it have to do with sanctions, or domestic and international sabotage, or the failure of these policies in and of themselves? In any case, production didn’t increase at the pace of demand. That resulted in a shortage of goods which eventually translated into rising prices and the emergence of a black market. It was hyperinflation that marked the failure of the Allende project.

sF: In thinking about the struggle between the contrasting interpretations of inflation, Fernando Henrique Cardoso presents an interesting case. He was straightforwardly a dependency theorist and to the left of CEPAL in the 1970s. By the time he came into power in Brazil the ‘80s and ‘90s, he implemented stabilization plans that were part of a broader neoliberalization of the Brazilian economy. What does this say about the trajectory of dependency theory more broadly?

MF: The case of Fernando Henrique Cardoso, one of the pioneers of dependency theory, allows us to see how we move from state-led development to the neoliberal state and the neoliberal order. I think there’s some consistency in his transition despite the drastic change. His critique of dependency theory emerges from his critique of the developmental state, which he saw as a populist alliance between workers, industrialists, and the state. That critique persists as Brazil turns from a developmental state under authoritarianism to a developmental state under democracy. Throughout his career, Cardoso tries to understand and unravel the state as an economic actor—the role it should and shouldn’t play. These are the main questions of his intellectual and political project.

sF: Because dependency theory has an anti-imperialist ethos, it remains popular among Marxist intellectual historians and much of the left. Yet the world economy it describes has evolved considerably in terms of industrial structure and the international division of labor. What do you think about the accomplishments, limitations, and legacy of Latin American structuralism and dependency theory today?

MF: One of the meanings of dependency theory that has perpetuated over time is its ability to point to the insertion of Latin America in the global economy as the reason for many of the economic, social, and political difficulties that the region faced in the mid-twentieth century. That critique was embedded in cepalino thinking from the start. The contribution of dependency theory is interrogating the relationship between the global economy and the internal structures of power, and the balance between those different social actors. I think that dependency theory could be used again to identify those local forces, the internal political structures of power that work with external global forces to perpetuate or challenge a specific model of development.

While the world’s attention was focused on the United States presidential election that would deliver Donald Trump a decisive victory and a second Presidency, Brazil’s municipal elections in October were signalling the political balance for the coming years within the second largest country in the hemisphere. Elections for city council and mayoralties take place all on the same date, and—much like the Congressional midterms in the US context—are often read as an indication of the health of the ruling government’s support, and weigh heavily on intraparty disputes over strategy for incumbents and opposition alike. In São Paulo, Latin America’s largest city and Brazil’s largest single electorate, some trends asserted themselves: namely, the concerted success of centrist forces to defeat the favored candidate of the left, and the surprising rise of a non-Bolsonarista far-right candidate in Pablo Marçal.

To discuss the election results and Brazil’s current position on the global stage, PW editor Hugo Fanton spoke with political scientist André Singer. The wide-ranging interview addresses Singer’s recent writing on Brazilian party politics, class structure and political behavior, varieties of autocracy, and striking similarities between the United States and Brazil. Singer is Professor of Political Science at the University of São Paulo (USP), former spokesman for President Lula Inacio da Silva (2003–2007), and the author and editor of numerous books, including O segundo círculo: Centro e periferia em tempos de guerra,released in Brazil last September.

An interview with André Singer

Hugo Fanton: Pablo Marçal’s performance in São Paulo’s mayoral election drew nationwide attention. Who is Marçal, and what does his candidacy tell us about the Brazilian political scene, and the prospects for the 2026 presidential election?

André Singer: Pablo Marçal, an internet influencer, was completely unforeseen by the major political players. He came out of nowhere, backed by a political party that has no representative in the National Congress, and yet secured 1,700,000 votes. It was an extraordinary result in the most important electoral contest of the year: the city of São Paulo. By a difference of just 50,000 votes—a very small margin—he didn’t make it to the second round. In addition to the general shock, Marçal’s success exposed unforeseen issues on the right of the political spectrum: a young man, thirty-seven years old, with no support other than his own communication skills, was able to mobilize São Paulo’s far-right electorate away from former President Jair Bolsonaro. Marçal became a far-right figure, independent of Bolsonaro and his chosen candidate, the Brazilian Democratic Movement (MDB) candidate, as well as the city’s incumbent mayor, Ricardo Nunes.

In order to get re-elected, Nunes nominated a Bolsonaro appointee as deputy mayor, confirming that there was a formal alliance not only with Bolsonaro’s Liberal Party (Partido Liberal, or PL), but with Bolsonaro himself. Once Marçal began to climb in the polls, Bolsonaro found himself in a difficult situation. At first, he tried to disqualify Marçal in order to boost Nunes’s campaign. But this backfired, and Bolsonaro’s own supporters forced him to retreat and reconcile with Marçal. This shocking grassroots defection seriously threatened Nunes’s prospects.

In that moment, I believe, it became clear that the main winner of the entire 2024 electoral process was São Paulo state governor Tarcísio de Freitas. Tarcísio supported Nunes’ candidacy and was in debt to Bolsonaro, who made him his gubernatorial candidate in 2022 and delivered him a victory on the back of his strong base in the countryside. Now, two years later, in the middle of this situation, Tarcísio found himself faced with a decision: to stand with Nunes, or with Marçal and Bolsonaro. Tarcísio opted for the former, saving Nunes’s bid for re-election, which eventually caused Bolsonaro himself to retreat from supporting Marçal and take a more or less neutral stance. Tarcísio, despite opposing Bolsonaro and Marçal, asserted throughout that the former president needed to come back to Nunes—understanding that if the right unified, it would be competitive.

Tarcísio represents what I called “Shrek-like Bolsonarism” in a recent article for piaui: a right-wing politician that seems friendly in contrast with extreme figures like Bolsonaro and Marçal. He is a hybrid figure who is originally from the monstrous extreme right but presents himself in a more palatable way for the non-extreme right. Mayor Ricardo Nunes has the same profile. He does not appear as an extreme right-wing figure, but embraces several of their slogans and pursues unity across the right.

São Paulo’s municipal election was widely covered in the national media and can be viewed, relatively speaking, as a preview of elements that may return in the 2026 presidential elections. Of course, Brazil is different from São Paulo and there should be no automatic transposition. But some of what happened here may prove useful in understanding certain elements of 2026. The 2024 election demonstrated the power of the far right after its defeat in 2022. It was the first time that the far right returned to the polls, after Lula’s victory and Bolsonaro’s exile from the electoral system, and it proved to be powerful—not enough to win, but enough to compete. Crucially, it proved that if there is unity, the right can win the election.

HF: The parties that performed best in these municipal elections are called the partido do interior—parties of the interior, or rural areas in Brazil. These are parties like PMDB, PSD, and so on, which perform well in the local governments of the countryside and are closely associated with regional elites. What does their success reveal about the traditional right wing and the Bolsonaro coalition? Is there a realignment taking place?

AS: In 2006, I described an electoral realignment that had taken place through the election and government of the Workers’ Party (PT).1 That realignment was characterized by the decisive shift of the bottom of the social pyramid—households earning zero-to-two times the minimum monthly income—from the array of Brazilian parties and toward a strong alignment with Lula and the PT. This fundamental alignment is still intact. Datafolha’s assessment of Lula’s government at the beginning of October is an indicator of this: 36 percent of the electorate as a whole rate his government as “good and excellent.” But at the bottom of the pyramid, this proportion rises to 46 percent. For everyone else who isn’t at the bottom of the pyramid, it’s around 27 percent. That’s a big difference. It’s as if the country were divided into two blocs, two great social halves, with the bottom half supporting the government and the top half tending not to support it. Numbers like this lead me to believe that Lulism is still standing. Another element that points in this direction: the only major victory for the PT in the municipal elections was in Fortaleza, one of the main Northeastern capitals, which is the center of the subproletariat, that fraction of the class that is technically at the bottom of the pyramid. So, in that sense, the alignment from the early-2000s remains. What is new, however, is that there is a shift within the middle class from the point of view of party identification, which began with the depletion of the Brazilian Social Democratic Party (PSDB) and the migration of these sectors to the extreme right from 2016 onwards.2

One of the ongoing factors—which was also very apparent in the 2024 municipal election—is Bolsonaro’s attempt to build up a party to organize and replace the PSDB, and that is the PL. Bolsonaro first joined the Social Liberal Party (Partido Social Liberal), which he left while in office. Then he launched his own party, which was abandoned along the way and dissolved. Finally, he joined the Liberal Party which had been around for a long time, and whose top leader was willing to become the main organizer of Bolsonarism. Therefore, Bolsonarism now has a party vehicle that did well in the elections. It’s the party with the most state resources for campaigning, because it holds the largest caucus in the Chamber of Deputies, and it did very well in October.

However, this comes at a price: like any force that joins the institutional game for real, there is a normalization effect. Somehow, it is drawn into the implicit or explicit rules of the electoral game. The implicit rule in the Brazilian case is that these parties need to behave like what former President Fernando Henrique Cardoso, when he was just a political scientist forty years ago, called a partido ônibus, or “bus party”—meaning you can join and leave at any time, and the parties don’t necessarily have a homogenizing influence on their members, such that regional and local sections can bear very different characteristics. This “bus party” form leads to some very odd cases, like local alliances between the PL and the PT. It’s rare, but it has happened—just to give foreign readers an idea of the complexities of Brazilian party politics.

The PSDB was partly replaced by the PL, but also partly by the Social Democratic Party (PSD), which is led by a very traditional politician, Gilberto Kassab. In São Paulo state, especially in the countryside, the PSD has absorbed the old PSDB machine, a very strong structure in a very powerful state. As a result, we’re witnessing a reshuffling of the right of center. On the one hand, the extreme right has acquired a party apparatus with some robustness; while, on the other, there is the strengthening of a party from the so-called centrão—the large, ideologically thin, and highly transactional group of parties that make up the center of Brazilian politics. The PSD, a partido do interior, is a more moderate force that has grown in size with the potential to dominate the centrão. The right’s problem is whether it will be able to produce an alliance between the PSD and the PL. In the elections in São Paulo, the right and the far right were separated in the first round but combined in the second. The question is whether they can do this on the national stage in 2026.

So what uncertainties hang over the election next year? Firstly, whether Bolsonaro will insist on being a candidate, even though he is legally barred from running. There are several signs that he will run, and in this he would mirror what President Lula did in 2018 while facing a prison sentence for now-annulled corruption charges: he waited until the very last moment to acknowledge that he could not be an eligible candidate and nominated Fernando Haddad to run in his place. If Bolsonaro does this, it will create problems for alternative candidates. For example, if Tarcísio wants to run, he will need to build his name nationally, which requires mobilizing earlier rather than later. But to do so would mean stepping into the open and confronting Bolsonaro, thereby contradicting one of his premises: the right will lose if it is not unified. Tarcísio’s problem is this equation. The second major uncertainty is whether Marçal or a candidate like him would have a chance of reproducing, on a national level, what happened in the city of São Paulo. It’s a very difficult question, because Brazil is not São Paulo. Brazil is a giant, heterogenous country, with a wide range of different characteristics across region, religion, age, gender, and so on. But it’s not impossible, as demonstrated by the previous phenomena of Jânio Quadros, Fernando Collor, and Bolsonaro himself.

HF: Can you say more about the relationship between these shifting political forces and the country’s class structure?

AS: I’m going to start from the bottom up and talk about four population segments. First, there’s the base of the pyramid. As I said before, looking at this section shows that Lulism still stands. For example, one of the most significant victories in Brazil was that of João Campos (Brazilian Socialist Party, or PSB) in Recife, who was leading the coalition that supported Lula in 2022 and who was supported by Lula now in 2024. Recife is one of the largest cities in the poor region of the Northeast, and historically the home of many national political leaders. We’ve already talked about the PT’s victory in Fortaleza, also in the Northeast, and then there’s Eduardo Paes’s (PSD) triumph in Rio de Janeiro, where, with Lula’s support, the winning coalition inflicted a defeat against Bolsonaro in his political stronghold. This is no small feat, as Bolsonarism remains very strong in the South of the country, where it won in all three capitals, and obtained expressive victory in the Central-West, in addition to its performance in some capitals in the Northeast. Nevertheless, the election and the polls show that the base of the pyramid still remains with Lulism.

The second tier is what social scientists refer to as those with a monthly family income ranging from two to five times the minimum wage. Here, a sharp divide begins. Marçal’s candidacy in São Paulo had a significant advantage in this group, although it was not his core support, which was among higher-income voters. Support for the far right increases up the income ladder. It was the same with Bolsonaro: the higher the income in these middle sectors, the more they oppose the base of the pyramid. In this respect, it is a class opposition to Lulism. From a social point of view, this is the fundamental clash at play. Those earning from two to five minimum wages are very important from a numerical point of view, representing more than 30 percent of the Brazilian electorate, while over 40 percent of the electorate remains at the bottom at two times the monthly minimum or lower. These two segments decide the election, as rich Brazilians don’t have the numbers to be decisive. But the two to five wage sector is divided. The extreme right does hold sway there, but it remains under dispute, and I would even say that this is the sector that will decide the election in 2026.

Next, we have the third tier, made up of those with a monthly family income above five minimum wages. Here, too, there is a threefold split: the far right, the right, and a small middle-class progressive fringe. The left-wing candidate in São Paulo, PSOL’s Guilherme Boulos, who was backed by Lula, faced difficulties at the base of the pyramid, but his support grew in the third tier—somewhat similar to the distribution that the PT could achieve until its breakthrough in 2002.

Finally, the fourth tier would be the dominant classes, who don’t even feature in opinion polls. They are not important from a numerical standpoint, but from a class structure perspective. It’s clear that part of the ruling class supports the extreme right, particularly in the agribusiness sector. The PL, for example, did very well in the cities with the highest agribusiness revenues—where that sector determines employment and is politically integrated in local government. This is also true among those in business and construction, which are economically important sectors. The major question is what the cosmopolitan bourgeoisie will do, given that it was difficult to get them to side with Lula in 2022. The bankers, financiers, and cosmopolitan business elites backed Lula’s candidacy in an environment of considerable tension, and the subsequent two years in office have been marked by a central governmental dispute: the problem of austerity. This sector of the bourgeoisie wants public spending to be cut, ostensibly to create a fiscal balance that will generate peace of mind for investors. Their support for Lula is accordingly very fragile, so a right-wing candidate seemingly without extreme right-wing characteristics could emerge and appeal to this cosmopolitan bourgeoisie.

HF: You’ve written about the idea of “autocracy with a fascist bias” to understand the phenomena of Trump in the US and Bolsonaro in Brazil. Could you explain this idea, and how it helps us understand the election of a more radicalized Trumpist movement in the US, the Marçal phenomenon, and the impacts of Bolsonaro’s ineligibility?

AS: From an empirical perspective, what we saw during the Bolsonaro administration was a tendency toward an autocratic regime—in a specific sense, it aimed at consolidating governance around Bolsonaro himself. This is unlike, for example, what became known as the techno-bureaucratic military regime of 1964, which had no prominent leadership and instead organized around an apparatus. By “autocratic” I mean something very particular because, by contrast, we don’t have any empirical evidence to say that he was moving towards a fascist-type regime. The fascist bias lies in having activated, or perhaps having sought to activate, the unconscious of the masses. Following the Frankfurt School’s analysis of historical fascism, communication that can activate this unconscious across class divisions are part of the “delusional system” of right-wing nationalist and fascist politics. There are many episodes of this kind of irrational, mass, communications-driven far-right movement in recent history. To give one example, in 2021 Bolsonaro’s networks started spreading the word that most of the Supreme Court (STF) ministers were receiving Chinese money to enable the legal rehabilitation of former president Lula and thereby enslave the Brazilian people to China. This was spread not as a metaphor, but as a fact. And this fact is completely delusional, outside of the realm of logical dialogue. This didn’t exist in Brazilian politics until Bolsonaro came along. It’s a novelty that typifies what I call the fascist bias.

My analysis is for Brazil, but since the question has been posed, I’m risking an opinion on the United States. From a distance it seems to me that Trump’s victory last November took place amid an intensification of this fascist bias. The promise to deport millions of people and fables about Haitian migrants eating pets in the middle of the country take part in this delusional system. This newfound phenomena presents us with challenges we aren’t accustomed to in political analysis, so it’s difficult to predict what will happen when Trump takes office, but I would expect a further deepening of both authoritarianism and this fascist bias.

Back to Brazil, it’s my view that the fascist bias was fully at play in Marçal’s campaign in the São Paulo election. It was an extremely aggressive candidacy, characterized by vicious attacks on other candidates, and viral falsehoods. He was so offensive and provocative that, in a televised debate during the campaign, another candidate hit Marçal with a chair. The scandal became known as cadeirada, roughly meaning “chairing.” In a subsequent debate, one of Marçal’s advisors punched another candidate’s publicist. Generally perceived as random explosive moments, these events were rather, in my opinion, part of a communication strategy: acts of expressive violence that activate the unconscious of the masses. That’s why the Marçal phenomenon is very significant—it represents the existence of a social environment for this type of politics.

HF: You launched a book last September, The Second Circle (O segundo circulo), which seeks to place Brazil in the world. Where does the country stand today compared to the early 2000s? How do you view Brazil in the context of increasing competition between China and the US?

AS: As a peripheral country, Brazil is subject to determinations coming from the center of the global system, but at the same time it processes these determinations through its domestic dynamics and class structure. As Professor Fernando Rugitsky has argued, Brazil’s position in the global trade system is primarily as a supplier of roughly processed raw materials for industrial use in Asia. Brazil is once again the breadbasket of the world—or a part of the world, at least. Meanwhile, the third corner of this triangle, the United States and Europe, dominate the financial and currency system in which Brazil is a subordinate party. What we don’t know is whether or not the polarization between the US and China will lead to Chinese and US-European industrial investment in Brazil. So far, there have been some Chinese industrial investments in the country, such as the BYD and Goldwind plants in Camaçari (both of which used to house American industrial giants, Ford and GE). These investments do not seem to be on a scale that would suggest structural change or a reversal of the trend towards deindustrialization. Nor, so far, have I heard about the transfer of advanced technology, which is essential if we are to think about the possibility of reversing this trend. The same question applies to the bloc led by the US in opposition to China, because Brazil, as an important country on the international stage—diplomatically and economically—could benefit from this division by negotiating concessions from both sides that point in the direction of what is a historical project for part of Brazilian society, which is to seek a definitive exit from so-called economic backwardness.

Compared to the early 2000s, when Lula won the first presidential election, Brazil is significantly more deindustrialized and reprimarized. This partly explains the reason why the Bolsonaro coalition was defeated in 2022 by a margin of less than 1 percent of the vote, despite the humanitarian catastrophe that was Bolsonaro’s management of Covid-19. There is also the further transformation of a country toward services rather than industry, something that has everything to do with Bolsonarism, which brings together ruling class groups linked to agribusiness and services. So today, from the standpoint of a development project, the situation is far more difficult than it was twenty years ago. Precarious work, superexploitation of the workforce, the progressive growth of organized crime—these are the trends from the point of view of income redistribution and the lower classes. The problem of how to organize a new program in this situation is, I would say, one of the most distressing questions of the moment.

HF: You write in this book about parallels between Brazil and the United States, about a “mimicry” across the politics of the two countries. Can you outline the main aspects of this parallelism and its implications for understanding Brazil in the world?

AS: We started with the observation that, since 2016, Brazilian politics has begun to resemble American politics. At the first level, former president Jair Bolsonaro began to literally copy all of Trump’s actions, culminating in the uprising of January 8, 2023, in which a Brazilian crowd invaded and vandalized the headquarters of all three branches of government in Brasilia—mimicking January 6, 2021 in Washington DC. This was a kind of mimetic performance, with extraordinary consequences, because many of these people are in prison to this day, paying a very high price for the delusional rallying cry that led them there.

The philosopher Roberto Mangabeira Unger says that there is no country in the world more like the United States than Brazil: the extent of the isolation of the two countries, both continental in size, both inward-looking and insolated. It is worth remembering that Brazil also has a historical tradition of turning its back on the rest of Latin America, and looking first to Europe and then to the United States. It is also the case that Brazil has historically copied other US formulas, notably the adoption of presidentialism (although this is true for several other countries in the region as well). But finally, and perhaps most essentially for our discussion, both countries have been deindustrializing in parallel.

Of course, the United States is the center of the system and Brazil is a peripheral country—the starting points are different, and the place of the two countries in productive and financial chains are different. But, curiously, both countries have been experiencing parallel consequences for neglecting domestic industry. Deindustrialization is the starting point for thinking about the strange underlying resonances in the political realm, despite immense differences in social composition, political system, and so on.

HF: What are the prospects for Lulism and left-wing politics in Brazil?

AS: Contextually speaking, I see three major challenges. The first is the fact that budget cuts in programs that provide income and benefits to the base of the pyramid could have a fatal effect on Lulism, which is built entirely on the provision of this support. Possible cuts in the minimum wage, in the Continuous Benefit Program, in salary bonuses, which affect the base of the pyramid directly, need to be carefully observed from a political standpoint. Secondly, there is a perception, common to both the United States and Brazil, that the increase in the cost of living is impacting the base of the pyramid and also the next tier up (the two to five minimum wage monthly family income group), meaning that aggregate economic figures seem to be of little importance on the scale of elections. We may observe economic growth, a drop in unemployment, and an increase in wages, but when surveys are carried out, pessimism about the economy even increases, which seems to suggest that, for ordinary people, life is still very difficult. And this may have something to do with the surge in inflation in the cost of living worldwide, due to the disruption of production chains during the Covid-19 pandemic and perhaps later the wars, as oil and energy prices have a huge impact on the entire price chain and, in particular, on the cost of living. So the second challenge is to design policies to protect the popular economy, to prevent the effects of the global economy from reaching the lower income strata. The third, and most difficult, is to draw up a program that makes it possible to attract this group of voters who receive between two and five minimum wages monthly, who are not at the bottom of the pyramid, but who are workers dealing with precarious incomes and all that come along with them. For example, an app delivery driver who works on a motorcycle in the city of São Paulo is not at the bottom of the pyramid—in the Brazilian case, he is in the middle sector and not among the poorest. What project can fight for this electorate, which has proven quite inclined to support Marçal in São Paulo? It can’t be anything other than a national development plan. But how can we think of a development plan in the adverse global conditions I described earlier? To end on an ironic note, I would say that we need to do this now. But how? I don’t know.

HF: In the first chapter of the book, you defend the use of the word “interregnum” to think about the global crisis. Could you comment on the analytical value of thinking in these terms?

AS: The purpose of the article is to reflect on the notion that interregnum, for Gramsci, means a period of struggle between forces that don’t have hegemony, but seek it. It’s not just the idea that chaotic periods lead to a new settlement. We take a very political angle of looking at the interregnum as a period of dispute between these forces. From our vantage point, we sought to interpret the Biden phenomenon as an attempt to create a new, organizing vision of Americanism. It’s not clear to me that all of these attempts have been lost with the electoral defeat, but it will now be replaced by Trumpism, seeking to put forward a counter-direction to resolve the same set of problems. For example, there are a number of analyses that point to the very difficult living conditions of the average American citizen, not to mention citizens at the very bottom of the US’s own class pyramid. How will Trump deal with this? In global terms, the competition over the new hegemony is taking place in two directions—inwardly and outwardly. For Biden, this was attempting new domestic economic policy while pursuing belligerent foreign policy. When it comes to China, the focus must be on what it is proposing for the global South, and at the same time, for its own domestic economy. Thinking about the “interregnum” is about focusing on the direction of these forces, in a moment when there is no defined hegemony.

This interview was translated from Portuguese to English by Marina Vello.

Since 1999, the European Union (EU) and Mercosur have been negotiating a bi-regional partnership agreement comprising three pillars: trade, cooperation, and political dialogue. A quarter century later, in December 2024, the parties announced the conclusion of negotiations during the Mercosur Summit in Montevideo, attended by European Commission President Ursula von der Leyen. Before implementation, the agreement will undergo legal scrubbing for national ratification processes. The European Union has opted for a split approval: the trade dimension of the agreement requires only European Parliament approval, while political and cooperation aspects must be submitted to national parliaments. Within Mercosur, though each country’s parliament must ratify the text, the agreement can take effect bilaterally between the EU and individually approving Mercosur nations.

A previous version of the deal was announced in 2019, under the Mercosur leadership of Jair Bolsonaro. Latin America abandoned those negotiations after the EU introduced new environmental regulations. While Bolsonaro opposed these measures, they were also widely viewed throughout Mercosur, including by progressive factions, as protectionist on the part of the Europeans. Negotiations resumed in 2023 with Lula’s new term. Although more moderate, the new text still faces criticism from organizations and governments on both sides of the Atlantic.

In the European Union, resistance comes primarily from agricultural sectors in France, the Netherlands, and Poland, which fear competition with Mercosur’s producers. In South America, concerns arise mainly from civil society and academia, centered on the agreement’s potential to undermine current reindustrialization efforts within Mercosur countries, reinforcing their export profiles focused on primary goods. Compared to 2019, the current version maintains greater freedom for the national implementation of public policies and public procurement requirements, enhanced environmental commitments, new review and “rebalancing mechanisms” in the case of disputes, and extended deadlines for trade liberalization or tariff removal in certain sectors.

Phenomenal World’s senior editor Maria Fernanda Sikorski spoke with Marta Castilho, professor of economics at the Federal University of Rio de Janeiro and coordinator of the Research Group on Industry and Competitiveness (GIC-UFRJ), about the agreement’s perspectives for Mercosur—and Brazil, in particular—and the risks of trade liberalization for South America’s national and regional development. The conversation has been edited for length and clarity.

An interview with Marta Castilho

Maria Sikorski: Could you describe how the political and economic environment evolved during the partnership’s negotiation period, from 1999 until its conclusion in 2024? Why did the agreement remain relevant, and how did EU-Mercosur trade relationships change during this time?

Marta Castilho: When negotiations began, the European Union was a bloc of fifteen member states. Mercosur had aimed to gain preferential access to the European Union over Eastern Europe, which then had industrial structures relatively similar to ours. Eastern Europe, however, eventually became closely integrated with Western European industry. This might have been the most significant change since negotiations began, at which time the horizon was a little more encouraging to our industry.

Since the beginning, Mercosur saw an opportunity to increase exports of agricultural products. Domestically, the agreement was supported by interests linked to agribusiness, while industrial sectors took a more cautious approach, advocating for a gradual trade opening as they feared increased competition from European manufacturing.

Additionally, it was important to consider that European companies maintained a strong presence in the region through multinational subsidiaries, and their positions had, let’s say, “mood swings” throughout negotiations. For example, one of the world’s largest poultry producers, a French company with operations here in Brazil, initially supported trade liberalization because their aim was to raise chickens in Mercosur and export the meat to Europe. This is in contrast with current objections coming from France. Similar shifts occurred across various sectors. The automotive sector is another significant example, as is the chemical sector and its various subsectors, due to the strong presence of European companies in our region. In general, Europe showed great interest in opening Mercosur’s industrial products market and facilitating service flows. In contrast, there was stronger resistance to agricultural product imports.

MS: An earlier version of the agreement announced in 2019 never received European Parliament ratification. What are the main changes in the current text?

MC: One relevant factor is that in the five years between 2019 and 2024 the Covid-19 pandemic happened. By 2019, European countries were already signaling a return to industrial policies, with new strategies focused on “Industry 4.0,” digitalization, and related areas. The pandemic exposed some of these countries’ vulnerabilities, leading them to explicitly adopt policies targeting localized production and reducing foreign dependency in specific sectors and segments. This shifted the EU’s trade interests in the agreement and the overall negotiating conditions between the blocs.

The shift particularly affected the interest in minerals, especially critical minerals. Mercosur is extremely rich in mineral sources—in this regard it is a paradise. One of the most recent shifts is Europe’s increasing attraction to the region’s minerals. The EU has taken a dim view of any initiative inside Mercosur countries to protect or tax these mineral exports, but Mercosur has been strategic about the critical minerals sector, ensuring the possibility of imposing conditionalities.

In Brazil, there is an ongoing debate about this matter. The discussion is not closed, and perspectives vary, for example, between the government of the State of Minas Gerais and parts of the Federal government. The discussion centers on developing a strategy for critical minerals beyond its exploitation and export as raw material, to focus on increasing processing capacity and, ultimately, manufacturing batteries and other goods domestically.

Another change between the 2019 and 2024 texts concerns public procurement. Mercosur secured the right to use this mechanism as a productive development policy. While Europe has long employed public procurement, the 2019 agreement eliminated the possibility of Mercosur using certain mechanisms. Mercosur managed to renegotiate this, bringing the agreement’s terms much closer to the bloc’s existing rules. This was one of the most positive aspects of the renegotiation.

MS: What are the implications of separating the agreement’s trade, political, and cooperation pillars, given that trade provisions take effect after the approval of European Parliament and Mercosur national parliaments, while political and cooperation clauses require approval from each EU national parliament?

MC: The partnership agreement follows a European tradition of handling non-trade aspects in negotiations of this nature, unlike the Anglo-Saxon tradition, for example. This is the reason why the EU-Mercosur agreement has a trade component, a cooperation component, and one for political dialogue. This is a positive aspect of the agreement because, for example, cooperation provisions could compensate for certain trade-related losses. Trade opening can be compensated by prospects for cooperation in technical development in areas in which Europeans are more advanced, such as technology, and in fields where we can exchange, like bioeconomy and tropical medicine.

Now, for pragmatic and strategic reasons, the agreement has been split up. This is because a trade agreement is easier to negotiate and approve. The procedure, even within the EU, is faster: if it’s just the trade portion, it doesn’t require approval from all member-state parliaments but only the European Parliament. A comprehensive partnership agreement would need to go through all national bodies—a process that could be delayed by the disagreements we’ve seen in France, Poland, and the Netherlands, for example. For the Europeans, it’s a pragmatic matter. But for Mercosur, in my view, it’s short-sighted, as the bloc misses the opportunity to benefit from potential gains that would be made possible by other aspects of the agreement, especially cooperation.

MS: Because it is possible that only the trade agreement obtains approval while other pillars remain indefinitely postponed.

MC: Precisely, because there is no incentive to approve. You won’t put to a vote something you know won’t be approved. European interests are already covered by the trade agreement. For example, some environmental rules added to the current text—such as the Carbon Border Adjustment Mechanism (CBAM) for disputes and the reforestation mechanism—do not affect the main European legislation: they are exempt from the trade agreement.

MS: Let’s discuss the trade agreement’s key aspects and their impact on different Mercosur sectors. Can we start with the part about tariffs and tariff rate quotas?

MC: The trade agreement covers various regulatory domains. One of them is tariffs and tariff-rate quotas—quotas are technically non-tariff barriers, but they are typically addressed together. The quotas are largely used for agricultural products: a lower tariff is applied for a certain amount of exports within the agreement, and anything exceeding this quota is charged with standard partner-country rates. Mercosur countries adopt a common tariff for agricultural products. The current agreement maintains an array of tariff-rate quotas from the 2019 text. Certain products see increased quotas and reduced in-quota tariffs. In other situations, the in-quota tariffs were reduced, but the established quota is lower than the amount we were already exporting in 2019 and 2020. Moreover, there are mechanisms which allow Europeans to review these quantities—another preserved aspect of the 2019 text. While Mercosur may gain improved access to the EU agricultural market, trade liberalization is not as impactful as some sectors hope or proclaim.

MS: Considering the volume of our current exports?

MC: Exactly. But some segments will benefit. Take beef producers, for example—it’s no surprise that French farmers are highly reluctant, as beef is one of the products receiving expanded quotas and reduced tariffs. Rice was one of the products for which both quotas and tariffs on imports into Europe were reduced. There are various situations among agricultural products.

MS: What about Mercosur’s industrial goods?

MC: That’s our biggest problem, for several reasons. European tariffs on industrial goods are already quite low: in general, they average around 5 percent, while ours will settle near 13 percent. Potential tariff reductions by the Europeans on our exports there are modest and Europe’s existing trade agreements with other countries further limit our preferential margin. On top of that, there’s a significant asymmetry, both in terms of competitiveness and scale of our industrial sectors. While we lack the competitive advantage to significantly penetrate European markets, their potential gains from trade liberalization are much greater.

MS: The general perception in critical assessments of the agreement suggests that Mercosur’s agribusiness would benefit significantly while industry would struggle. But from what you are saying, the agricultural sector doesn’t necessarily gain that much, except in specific products.

Given this scenario, what implementation conditions would help South American industry benefit, or at least mitigate negative impacts of competition with European industry?

MC: The trade and tariff liberalization is already set and will likely be implemented. What this means is that, in trade terms, there’s little to be done. On the one hand, we need to enhance domestic industry productivity and competitiveness—and that’s our own responsibility, which involves conceiving industrial and productive development policies, making strategic use of public procurement, and implementing technological policies. On the other hand, we can also make use of certain adjustment mechanisms within the agreement, such as the rebalancing mechanism. The revised text added certain safeguard mechanisms against occasional surges of products and abrupt inflows in specific sectors. While specific instruments await definition, at least the deal preserves adaptation possibilities.

Nevertheless, competition between our industrial production and Europe’s remains inevitable. What we can do is leverage available domestic tools to enhance our industrial competitiveness, while utilizing both national and agreement-based trade mechanisms.

MS: Tariffs represent a crucial tool for protecting and strengthening domestic industry in order to become competitive, especially for countries like those in South America. Doesn’t an EU trade agreement of this nature undermine efforts toward reindustrialization in the region?

European companies enjoy technological and productive superiority, better credit access, and stronger state support. Brazilian companies, conversely, face extremely high interest rates, scarce credit, currency instability, and logistical and infrastructure challenges. Aren’t we giving up a crucial industrial policy tool? Could this agreement reinforce Brazil’s trend of returning to a primary-export-based economy as has taken shape in recent decades?

MC: Absolutely. The agreement impacts it in both short and long-term. Short-term effects stem from tariff reductions. Even though the timeline for vehicle tariff reductions was extended, particularly for those with new technologies— the tariff reduction schedule for electric vehicles, for example, could extend up to 30 years—the current version doesn’t seek to revise the tariff reduction promised in 2019. We gave up on an instrument that could strengthen domestic industry in relation to a stronger trade partner, further complicating reindustrialization efforts.

Beyond tariffs, other crucial domains include public procurement, questions related to intellectual property, and so on. Securing public procurement mechanisms represents a significant achievement for Mercosur, and it’s worth noting that this is a hallmark of the current Brazilian government in the text. They insisted on this point, and now we will explicitly use it—just as developed countries do. This mechanism is particularly interesting, because it not only enables state support for specific sectors through preference margins and conditionalities but also helps to prompt certain practices—for example, requiring public procurement to be sustainable encourages suppliers to adopt sustainable practices. This applies both to domestic and foreign companies: if an international company wants to become a government supplier, it could, for example, face technology-transfer requirements.1

As for the intellectual property section, I get the impression that there haven’t been significant progress or reversals compared to 2019, which established slightly stronger commitments than those already made by WTO countries, but not much more than that.

Compared to previous versions, it seems that until around 2013 or 2014, the Brazilian government approached negotiations with a clear strategic vision centered on productive development and autonomy. That continuously shifted until 2019. While we might see some improvements now, the text retains several elements negotiated under a strongly liberal framework. The trade chapter, for example, has remained largely untouched.

MS: How might the agreement impact Brazil’s reindustrialization efforts?

MC: The trade part of the agreement undermines reindustrialization efforts targeting a more technologically dynamic and autonomous productive development. While some domains—such as public procurement and certain safeguards and rebalancing mechanisms—represent progress compared to 2019, they are insufficient.

Brazil’s large consumer market and position as South America’s export platform demand special consideration. So, it’s the Brazilian government’s role to try to impose conditionalities to compensate agreement-related losses. The mining sector offers a prime example. The government can potentially intervene in the conditions of mineral exploitation within national territory. There’s some room for negotiation with investors—for instance, by stipulating that certain advantages can only be accessed if more production stages occur domestically. However, this will depend on the domestic management of industrial, technological, fiscal, and tax policy instruments. It will also hinge on macroeconomic conditions, including growth potential and interest rate dynamics.

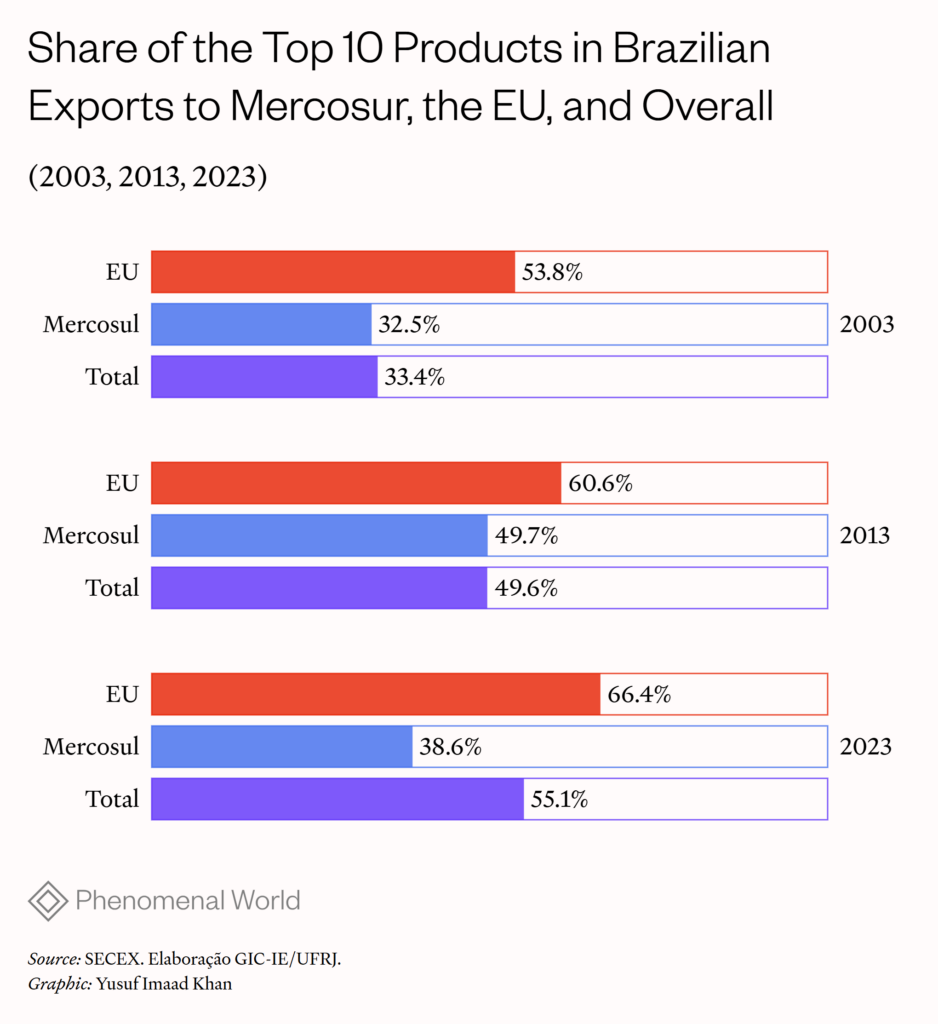

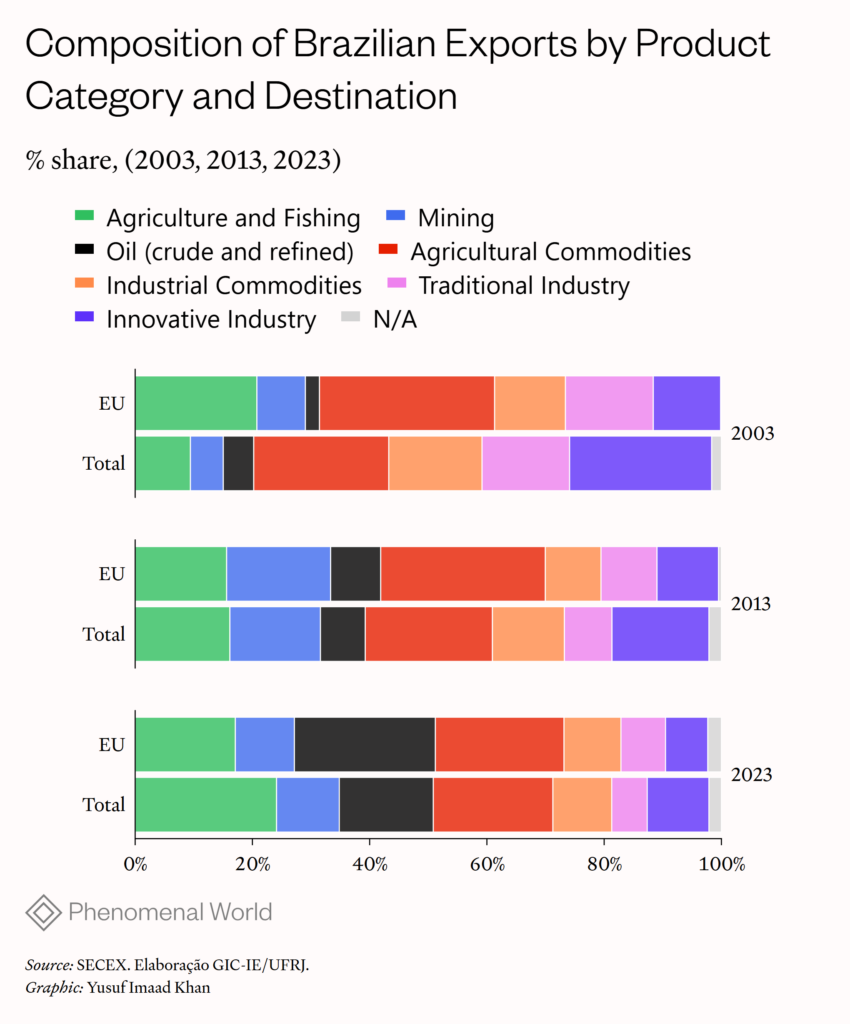

Moreover, it is important that the Brazilian government shares its advantages with other Mercosur countries. The problem with this agreement is that it tends to reinforce a pattern of growing regressive specialization, which has intensified since the 2000s across Brazil and the region. Comparing Brazilian exports to the EU in 2003, 2013, and 2023 reveals the increasingly primary nature of our exports profile. And the agreement tends to reinforce our specialization in agricultural and mineral products.

Order

2003

2013

2023

1

Soybeans, whether or not ground

Iron ores and concentrates, including roasted iron pyrites

Petroleum oils and oils obtained from bituminous minerals, crude

2

Soybean oilcake and other solid residues from soybean oil extraction

Soybean oilcake and other solid residues from soybean oil extraction

Soybean oilcake and other solid residues from soybean oil extraction

3

Iron ores and concentrates, including roasted iron pyrites

Soybeans, whether or not ground

Coffee, whether or not roasted or decaffeinated; coffee husks and skins; coffee substitutes containing coffee in any proportion

4

Fruit juices (including grape must) and vegetable juices, unfermented, not containing added spirit, whether or not containing added sugar or other sweetening matter

Coffee, whether or not roasted or decaffeinated; coffee husks and skins; coffee substitutes containing coffee in any proportion

Soybeans, whether or not ground

5

Coffee, whether or not roasted or decaffeinated; coffee husks and skins; coffee substitutes containing coffee in any proportion

Chemical wood pulp, soda or sulfate, other than dissolving grades

Copper ores and concentrates

6

Chemical wood pulp, soda or sulfate, other than dissolving grades